The payments industry is undergoing a rapid transformation. The expansion and modification of payment apps, the proliferation of gadgets & devices, evolving socioeconomics, the need for financial inclusion, and the imperative for innovation have all prompted the rise of another class of players in the online payments space – fintechs. It’s no doubt that today, fintechs stand as exemplifiers of the fabrics of innovation and interconnectivity that have come to characterize & describe the payments industry. Other players like telecom companies & regulators like the PSD2 have not been left behind in their endeavor to level the playing field, placing the customer as the ultimate beneficiary. Slowly, but surely, these disruptions are gradually shifting the payments ecosystem from a commoditized entity to a strategic instrument that will provide value for consumers. Even so, no one can dispute the fact that transfers and online payments are two of the financial sectors most disrupted by fintechs. Banks being the focal point of payment transactions, the need to create new wellsprings of income will constrain them to tread on collaborative innovation with advancement & progress highly based on the interconnectivity of various partners in the financial industry scene. The Application Programming Interfaces (APIs) and particularly the P2P payment APIs have turned into absolutely essential units to help in the accomplishment of such interconnected communities within the financial frameworks and landscape. A functional peer-to-peer payment system, or person-to-person payment API is a quintessential aspect of every strong/robust digital ecosystem and a critical component to the soundness & health of the surrounding financial economy. Launch your payment project in record time P2P payment (or peer-to-peer payment) is an electronic exchange made from one individual to another with the assistance of the P2P payment apps. Through these applications, each individual record gets connected to the next user’s digital wallet. When the exchange happens, the record balance in the P2P payment apps records it and pulls cash specifically from one user’s ledger or application wallet and sends it to another. P2P payment has been instrumental in revolutionizing the e-commerce enterprise. To get the big picture, P2P transactions ordinarily involve the trade of cash from one user to another via digital utility applications onto which a credit or debit card or linked bank account details are linked via the internet. Typically, the P2P dynamic solely rests on the seamless flow of cash without the necessity of the physical presence of a human being. The emergence & advancement of smartphones in the payment processing arena has further facilitated the development, progress, and mainstream acceptance/adoption of peer-to-peer payments & transactions. Through P2P applications, each individual record gets connected to the next user’s digital wallet. When the exchange happens, the record balance in the payment apps records it and pulls cash specifically from one user’s ledger or application wallet and sends it to another. Whether it’s paying bills, making in-store purchases, splitting bills payment, or paying back a buddy who loaned you some cash, peer-to-peer payments apps make the art of sending and receiving money effortless & flawless. They connect with the person’s bank account, credit or debit card, and rapidly transfer funds to whoever you want. In a similar fashion, a peer-to-peer payment API must be highly functional, practical, accessible, and convenient for many users. This is because just like any other ecosystem, peer-to-peer cyber systems will only grow if their APIs will enable their users to thrive. This simply means that when choosing a P2P payment API one must be savvy enough to recognize an API that will enhance efficiency, and reliability, and create new opportunities. It should equip you with the creativity to find ways of incentivizing various stakeholders to join in; and most importantly facilitate the success of its users, partners, and other constituents. A quality P2P payment API should guarantee easy and streamlined onboarding processes for all users while at the same time ensuring that customers benefit maximally from this payment method. Most peer-to-peer payment systems are generally simple & easy to use with user-friendly methodologies. The peer-to-peer Application Programming Interface provides a way for you to integrate your existing systems with your P2P events. This being the case it’s often said that you’re better off going for a superior technology payment API that will easily integrate other digital payment apps for an enhanced, better, and seamless user experience. In this regard, as you pick your API, you ought to ask yourself the following question: “Should I assemble an API from scratch, or utilize an existing solution that offers third-party integration?” Quite often, using ready solutions is a more sensible option, especially for smaller business due to factors like: So, if a great P2P payments transfer API is already available in the market to suit your business model perfectly, why not leverage it to launch faster and start growing your business? Let’s suppose you decide to build your payment API for P2P transfers from scratch. The first obvious advantage is that building your own API enables you to amplify on the various potential outcomes for customization. You basically have the final say from the research and development phase all the way to the final deliverables. Building your own API comes with its advantages and challenges when it comes to making sure you have a high caliber and easy-to-use person-to-person payment system app.

Create your digital banking solution in weeks As such, other key features to put into consideration when choosing a payment API for P2P transfers include a number of important ones. A P2P payments API can only be termed as secure if it can effectively reduce the risk of unauthorized transfer of funds. This can be done by evaluating the extent to which the API prevents sensitive account information from falling into the hands of fraudsters. One crucial element to enhance this security is integrating a verify API, which ensures that each transaction is authorized by the rightful user, preventing unauthorized transfers and fraud. Another aspect of security can be assessed by measuring the strength of the authentication procedure used to verify that a transfer funds has been authorized by a legitimate user. If such authentication were foolproof, a fraudster in possession of a consumer’s account information would be unable to impersonate the consumer and use the stolen information to make unauthorized withdrawals/transfers of funds from the consumer’s account. Speed alludes to the time between the initiation of payment by the payer and the completion of the transfer of funds to the payee. With quick peer-to-peer payments, payers can progressively monitor their funds and ascertain when cash will be transferred out of their accounts and how their parties will be influenced. Therefore, they will be less likely to acquire unintentional overdrafts or have peer-to-peer payments denied on the grounds that they have depleted account balances or surpassed credit limits. Rapid payment has comparative advantages for consumers receiving P2P payment apps, by giving them more prominent sureness about the planning of inflows to their records/accounts. Payer control refers to the payer’s capacity to pick the most beneficial terms for the transfer of funds to the payee. Solid payer control over the exchange of funds benefits users by helping them manage their funds and control their spending, using a peer-to-peer payment system. In particular, certainty about the timing of exchanges and increased access to data about account status enables payers to maintain a strategic distance from overdrafts and effectively manage their account balances. Another valuable trademark in choosing a payment API for P2P transfers is its potential for universality. What are the odds of the API gaining far-reaching acknowledgment or widespread acceptance among consumers? The potential for the universality of a P2P API depends on two principal factors. The primary factor is the means by which appealing consumers would discover the peer-to-peer payments API if they were to use it and the assurance that the other party to the transaction would be willing to use it. The answer to this question depends on the cost and convenience of utilizing the service after setup and on other characteristics of the payment that affect the benefits to the user, for example, speed, payer control, and security. The second factor is the cost imposed on the customer to set up and utilize the service. This will incorporate both the time required to enroll and figure out how to utilize the service and the cost of any equipment required, for example, a smartphone. The cost additionally relies upon whether the user must have an account with the participating linked bank account or card network in order to access services and, assuming this is the case, how likely the consumer will be willing to have such an account or have the capacity to set up one. The structure of the API must be steady, logical, and convenient. There must be clear error messages when something isn’t correct. The recipient is then notified with the aid of an e-mail or textual content message that a certain user is sending them money, along with instructions on how to securely receive the funds. As soon as this is accomplished, the funds are electronically transferred and the transaction is completed effectively, securely, and rapidly. There are some peer-to-peer payment APIs that don’t give any client support. In this circumstance, clients need to take after manual guidelines to settle an issue. To stay away from such circumstances, check whether the API supplier offers live technical help, at the least within average working hours. This is to allow fast resolutions every time a technical problem may arise. Within the coming years, mobile payments will change credit card shopping, even in point-of-sale environments. P2P transfer APIs that support cell payments permit customers to transfer funds using their cellular phones, either through the branded payment apps or by way of a cellular-optimized web page. View the demo video of the SDK.finance Platform to see how you can streamline transaction management and guarantee financial compliance using our robust FinTech Platform: Some P2P payment APIs only support payments in a limited number of currencies. As such, depending on your business needs, it’s important to adopt an API that will support various currency denominations based on your geographic and demographic target audiences. Although supporting additional payment methods can be difficult due to integration risks and complexity, a good P2P transfer API should work to reduce the risks and complexity of technical integration. It should facilitate simple and elegant integration processes with minimal development time & fewer maintenance costs. This alludes to a set of non-functional requirements like availability, scalability, and stability, that build trust and present the necessary ingredient in measuring the efficacy of a P2P transfer API. Also sometimes referred to as “automated onboarding,” this is a key component of a quality P2P payments API, as it does not require staff to manually create accounts. If you are planning to build a business of a meaningful scale, choosing a quality payment API for P2P transfers is certainly justified regardless of the resources it may require. Additionally, building your own Payment API that is particularly custom fitted to your organization’s needs, and centered on scalability and efficiency, can go a long way in defining the difference between offering a commoditized service and offering a highly differentiated one at a superior cost.Payments industry overview

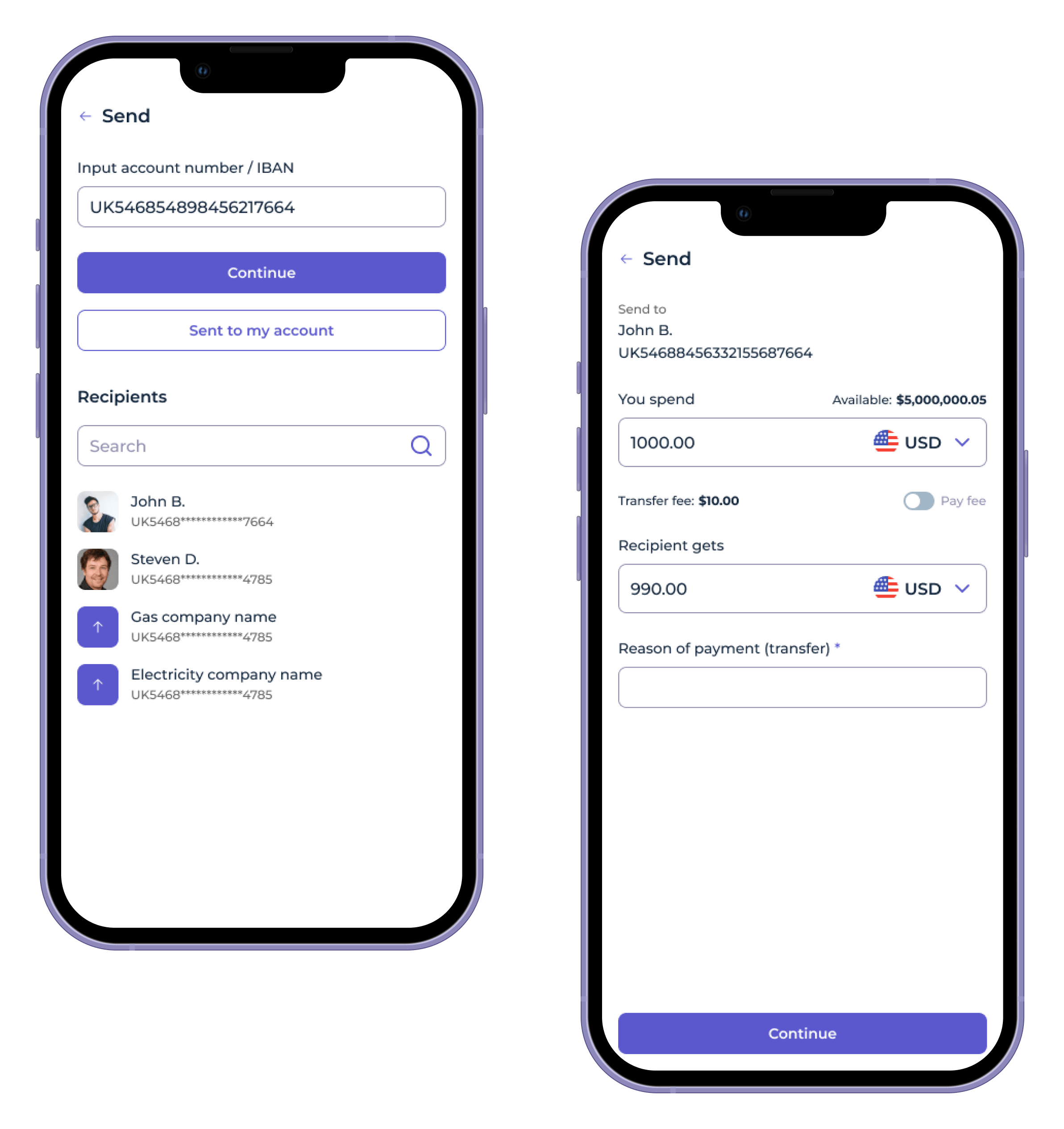

What is a P2P payment?

How the p2p payments process typically works?

Payment API for P2P transfers: the importance

P2P money transfer API: build or buy?

Examples of existing money transfer/payment APIs for P2P transfers

Building your custom payment API for P2P transfers: pros and cons

Benefits of building your own peer-to-peer payment system app

If you already operate mobile payment apps or online P2P websites for your financial institution, integrating it into your customized API could be easy and seamless.

By building your own P2P application you have full control, which implies you can create and perform updates at your own pace, to enhance your clients’ experience.

Software designed with your needs in mind can permit your staff to work faster and smarter.

By designing your own innovative solution well suited for your particular business tasks, you get the potential to beat the competition. Challenges of building your own P2P app

To build the best custom money transfer application, you must first assemble a stellar development team. It’s not an easy task to find a strong software development team with the essential knowledge & necessary skills to construct a custom-made payment API.

Marketing your new app on the market featuring fierce competition is as well not an easy task to accomplish.

Building a payment API from scratch also comes with the need for massive amounts of money and a lot of time.

Think about the entire development process, licenses, regulations, partnerships, and all the things you need to handle.Key features of a P2P payment API to look for

Security

Speed

Rapid payment in peer-to-peer payment system exchanges can altogether profit members by enabling them to screen their monetary positions and track their spending. Payer control

Universality

Ease of use

For illustration, in an effective and simple-to-use P2P API, a sender simply presents the email or cellphone number of who they wish to ship money to and the quantity they need to ship. Customer support

Mobile payments

A quality P2P API should thus allow for easy integration with various mobile applications.Multi-currency

Easy payment methods integration

Reliability

Self-Service Account Creation

Bottom line

Fast-track your money transfer system launch

Neobank software that scales with you