The neobanking market is expected to grow to $394 billion in value by 2026, at a CAGR of 46.5% in the coming years, driven by underserved market segments such as non-bank customers, SMEs, freelancers, startups, and credit entrants. The largely undisturbed retail banking business, which has enjoyed excessive profits and left many customers dissatisfied and unserved, is now threatened by neobanks.

Revolut, Fidor, Simple, N26, and Monzo are some of the well-known neobanks, the alternatives to which incumbent banks are trying to develop. For instance, Goldman Sachs has launched Marcus, and RBS has launched its standalone version called Bó to compete with the “newcomers”.

What creates the demand for digital banks?

Digital banks offer unparalleled convenience and transparency to their users: via their smartphones, customers can open an account whenever and wherever they want. In addition, low and transparent fees allow customers to reap the benefits of financial services.

The established banking system, on the other hand, relies on physical branches to open accounts, carry out transfers and handle customer queries, which is very restrictive for some customer groups.

Those who live in rural areas or work long hours need to make special arrangements to travel to a branch during business hours just to open an account.

Moreover, traditional banks cover their high overheads by passing on the costs to consumers in the form of high and unexpected fees. So, digital banks are a lot more accessible and cheaper to use than brick-and-mortar ones. Now, let us look at Revolut, one of the most prominent representatives of the digital banking industry and its evolution.

Launch your digital bank in weeks, not years

Talk to Our TeamWhat is Revolut?

Revolut operates in the UK under an electronic money institution (EMI) licence regulated by the Financial Conduct Authority. Within the European Union, Revolut Bank UAB holds a full banking licence issued by the European Central Bank and is supervised by the Bank of Lithuania.

As of 2026, Revolut is considered one of the largest and most recognised digital banking brands in Europe, serving tens of millions of retail and business customers globally. The company has continued expanding its banking, payments, and wealth management capabilities while maintaining a strong focus on mobile-first financial services and international growth.

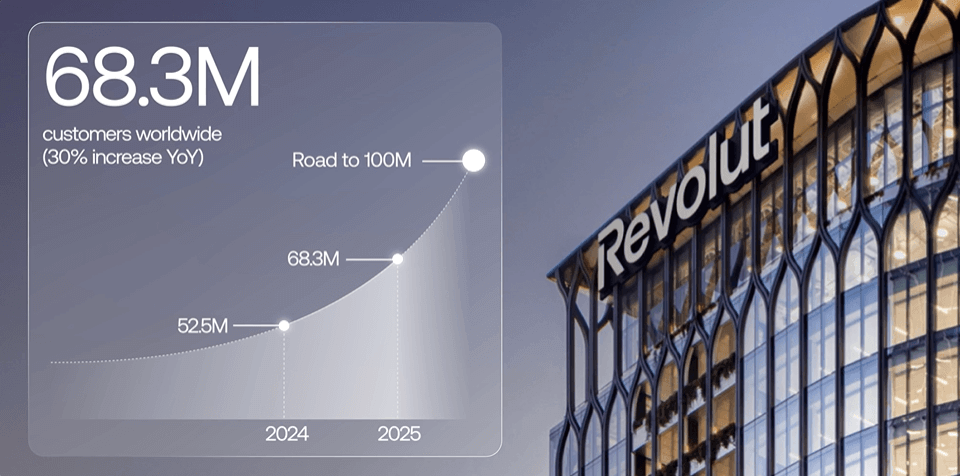

Revolut users and revenue stats

- 68.3 million – number of Revolut customers globally (as of December 2025)

- 1 billion+ – number of monthly transactions processed in 2025

- 10+ thousand – people working for Revolut globally

- +38% – total customer growth in 2025

- £4.5 billion – revenue in 2025 (72% increase compared to 2024)

- 38+ – countries where Revolut services are available

- £50.2 billion – customer balances held by Revolut in 2025 (66% increase compared to 2024)

Source: Revolut annual report 2025

Revolut Number of Users Worldwide in 2025

Image source: Revolut official website

This fintech startup has attracted millions of customers by allowing its customers to do almost anything online that most traditional banks do offline.

Many people wonder what has made Revolut so successful and search for a “recipe” on how to build a digital bank that could make a real alternative to this giant.

Why is Revolut such a popular platform?

Revolut’s banking features make managing your money incredibly easy. Although the term “user-friendly” is used far too often today, in this case, it perfectly sums up the Revolut experience. Simple everyday use examples show why Revolut is much better than a traditional bank.

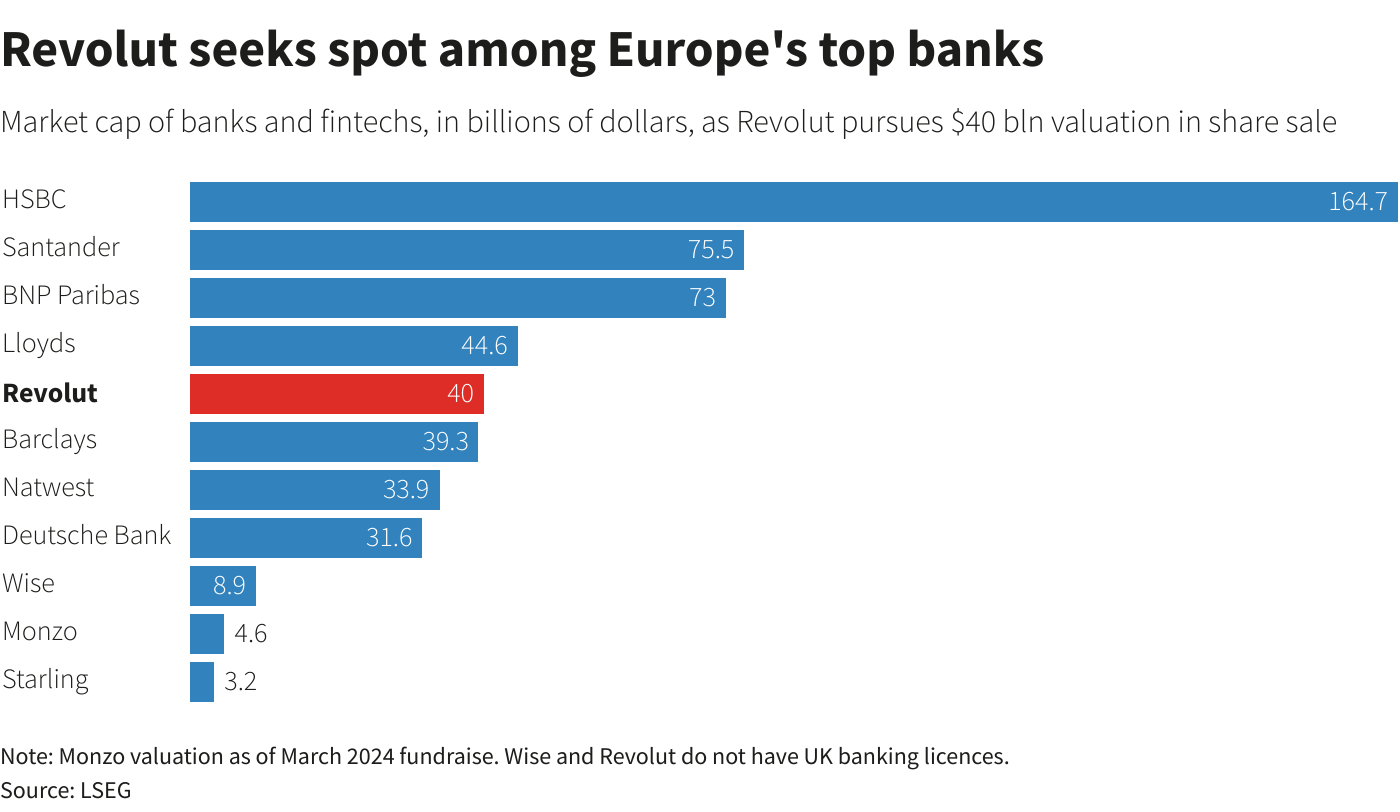

Source: Reuters Graphics

Truly user-friendly

Image source: Revolut official website

User-friendly experience is top priority for this neobank. Compared to the long queues and never-ending red tape at traditional banks, opening an account with Revolut is a breeze. And it’s not just one basic account – you can set up more accounts in 30 currencies with just a few taps and at no cost.

Investments and trading

Revolut allows users to invest directly from the app in stocks, ETFs, commodities, and selected cryptocurrencies. The platform combines banking and investment services within a single mobile interface, helping users manage everyday spending and investments in one place.

Crypto and digital assets

Revolut integrates cryptocurrency buying, selling, and holding functionality directly into its banking app. In selected markets, users can access crypto trading and digital asset features without using a separate exchange platform.

Multi-currency

You can spend the money in any of your currencies via a card you receive in the post, making it much easier to travel and spend abroad. Revolut allows users to spend in multiple currencies without incurring additional transaction fees.

Let us say you are in Prague and have a few Czech crowns in your secondary account, but not enough to buy another cup of coffee. Revolut automatically converts your primary currency to make up the difference when you pay with your card.

International transfers

Revolut supports low-cost international money transfers across multiple currencies and countries. Users can send funds internationally through the app with transparent exchange rates and faster settlement compared to many traditional banking providers.

Deposits

£50.2 billion was held in Revolut customer balances in 2025, representing a 66% increase compared to 2024. Revolut allows users to open accounts digitally, manage multi-currency funds, access savings products, and use investment features directly from the app. Savings returns and interest rates vary depending on the customer’s plan, product type, market conditions, and selected currency.

Personal loans

Lower foreign transaction fees

But that’s not the kicker. Unlike traditional banks, Revolut Bank does not charge you exorbitant foreign currency fees or exchange your money at a terrible rate that’s set once a day.

Instead, you get a constantly updated interbank exchange rate with no fees, so you save money on every transaction. Revolut estimates that customers save an average of £46 when traveling abroad.

The same applies to international bank transfers. Apart from the interbank exchange rate, Revolut does not charge any fees for money transfers or currency exchange. This is what makes this digital bank very popular not only with frequent travelers and ex-pats but also with people having family abroad.

No more card-related fuss

Revolut Bank has solved the usually complicated problem of lost cards. Instead of calling your bank’s hotline and spending time on hold, you can change your pin code or block your debit card in the Revolut app with just a few taps. Revolut also offers fee-free debit card spending overseas and provides additional debit cards with various benefits and perks.

There you can adjust your spending limits and quickly switch between magnetic stripe, NFC, and ATM transactions for added security.

Kids and junior accounts

Revolut also offers kids and junior accounts designed for children and teenagers. These accounts allow parents to create and manage cards for their children directly through the Revolut app, monitor spending, transfer pocket money instantly, and set spending controls or limits.

The feature is aimed at helping younger users learn basic money management while giving parents visibility and control over transactions in real time.

Business accounts

In addition to retail banking, Revolut provides business banking products for freelancers and companies. These include multi-currency business accounts, expense management tools, team cards, and international payment capabilities.

Budgeting and analytics

The app provides real-time spending analytics, transaction categorisation, budgeting tools, and instant payment notifications. These features help users monitor expenses and manage personal finances more effectively.

Integrated travel features

Revolut includes travel-oriented services such as global card payments, travel insurance on selected plans, airport lounge access, and support for multiple currencies within a single account.

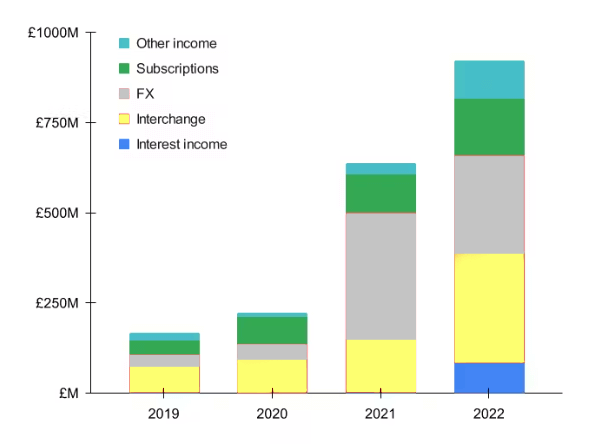

Revolut Business Model: How does Revolut make money?

Image source:BusinessofApps

Taken the favourable conditions for the customers and low fees, many people are left wondering – how does Revolut earn money? Or, more generally, how do digital banks make money? Let’s take a closer look at Revolut’s business model.

Revolut offers a comprehensive range of payment services for personal and business customers, including overseas payments, savings, and investment products.

According to Revolut’s official data, there are a few main sources of this digital bank income:

Image source: Sacra

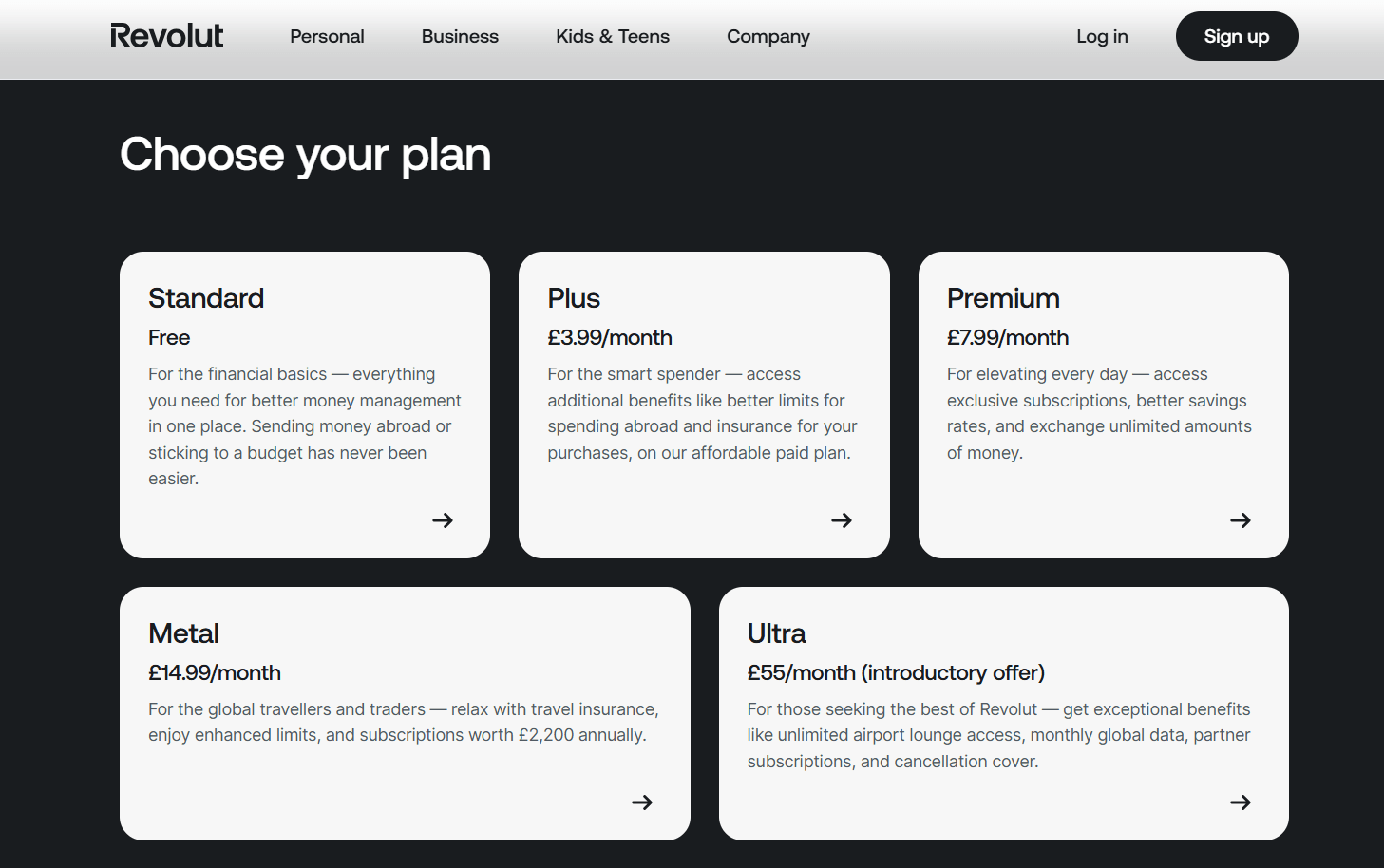

Revolut Plus, Revolut Premium, Revolut Metal, and Revolut Ultra paid subscriptions provide unlimited foreign exchange, higher ATM withdrawal limits, and benefits like travel insurance and airport lounge access, with prices ranging from £3.99 to £55 per month.

There’s one more thing, however. Every time a customer makes a card purchase, the card scheme (Visa or Mastercard) returns a portion of the fees to Revolut. It is an incredibly small percentage fee, but it adds up when millions of purchases are made.

As B2B users companies can create accounts that offer multi-user access, expense management, and API integration, with plans starting at £25 per month.

Benefits of Revolut vs. traditional banks

Unlike traditional banks, Revolut offers its customers full control over their banking experience. They are free to set their security preferences, such as whether or not to enable NFC or magnetic stripe payments. Customers can also use the features that established banks simply don’t offer, from buying cryptocurrencies and gold to investing in the NYSE. Unlike high street banks, which charge around €3 per transaction for ATM usage in Spain, Revolut offers more cost-effective solutions.

The reason traditional banks can’t implement new features is because of their technology infrastructure. Closed legacy systems require a lot of time and resources to upgrade, and some banks struggle to integrate even the most basic functions like currency exchange.

Digital banks, on the other hand, rely on a much more flexible and robust API-first architecture to introduce new functionality in a fraction of the time.

These factors make Revolut attractive not only to the previously underserved customers but also to those who’ve accounts with traditional banks. If you can open a free bank account in the time it takes to download a new app, trying out a neobank is as easy as can be.

SDK.finance provides core banking infrastructure with ledger, payments, wallets, ready applications and flexible deployment options

Talk to Our TeamMust haves needed to build a digital bank like Revolut

Revolut, like Rome, wasn’t built in a day. We at SDK.finance know all too well that building a digital bank is a complicated process (based on our 15-year experience in creating banking software).

Revolut provides a range of services and is regulated by various authorities, ensuring compliance and security for its users. So, what are the key components that are mandatory for building an app similar to Revolut?

Core banking system

An essential part of any digital bank is its core banking platform. It is an engine behind accounts, balances, transactions, the storage of customer data, receipts, and other reporting tools.

A decent core banking software relies on a composable architecture that’s connected via APIs and allows distribution channels, products, and customer data to be decoupled.

This particularly agile architecture allows for carrying out quick changes while providing a continuous digital customer experience.

Once the banking core is ready, customer onboarding, payment processing, card issuing, and KYC services are integrated into the platform. Developing a core banking platform from scratch is a complicated and time-consuming process that can overwhelm teams and delay product launches.

For this reason, very few banks use their own platforms. N26, Tandem, O2 Banking and other Revolut competitors have outsourced their core banking platforms from the fintech software vendors. The new cloud-based platforms with pre-integrated key features help assemble best-in-class products and launch them much faster and with less capital expenditure.

SDK.finance provides core banking infrastructure with ledger, payments, wallets, ready applications and flexible deployment options

Talk to Our TeamDedicated team

It cannot be overstated how important it is to have the right team to develop a digital bank like Revolut. A team should be made up of people genuinely interested in implementing your vision through to the end. Their success is based on shared responsibility, trust in each other and a lack of doubt about their purpose and goals.

Here is an an example of what a small digital bank team can look like:

Vision & growth hacking

Vision shared within the team, helps everyone understand what they are working towards and encourages the work with passion. Growth hacking consists in selecting a single hypothesis at a time and testing it to see if it works out or not. Then you need to document and analyze the results before moving on to the next iteration. The approach is particularly attractive to startup founders because it focuses on rapid growth. Although some results may turn out to be complete failures, other experiments may produce a successful strategy for exponential growth.

Quick features delivery

For a startup with limited resources to succeed in a new market, it needs to innovate much faster to outperform the competition. Launching new versions is crucial to provide customers with a superior UX, and that is exactly what Revolut has done.

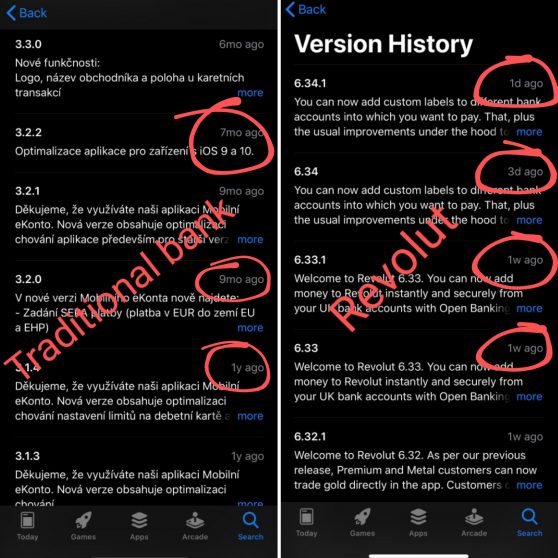

Updates frequency: Revolut vs. traditional banks

Compared to a traditional banking app that has a couple of updates a year, Revolut releases a new version a few times a week. Its constant iterations and fixes allow it to continuously please its growing customer base and stay ahead of the competition.

The problem in traditional banking is that the journey from an idea to a rolled-out feature takes months or even years. On the other hand, neobanks can implement this in weeks thanks to different business processes and product development lifecycle and core banking software, of course.

Image source: Revolut

Since any bank is based on a core bank system, it is often the main barrier for the implementation of the new WOW features that customers love.

Digital banking software to create a Revolut-like bank

If your goal is to launch a digital bank like Revolut, SDK.finance gives you the core infrastructure needed to move faster without building everything from scratch. The Platform combines:

- a robust ledger,

- multi-currency accounts,

- payments,

- wallets,

- transaction processing,

- role-based back office,

- ready-to-use mobile applications in one modular system.

This makes SDK.finance a strong fit for fintech teams, EMIs, PSPs, and financial institutions that want to launch a neobank, digital wallet, or mobile banking product with Revolut-like functionality while keeping control over the product roadmap. Instead of spending years developing the banking core, account logic, transaction flows, and operational tools from zero, you can start with a proven fintech platform and focus on customer experience, integrations, compliance partners, and market growth.

SDK.finance is API-first and integration-ready, so you can connect KYC providers, card issuing partners, payment gateways, FX services, compliance tools, and other third-party systems required for a modern digital banking ecosystem. The platform is available as cloud-based SaaS or source code, giving your team flexibility depending on your technical strategy, security requirements, and scaling plans.

Watch the SDK.finance mobile banking app UI in action and see how the Platform can help you launch a secure, feature-rich digital banking product faster:

In short, SDK.finance helps you build the foundation of a Revolut-like digital bank faster: accounts, balances, payments, wallets, mobile apps, back office, and integrations are already covered, so your team can concentrate on launching, differentiating, and scaling the product.

SDK.finance provides core banking infrastructure with ledger, payments, wallets, ready applications and flexible deployment options

Talk to Our Team