Digital payment methods such as cards, online payments, and mobile wallets have become standard across most industries. As transaction volumes grow, businesses need reliable ways to accept payments, manage processing, and ensure fast settlement.

Merchant services providers play a central role in this process, acting as the operational layer between merchants, acquiring banks, and payment networks.

What is a merchant services provider?

A merchant services provider (MSP) enables businesses to accept and process electronic payments, including card, online, and mobile transactions. These providers coordinate payment authorization, routing, and settlement, ensuring that transactions move securely between all parties involved.

The provider a business chooses directly impacts transaction costs, settlement timelines, and overall reliability of payment operations. This article explains how merchant service providers work, what types exist, and how to choose the right provider depending on your payment model.

While many businesses rely on third-party merchant service providers, others build their own payment infrastructure to gain more control over transaction flows, fees, and integrations using platforms like SDK.finance.

Key Functions of a Merchant Services Provider

Merchant services providers (MSPs) offer the infrastructure that enables businesses to accept and manage electronic payments. Their role spans several essential functions within the payment processing chain.

1. Establishing Merchant Accounts

MSPs facilitate the setup of merchant accounts, which are specialised accounts where funds from card payments are temporarily held before being settled into a business’s bank account.

2. Providing Payment Gateways

For online transactions, MSPs supply or integrate with payment gateways that securely capture, encrypt, and transmit customer payment data for authorisation.

3. Handling Transaction Processing

They coordinate the full transaction lifecycle — from sending authorisation requests to routing responses and settling funds between parties.

4. Ensuring Security and Compliance

MSPs help businesses meet regulatory and data security requirements such as PCI DSS. They also provide fraud prevention and chargeback management tools.

5. Offering Reporting and Reconciliation Tools

Many providers include dashboards and APIs that allow businesses to track payment flows, fees, and settlements for financial management and reconciliation.

6. Enabling Multichannel Payment Acceptance

Modern MSPs support payments across multiple channels, including point-of-sale, e-commerce, mobile apps, and contactless systems, to accommodate various customer preferences.

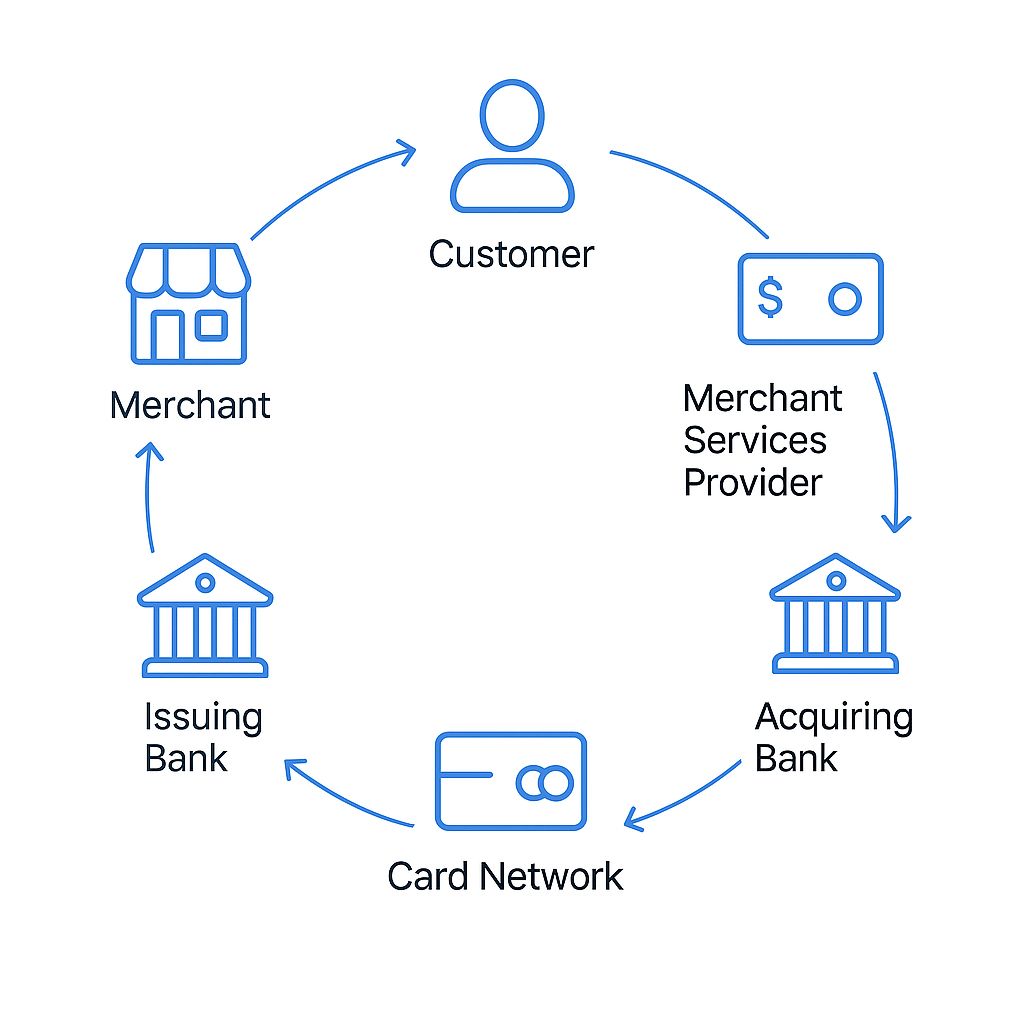

How the Merchant Services Ecosystem Works

A merchant services provider acts as an intermediary between businesses, acquiring banks, card networks, and issuing banks. It ensures that payment transactions are processed quickly and securely, usually within a few seconds.

Key Participants in the Ecosystem

-

Merchant – The business accepting payments

-

Customer – The cardholder making a purchase

-

Merchant Services Provider (MSP) – The intermediary enabling payment acceptance

-

Acquiring Bank – The bank that receives card payments on behalf of the merchant

-

Card Network – Visa, Mastercard, etc., facilitating communication between banks

-

Issuing Bank – The bank that issued the customer’s payment card

Behind every tap or online checkout, there’s a chain of interactions across multiple parties:

Step-by-Step Transaction Flow

-

Payment Initiation

The customer initiates a payment by tapping their card on a POS terminal or entering their card details online. -

Data Transmission to Payment Processor

The merchant services provider captures the payment information and transmits it to the acquiring bank or payment processor. -

Routing to Card Network

The acquiring bank sends the transaction request to the relevant card network (e.g. Visa, Mastercard, Amex). -

Forwarding to Issuing Bank

The card network routes the transaction to the customer’s issuing bank (the bank that issued the payment card). -

Authorisation Decision

The issuing bank checks the customer’s account for available funds and verifies the transaction. It either approves or declines the request. -

Response Routing

The authorisation result is sent back through the card network to the acquiring bank and the merchant services provider. -

Merchant Notification

The merchant receives the response via the payment terminal or gateway. If approved, the terminal displays a confirmation message and approval code. -

Funds Settlement

The customer’s account is debited, and the funds are transferred (after settlement and fees) to the merchant’s account, usually within 1–2 business days, depending on the provider and setup.

This streamlined process is designed for speed, but it involves multiple checks, verifications, and security measures to reduce fraud and ensure funds flow correctly. The MSP plays a central role in orchestrating all of this behind the scenes.

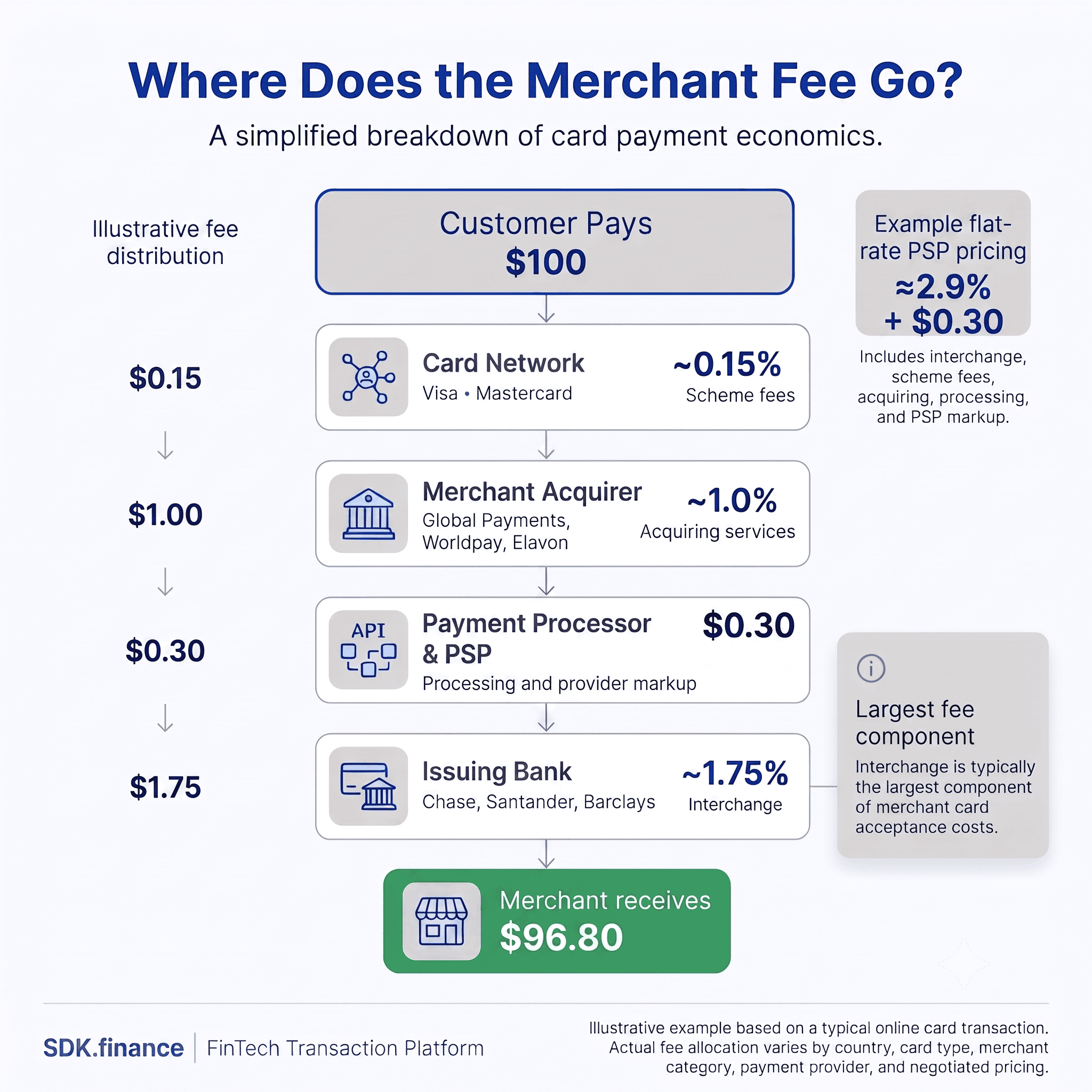

How merchant payment fees are distributed

When a customer pays by card, the merchant does not typically receive the full transaction amount. The total merchant fee is distributed among several participants, including the issuing bank through interchange fees, the card network through scheme fees, the acquiring bank, and the payment processor or PSP. The exact cost depends on the country, card type, merchant category, transaction channel, and the pricing agreement with the provider.

Types of merchant services providers

Different providers offer different merchant payment services so you can choose the best payment processing solutions for your type of business. According to different functions, there are three of the most common types of services available through merchant providers: merchant accounts, payment services, and payment gateway providers.

Merchant service provider vs payment gateway

Merchant service providers and payment gateways are two important components of the payment processing ecosystem, each performing different tasks. A merchant service provider, also known as a payment processor, acts as an intermediary between businesses and the various parties involved in the payment process. They enable businesses to accept electronic payments and handle the authorization, processing, and financing of transactions.

On the other hand, payment gateways act as secure channels for the transmission of payment information between customers, businesses, and merchant service providers. They encrypt and route payment data, ensuring the secure transmission of sensitive information. Payment gateways also provide additional functionality such as fraud detection and integration with e-commerce platforms. Together, these components work in tandem to enable businesses to process payments smoothly, securely, and efficiently.

Merchant account providers

These entities are the most popular service providers. They offer a merchant account specifically designed for businesses to accept credit and debit card payments. Merchant account providers are extremely helpful for companies that make a large number of transactions with credit and debit cards. With this model, the processor (or the Bank) issues a Merchant ID, that is exclusive to your business and no one else.

Offering access to exclusive merchant accounts, they allow businesses to control payments and get benefits from quick access to funds and low transaction fees.

They also can provide other merchant payment services to enhance your business’s payment methods, including:

- Credit card terminals

- Mobile card readers

- POS systems

Merchant accounts can also have the following fees: monthly minimum, billing, authorization, transaction, customer service, and maintenance.

Launch your digital bank in weeks, not years

Talk to Our TeamPayment services providers

While large companies have merchant account providers, there is an alternative for small businesses that do not need an additional account. Payment service providers (PSPs, third-party processors, or aggregators) enable businesses to accept digital payments both offline and online, without having a dedicated merchant account.

For example, you do not need to have a unique merchant ID number, because your account is aggregated with other merchants. PSPs simplify payment processing for small business owners, despite having longer processing times and higher overall costs.

What is the difference between a merchant service provider and a payment service provider?

Despite the similar functions, there is a key difference between a merchant services provider and a payment services provider. Payment service providers consolidate multiple businesses under a single account, while merchant services providers establish a separate account and identification number for each business they serve.

The table below illustrates the difference between a merchant services provider and a payment services provider:

| Characteristics | Merchant service provider | Payment service provider |

| Description | Merchant service providers offer an account specially designed for businesses to accept credit and debit card payments. | Payment service providers offer your business the ability to accept credit card payments without a dedicated merchant account. |

| An approvement process | Involves a verification and compliance process that may take weeks. | Typically instant approval. |

| Merchant account setup | The underwriting process varies by the bank account provider and can have different requirements for opening an account. | Payment services providers provide easier ways to set up. PSPs are free to sign up for and there is minimal documentation that is required to activate your account. |

| Pricing | More complex fees include: flat-rate, interchange-plus, and tiered pricing | Fewer fees to worry about in general |

| Processing volume | Negotiable limits on transaction size and processing volume. | Can offer strict limits on transaction size and processing volume. |

While PSPs consolidate a variety of different merchants under a single umbrella account, merchant services providers offer a dedicated account for accepting electronic payments. Each of these methods provides debit and credit card transactions but has specific functionality to meet your business needs.

Payment gateway providers

A payment gateway provider is a kind of merchant service provider that authorizes the processing of card or direct payments. It serves as a mediator between the business and the customer, allowing businesses to accept online transactions through a secure network.

Payment gateway providers can offer more than a simple function of enabling your business to process credit and debit card transactions over the Internet. They also provide a high level of security and fraud prevention so that both you and your customers can conduct online financial transactions seamlessly.

Payment gateway providers offer the following features: fraud detection, 24/7 customer support, and international payment processing, recurring billing. It is also important to ensure that the payment gateway is Payment Card Industry (PCI)-compliant.

Merchant services products

The majority of merchant payment services offer a wide range of services and products for businesses to accept and process payments. Here are the most common categories of merchant services products:

Merchant accounts

A merchant account is a type of bank account that is specially made for business purposes to accept and process electronic transactions by debit or credit cards from customers. This account serves as a temporary holder for card payments, acting as an agreement between the business (also known as an acceptor) and an acquiring bank.

The merchant account stores funds from processed transactions. Those funds are then transferred by your provider into a business account that you specify, such as a business checking account.

Credit card terminals

Credit card terminals, also called electronic data capture machines, are digital products that allow customers to physically swipe, dip, or tap a credit card to make a payment. These machines connect to the merchant service provider and process and validate transactions. There are many different sizes and forms of credit card terminals: from simple magstripe swipers to handheld terminals.

Point-of-sale (POS) systems

A point-of-sale or POS system usually consists of software and hardware that accept payments. It also can manage a company’s daily operations and processes: processing sales, producing reports, monitoring inventory, managing staff, reconciling tips and commissions, accepting gift cards, setting up loyalty programs, and enabling point-of-sale financing options for customers.

Mobile payment systems

The smartphone or tablet can function as a credit card terminal with mobile payment systems. They consist of a mobile card reader that connects to your mobile device and an application to communicate with your provider’s processing network. These mobile payment systems provide online transactions in any place, where there is an internet connection.

Payment gateway

A payment gateway is software that enables you to accept and process safe credit card payments online through your website or e-commerce store. In essence, the payment gateway replaces the credit card terminal. Customer credit card information is gathered and encrypted by a payment gateway for later processing.

Virtual terminals

A virtual terminal is software that enables businesses to accept payments made with a credit card, without the card having to be physically present. It is a program that transforms your computer into a credit card terminal. An optional USB-connected card reader can be used to swipe cards or manually input transactions. Businesses that accept orders over the phone or by mail and don’t have an e-commerce website are most likely to use virtual terminals.

How to Choose the Right Merchant Services Provider?

Choosing the right merchant services provider can be a daunting task. Here are some steps to follow:

- Assess your business needs: Determine your business needs and requirements, including the types of payments you need to process and the level of security you require. This assessment will help you identify the features and services that are most important for your business.

- Research providers: Research different merchant services providers, considering their offerings, pricing, and reputation. Look for providers with a track record of reliability and customer satisfaction.

- Evaluate security and compliance: Evaluate the provider’s security and compliance measures, ensuring they meet industry standards. This includes checking for PCI DSS compliance and other relevant certifications.

- Consider integrations and partnerships: Consider the provider’s integrations and partnerships, ensuring they align with your business needs. Look for providers that can seamlessly integrate with your existing systems and offer valuable partnerships.

- Evaluate customer support and reporting tools: Evaluate the provider’s customer support and reporting tools, ensuring they meet your business needs. Look for providers that offer robust support and detailed, customizable reporting.

- Compare pricing: Compare the provider’s pricing, considering the costs of transaction fees, monthly fees, and any additional charges. Ensure that the pricing structure is transparent and fits within your budget.

- Read reviews and ask for referrals: Read reviews and ask for referrals from other businesses, ensuring the provider has a good reputation and can meet your business needs. This feedback can provide valuable insights into the provider’s performance and reliability.

By following these steps, you can choose a merchant services provider that meets your business needs and helps you optimize your payment processing.

While merchant service providers simplify payment acceptance, they also introduce constraints around pricing models, settlement flexibility, and system-level control. These limitations become more visible as transaction volumes grow or when businesses operate across multiple markets.

In such cases, companies often move towards building their own payment infrastructure, combining acquiring, payment routing, and ledger management into a unified system.

SDK.finance Merchant Service Provider Solution

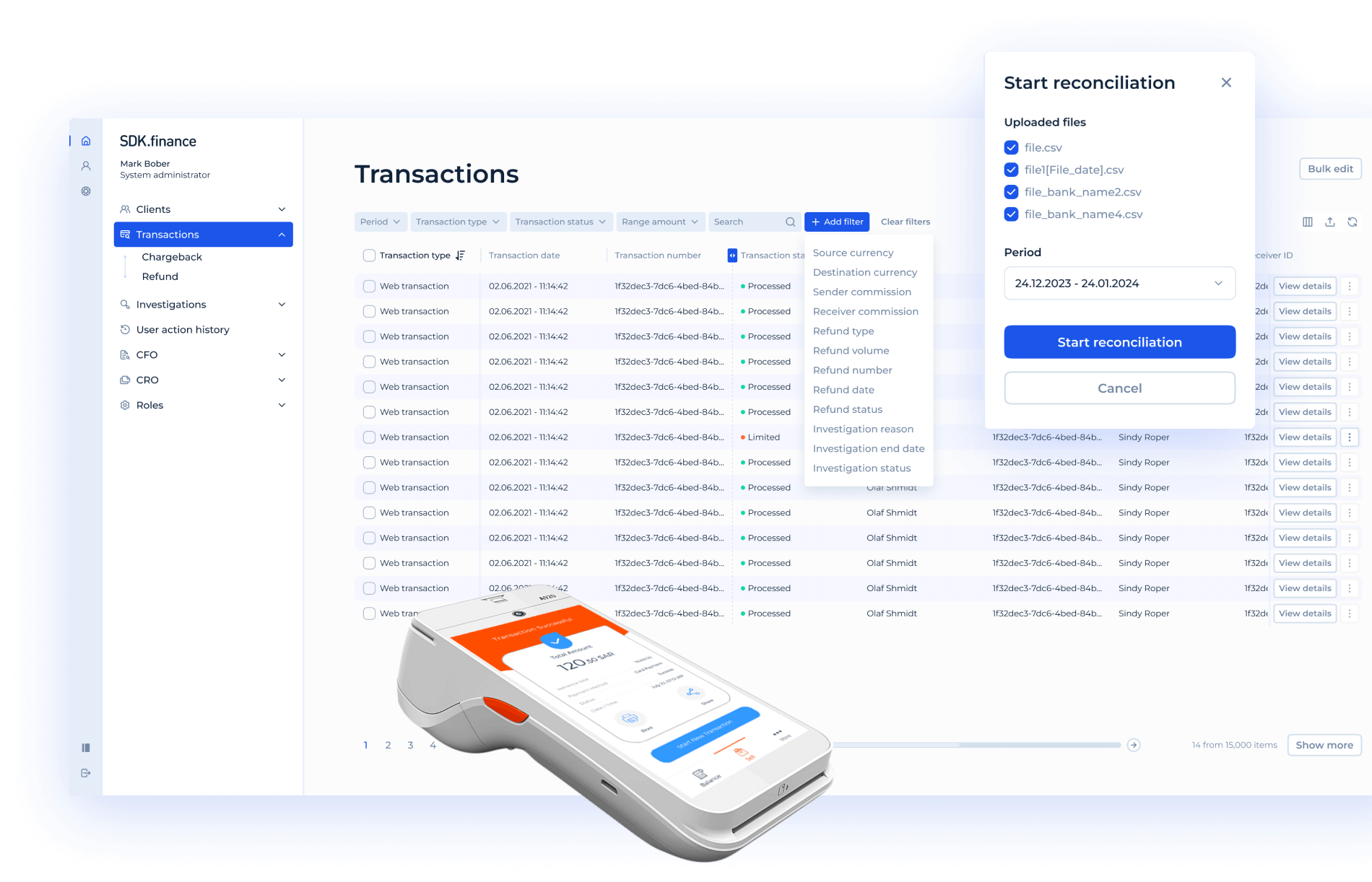

With the SDK.finance payment acceptance platform for MSPs and PSPs, you can empower the business and increase revenue by offering a complete stack of online and offline services for merchants. Our transaction core has ledgering functionality, so it can be customized to collect the transaction information from the POS, link it to a specific merchant account, and track the transaction status in the bank until the money is in the merchant’s account.

SDK.finance payment solution features include:

- Customer onboarding

- Transactions management

- Online POS

- Payment initiation and acceptance

- Regular payouts

- Refunds initiation

- Merchant’s digital wallet

- Roles and permissions management

SDK.finance has experience in transforming a core transaction accounting system through our payment software. Our technical team has integrated the ledger layer software with a leading MENA payment solution provider, allowing our customer company to see the entire payment cycle in detail, from acceptance and reconciliation to settlement and payout ensuring transparency for the money flow and daily accounting.

Watch the Merchant Portal powered by SDK.finance demo video:

As a result, SDK.finance helped to reimagine the technology and processes behind the customer company’s accounting system and launch a revitalized scalable future-proof solution. Through cooperation with SDK.finance, a new accounting system based on the ledger layer software is now integrated with an extensive network of the customer’s POS terminals across several countries in the MENA region.

Create your digital banking solution in weeks

Talk to Our TeamWrapping up

The merchant services provider is the financial partner that helps businesses to operate, facilitate transactions and provide different payment services that meet companies’ and customers. They act as an intermediary between banks, businesses and customers. The rise of digital payments, payment causes the need to ensure seamless transactions and improve operational efficiency.

SDK.finance provides a payment acceptance software platform for MSPs and PSPs that helps them increase business productivity and quickly grow revenue. With our finance platform, you can offer online and offline payment acceptance services to merchants, without having to start from scratch. Using the SDK.finance merchant payment processing platform, you’ll shorten time-to-market and save resources on software development. Contact us to build your payment platform based on our fintech software.