PayPal is one of the earliest and better-known digital payment app used by consumers and businesses alike to make money transfer around the world – online, through mobile payment apps, and in person.

Mobile payment app development is crucial for building a payment app like PayPal, considering the necessity for a robust payment gateway, transaction history feature, and the growing demand for digital payment solutions in today’s cashless and cardless transactions trend.

In this article, we explore how to build a payment app like PayPal and provide a solution to launch your digital payment applications faster and more affordable.

- History of PayPal: Timeline and Facts

- Why is PayPal so popular?

- What are the main features of PayPal?

- PayPal statistics

- Why payment platforms like PayPal are in demand?

- Why banks can’t keep up with PayPal?

- How to create a payment app like PayPal?

- What it takes to develop a white label PayPal alternative?

- White label software to build a PayPal alternative

Understanding Mobile Payment Apps

Mobile payment apps have revolutionized the way we make transactions, providing a convenient and secure way to send and receive money. In this section, we will delve into the definition and types of payment apps, as well as the benefits of creating a payment app.

Definition and Types of Payment Apps

A mobile payment app is a software application that enables users to make financial transactions using their mobile devices. There are several types of payment apps, including:

- Standalone payment apps: These apps are self-encapsulated ecosystems that allow users to make transactions without the need for a bank account or credit card. Examples include apps like Cash App and Venmo.

- Bank-centric payment apps: These apps are integrated with existing banking infrastructure, allowing users to manage their accounts and make payments directly from their bank accounts. Examples include apps like Zelle and many traditional bank apps.

- Social media payment services: These apps allow users to send and receive money through social media platforms. Examples include Facebook Pay and WhatsApp Pay.

- Mobile payment applications: These apps enable users to make payments using their mobile devices, often through NFC technology or QR codes. Examples include Google Pay and Apple Pay.

Benefits of Creating a Payment App for Businesses

Creating a payment app can have numerous benefits for businesses and individuals alike. Some of the benefits include:

- Convenience: Payment apps provide a convenient way to make transactions, eliminating the need for cash or credit cards. Users can make payments anytime, anywhere, using their mobile devices.

- Security: Payment apps use advanced security measures, such as encryption and biometrics, to protect sensitive financial data. This ensures that users’ payment information is secure during transactions.

- Increased revenue: Payment apps can increase revenue for businesses by providing a new channel for transactions. Businesses can reach a wider audience and offer more payment options to their customers.

- Improved customer experience: Payment apps can improve the customer experience by providing a fast and secure way to make transactions. This can lead to higher customer satisfaction and loyalty.

History of PayPal: Timeline and Facts

The terrific idea behind PayPal’s launch in 1998 was enabling people to “email money”. What started as a product without a definite use case and a market grew like a wildfire when it entered the eBay community.

At the time, people had to mail a check for a purchase, wait for it to arrive and clear, and wait for an item to arrive.

The already lengthy process was further complicated by lax fraud prevention measures, as a seller could simply not mail an item after receiving the payment. In stark contrast, PayPal let customers transfer money from their bank account to a seller PayPal account in hours instead of weeks and protected the money until the transaction was concluded.

By enabling much faster direct and protected payments, PayPal online payment platform grew from 10 thousand app users in 1999 to 5 million by the summer of 2000.

Now, the company is valued at over $193+ billion with many successful payment products like Braintree, Venmo, and Xoom under its wing and is expected to surpass a market cap of $1 trillion by 2030.

After 20 years of providing excellent service, PayPal continues to succeed for the same reasons – it provides faster and more convenient ways to pay for consumers and merchants alike. The scalability and reliability of its mobile payment system have been crucial to its growth and success.

With digital payments increasingly becoming the norm, many people are wondering what it takes to build a payment app like PayPal?

Why is PayPal so popular?

It’s easy to start with

One of the biggest advantages of PayPal payment infrastructure is its low barrier to entry. Anyone, including app users, can create an account and start using it in under 10 minutes, making it highly convenient for them.

Compared to opening a bank account at a traditional bank or a financial institution that requires a visit to a physical branch and tons of paperwork, PayPal is much more convenient. All you need to do is sign up and input your information online – no lengthy queues and unnecessary bureaucracy.

Connecting existing bank accounts or credit cards is very easy. As a result, all types of businesses and everyday consumers have quick access to a broad payment ecosystem. From splitting a bill at dinner to selling products online, PayPal gives people the ability to send and accept money with just a few taps.

Source: Pinterest

Once you set up a PayPal account with your bank account or credit card, you can keep using it wherever you shop. Instead of entering credit card information time after time, all you need to do is log in with PayPal to make a purchase. Not only does this save you time, but it also keeps your bank information safe during transactions.

It’s caters for ecommerce

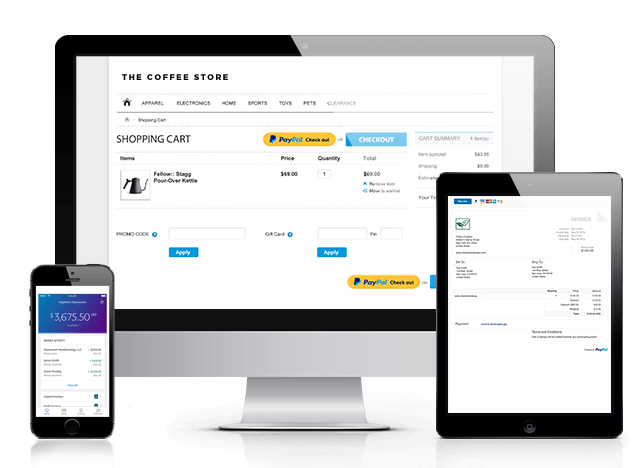

Retailers, e-commerce stores, and even restaurants who use the platform can attract customers with faster checkout, giving them an advantage over their competition. But that’s not the only benefit for business owners. PayPal’s merchant services are a fantastic way to keep things organized. A reliable and secure payment gateway is crucial for mobile payment app development.

Source: PayPal official website

Tracking orders, generating sales reports, and keeping track of invoices is easy with PayPal payment infrastructure. Furthermore, the system’s flexibility lets merchants set up new payment links and buttons in virtually any situation.

While those tools provide a great foundation, PayPal also has partnerships with many third parties to help you grow and manage your business.

From website and store builders like Squarespace, Wix, BigCommerce, and Shopify to partners like Magento that enable you to further develop your business, multiple quick and easy integrations make Paypal payment platform a one-stop-shop solution for many companies worldwide.

It’s secure

Despite how popular and commonplace online shopping and mobile payments have become, concerns over the safety of consumer data and payment information remain as relevant as ever. PayPal’s solution is to act as a mediator between buyers and sellers to resolve disputes and any order discrepancies.

Developing secure payment apps that prioritize full security and robust performance is essential in the fintech industry. Although the resolution process may take some time, it is good to have an additional security layer to prevent fraud. These features make digital payment platforms like PayPal incredibly attractive to customers and merchants for their functionality, convenience, and user-friendliness, all of which stem from the versatility of PayPal’s core payment system.

What are the key features of PayPal?

| Feature | PayPal digital payment platform |

| Payment options | Instant payment, split payments, accepted credit cards and debit cards, ACH payments and eCheck processing, multi-currency, online payment portal |

| Security | Data tokenization, two-factor authentication, PCI compliance, POS verification |

| Development | Customization, accounting software integration, e-commerce software integration |

| Invoicing | Provide |

| Platform | Internationalization, PCI regulation compliance, e-commerce, and accounting integration |

| Payment tools | Payment gateway, expense tracking, payment schedule |

| Customer service | Live chat, phone support, knowledge base |

| Additional services | Seller’s Protection Program |

Launch your digital bank in weeks, not years

Talk to Our TeamPayPal statistics

- 427 million active accounts (as of Q1 2024)

- 29 million active merchant accounts (as of the end of 2023)

- $29,9 billion in total revenue in 2023 (an 7.9% increase year-on-year)

- $4.2 billion net profit in 2023

- $1.52 trillion transaction volume in 2023

- 41 million transactions are done via PayPal every day

- Supports 100+ currencies

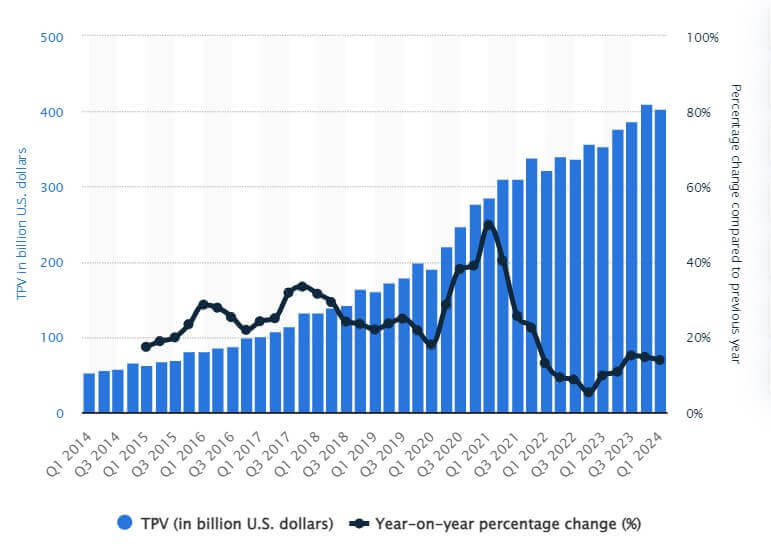

Total payment volume 2014-2023, $ billion

Source: Statista

Why payment platforms like PayPal are in demand?

According to McKinsey, the global payment market revenue in 2022 was $2.2 trillion and is expected to grow by 7% per annum to $3 trillion in 2027.

Customers are increasingly turning to nonbank financial providers like PayPal for the functionality traditional banking services do not provide.

Creating your own payment app can be a lucrative opportunity, offering customization, specialization, and the convenience of contactless payments, which are expected to see further adoption. Additionally, safeguarding payment data is crucial for building user trust and ensuring the app’s functionality. The incumbent banking system relies on physical branches to open accounts, make transfers, and service customer requests, which is highly prohibitive for some customer groups.

Those in rural areas or those working long hours have to make special arrangements to travel to a physical branch only during office hours just to make use of their account.

Even then, traditional banks cover their high overhead by passing the costs onto the consumers in the form of high and unexpected fees.

Payment providers, in comparison, offer unparalleled convenience and transparency. With just a smartphone, customers can interact with their money whenever and wherever they want.

For example, consumers use PayPal for cheaper and often free account-to-account payments (A2A) that are quickly rising in popularity in Europe and Asia. Low and transparent fees are easy to understand and enable customers to reap the benefits of vast financial ecosystems.

Quick loan approvals and a myriad of business management tools and integrations make payment providers like PayPal vastly more beneficial and cost-effective to merchants when compared to traditional payment providers.

As the conventional sources for growth in retail payments change and become more digital, the market will shift towards payment providers who rely on efficient technology infrastructure to deliver superior features to consumers.

Why banks can’t keep up with PayPal?

The reason why traditional providers like banks cannot implement new functionality lies in their closed legacy systems which require a lot of time and resources to upgrade.

Some of them are struggling to integrate even the most basic functions like currency exchange.

Modern payment apps, on the other hand, rely on a much more flexible and stable API-first architecture to roll out new features in a fraction of the time.

These factors make payment platforms like PayPal attractive not only to underserved customers but to those with accounts at traditional banks because they can drastically increase their payment options in under 10 minutes.

Planning and Development Process

Building a successful payment app requires a strategic and comprehensive approach. In this section, we will outline the planning and development process for creating a payment app.

How to create a mobile payment app like PayPal?

Understanding the cost and technical aspects of money transfer app development is crucial for a successful project. P2P payment app development involves addressing various technical challenges and ensuring user-friendly interfaces and security measures.

P2P payment apps come with various features and market examples, including bank-centric, social media-centric, and mobile OS-focused apps.

To clarify how to create a payment app like PayPal you need to keep the following steps:

1. Outline the scope of the project

Set up the goals, deadlines, and project requirements you’ll be working towards to build a payment app. It can help you to clarify the project scope to ensure that all of the project’s elements are aligned with the objectives.

2. Choose the correct SDLC model

You can start with an MVP model that targets specific geography and a limited set of features. These key features should encourage users to try the payment app and highlight its advantages over competitors. The goal is to validate the concept and gather user feedback without incorporating additional, nice-to-have features.

3. Hire a team to develop a digital payment system

Then you need to find an experienced team that can help you with the fintech software development process. Developing a P2P payment app requires a skilled team to address various software disciplines and ensure transaction security. Business analysts, UI designers, web developers, Android developers, iOS developers, a group of testers, and project managers must be familiar with specific payment technologies stack to create an app like PayPal.

4. Get a cloud service provider

You can speed up the development process by using cloud services to manage the platform infrastructure. Utilizing a ready-made server, storage, operating system, or runtime environment reduces costs and time to market.

5. Get an online payment solution (an API/SDK)

To build a payment app, you require an API/SDK solution to develop a PayPal payment infrastructure. The primary elements of online banking electronic payments can be included this in their implementation. With this integrated solution, you may start accepting payments online right away. These platforms usually work with the web, Android, and iOS.

7. Comply with financial regulations

To comply with the strict requirements governing financial sector companies, an online payment app needs an ID verification solution.

The system should make it possible to validate government-issued identification, as well as handle compliance with the “Know Your Customer” (KYC) and “Anti Money Laundering” (AML) processes for sensitive financial data.

Watch the SDK.finance demo video to explore how to simplify transaction management, ensure financial compliance, and create successful payment app with our powerful FinTech Platform.

This video highlights how SDK.finance provides a comprehensive view and control over your client transactions, as well as the AML & fraud prevention functionality:

8. Design and develop your payment platform

Before your team starts a payment app development, choose the most optimal technology. To create payment app like PayPal, you should first consider what must-have MVP (minimum viable product) features it will have, these can be:

- Unique ID verification

- Digital wallet

- Sending bills and invoices

- Sending and receiving money

- Transaction history

- Messaging

Additionally, the user interface and experience design in payment gateway apps are crucial for ensuring customer satisfaction and security.

9. Conduct the testing process

Finally, you should test your online and mobile applications across a variety of browsers and platforms before launching them.

What it takes to develop a white label PayPal alternative?

PayPal system design was built and rebuilt multiple times over the last 20 years. Although building a payment platform is a complicated process, here we highlight the most vital components which are mandatory to create a payment platform similar to PayPal.

It is crucial to ensure compliance with regulations and incorporate features of well-known payment apps.

Additionally, the importance of secure and reliable payment gateways cannot be overstated.

Core digital payments platform

The most important part of any digital payment platform is the core software. It is the engine behind the creation and management of accounts, balances, transactions, journal entries, and the storage of customer data, receipts, and other reporting tools.

A good core platform relies on a composable architecture that is connected via APIs and allows sales channels, products and customer data to be decoupled. This particularly agile architecture enables rapid change while providing a continuous digital customer experience.

Onboarding, payment processing and KYC services must then be integrated into the platform. Developing a core platform in-house is a complicated and time-consuming process that can overwhelm teams and delay product launches. For this reason, very few payment providers have their own platforms.

Many PayPal alternatives have outsourced creating their core payment platforms to fintech providers. New cloud-based platforms with pre-integrated key features help assemble best-in-class products and bring them to market much faster and with less capital expenditure.

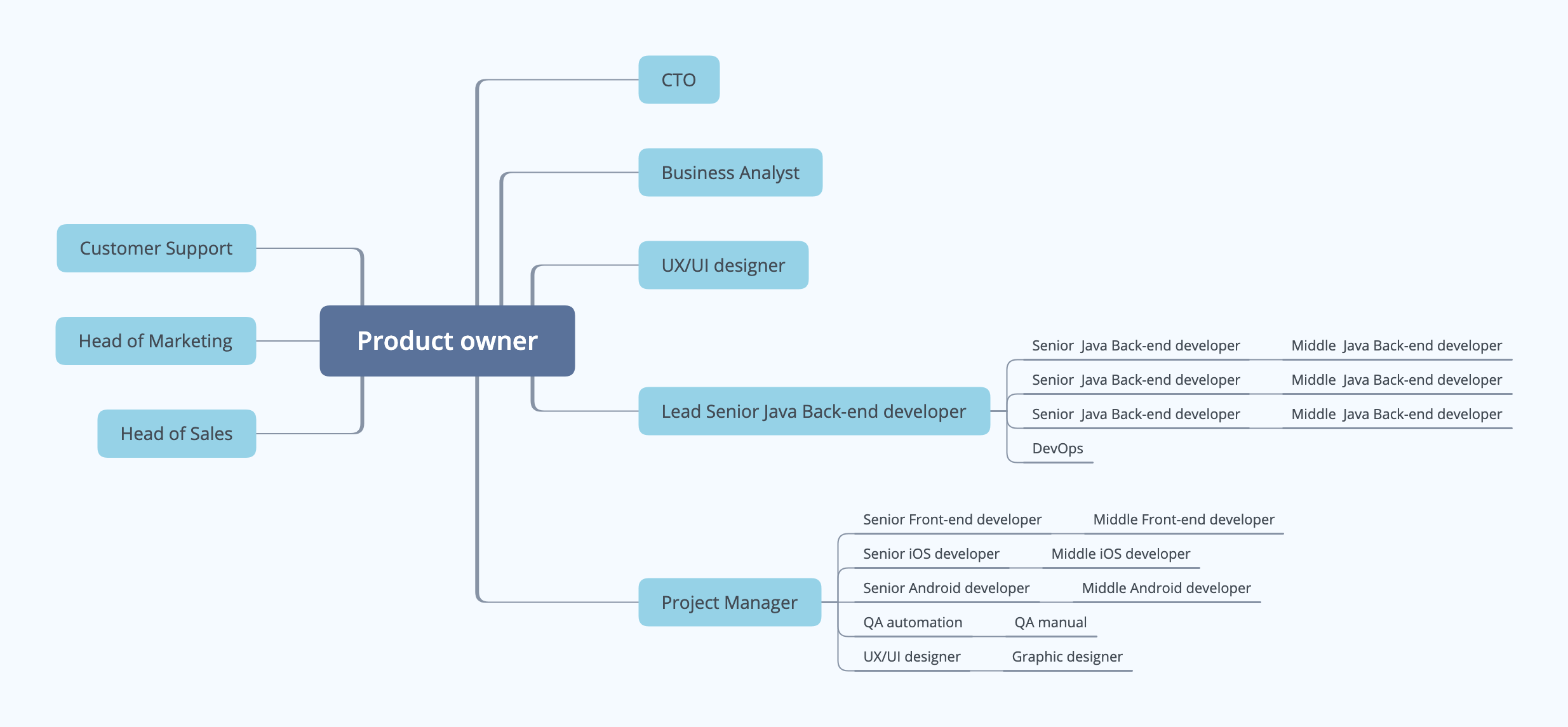

100% dedicated team

It cannot be overstated how important it’s to have the right team in place to build a digital payment platform like PayPal. The team should be made up of people who’re genuinely interested in seeing your vision through to the end.

A development team should resemble a special unit on a mission. Their success is based on shared responsibility, trust in each other, and lack of doubt about their purpose and goals.

A small team may have the following structure:

Vision & growth hacking

Developing and sharing your vision with your team will help them understand what they are working to achieve and encourage them to work with passion. PayPal’s first goal, for example, was to determine their use case and find an opening in the market which they achieved by adapting their product for eBay.

Using a growth hacking strategy, you can then deliver your unique vision to consumers. This scientific approach consists of choosing and testing a single hypothesis at a time to see whether it works or not.

Fast features delivery

If a startup wants to succeed in a new market, it needs to innovate much faster to outperform the competition. Releasing new versions is important to provide customers with a superior product, and that’s exactly what PayPal has done.

For example, compared to a traditional payment provider’s app that only gets a few updates a year, PayPal releases a new version every few weeks. The constant updates and fixes allow PayPal’s system design to satisfy its growing customer base and stay ahead of the curve.

The problem with traditional payment providers is that the journey from an idea to launching a feature can take months or even years. The same idea can be implemented within weeks by a payment provider running on a modern technological infrastructure.

The difference lies in the overall business processes and product development lifecycle.

Ready backend, APIs, and integrations

Talk to Our TeamWhite label software to build a PayPal alternative

There are many worthy next-generation fintechs competing in the payment services market. SDK.finance with its white-label digital wallet platform has been quite successful at helping businesses get their payment systems up and running fast and without too much time and money investments.

SDK.finance offers a highly secure white-label digital wallet software that allows building a PayPal-like platform and fulfill the need for it in the markets where it is lacking much faster, than in case with from-scratch development.

If you are looking for a solution to develop a FinTech app like PayPal, reach out to us and let’s discuss how we can be useful to you.