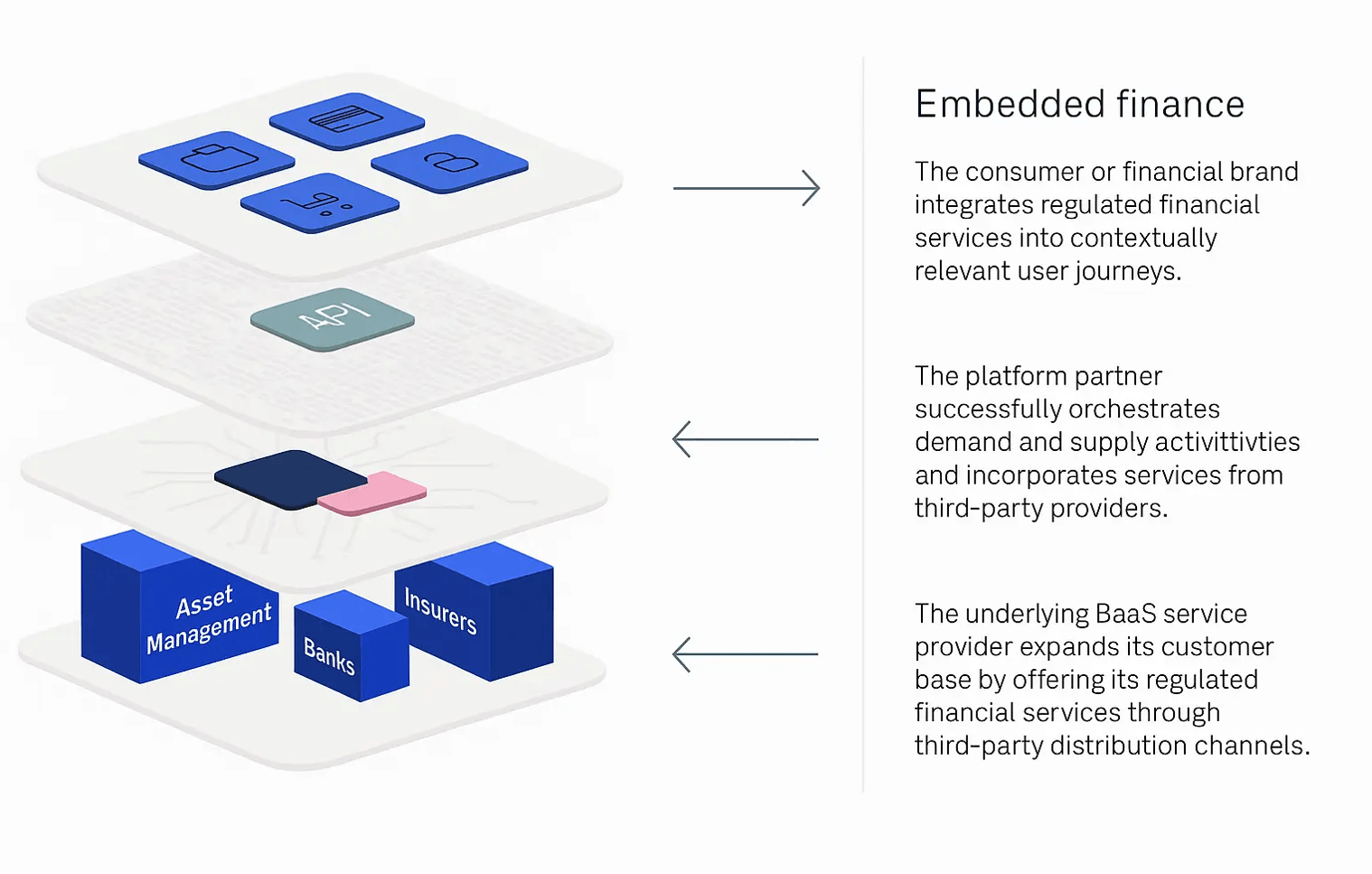

Embedded finance has shifted from an optional capability to a core expectation. Companies outside traditional finance now want to offer banking services: accounts, payments, cards, and financial workflows within their own products. To support this, they need payment infrastructure that delivers banking services through secure, predictable, and well-structured API infrastructure. This is where a core banking API becomes essential. Core banking APIs and application programming interfaces are shaping the future of embedded finance, transforming traditional banking into more integrated, real-time services.

FinTech-built systems are now taking the lead, offering API-first platforms that can be embedded directly into digital services. API banking enables a wider range of financial products and services, allowing businesses to unlock new revenue streams by integrating financial solutions into their ecosystems. This article explains how a core banking API works, why FinTech architecture is better suited for embedded finance, and why SDK.finance stands out among available API banking vendors.

A core banking API provides access to essential financial operations through a set of programmable endpoints. Modern core banking APIs deliver a wide range of core banking functionalities and banking capabilities, including identity verification, insurance, and accounting,payment processing, enabling secure, compliant, and flexible integration of financial services. These APIs empower businesses to build, offer, and manage innovative financial products efficiently.

Instead of interacting with a traditional monolithic core systems, teams rely on APIs gateway to manage:

For embedded banking, this API layer becomes the backbone that connects financial capabilities with applications such as marketplaces, SaaS tools, mobility platforms, healthcare, telecom services, or retail ecosystems.

Fintech platforms built with an API-first mindset differ from legacy banking systems in several critical ways. Fintech-origin APIs are enabling non financial companies and external platforms to develop and deliver innovative financial services without the need to build their own infrastructure.

This approach empowers businesses outside the traditional financial sector to embed banking functions directly into their products, expanding their offerings and enhancing customer engagement. By creating seamless user journeys and improving customer experiences through embedded finance, these APIs are transforming how financial services are accessed and integrated.

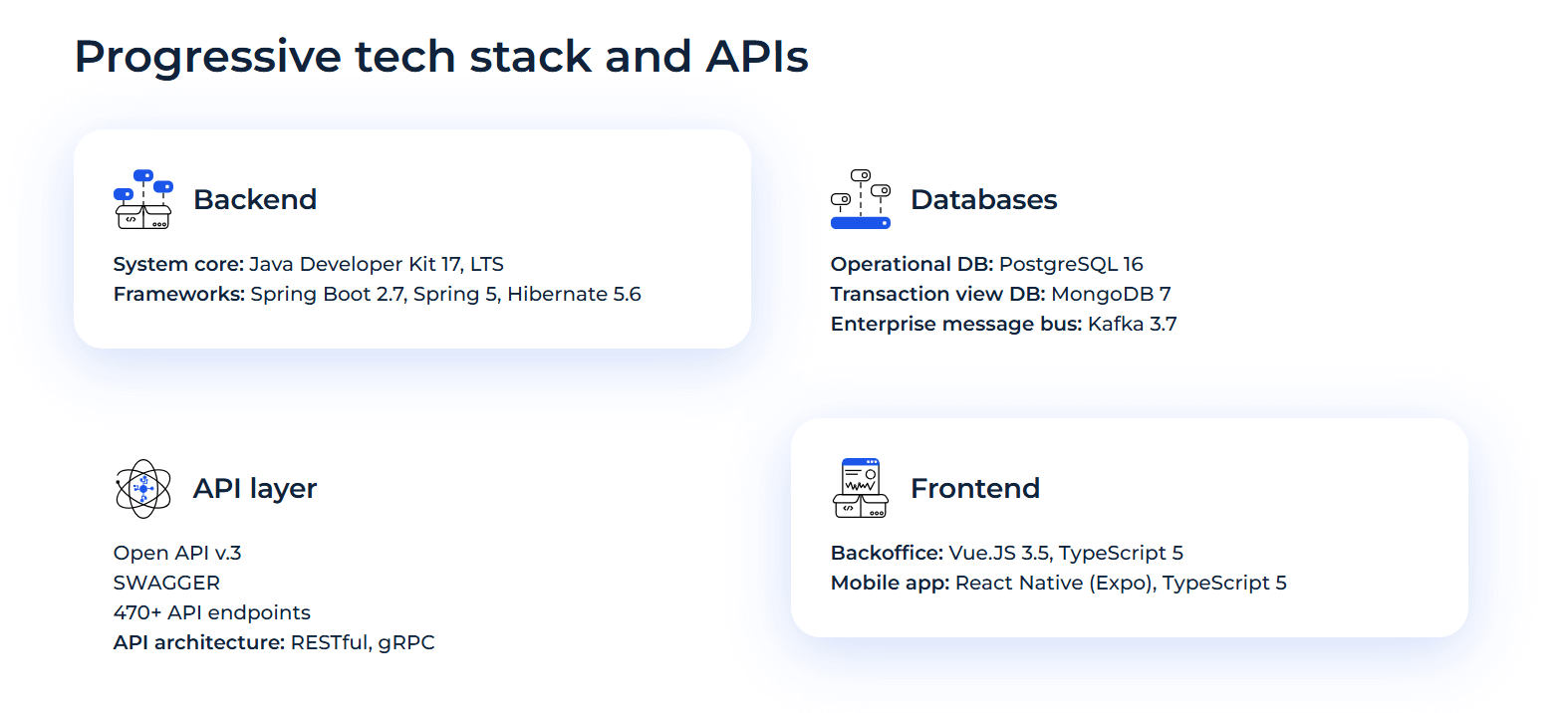

FinTech cores use RESTful APIs, webhooks, and standardised data models to deliver integrated banking solutions. This reduces friction for engineering teams building banking features into existing products.

Companies often integrate additional operational tools such as CRMs or Lead Management Software through the same API gateway, ensuring a unified flow across product, compliance, and customer-facing processes.

Pre-built modules such as account orchestration, KYC connectors, payout engines, and ledger layers, payments, combined with robust APIs, enable businesses to launch new services rapidly – often in weeks or months.

Each banking capability – accounts, payments, FX, compliance, card issuing logic – can operate independently. This lets non-financial companies focus on the customer experience and introduce or expand features without rewriting the entire stack, and enables them to create branded financial products tailored to their needs.

FinTech cores typically process thousands of transactions per second, supporting smart routing and advanced payment processing for efficient, real-time operations. They integrate with payment rails, card networks, alternative payment methods, and settlement and reconciliation systems.

From loyalty points to digital assets and multi-merchant structures, FinTech engines support a variety of embedded finance use cases beyond traditional banking, enabling platforms to integrate wallets, accounts, payouts, card issuance, and compliance through flexible APIs. These engines can accommodate use cases that legacy cores do not natively support.

Multiple core banking providers support embedded finance through API-based platforms. BaaS providers deliver banking as a service, acting as the technical backbone that enables a variety of service models for embedded finance and seamless integration of financial products into third-party platforms. Each serves different segments and regulatory markets.

It is often chosen by fintech teams aiming to launch banking features in the US without building their own compliance stack or banking relationships.

It is typically used by companies that need a ready-made framework for embedding card issuing and payment capabilities across European markets.

The platform is selected primarily by mid-sized and large banks transitioning away from legacy systems toward API-based, scalable architecture.

It is generally selected by large banks and international financial organisations that require extensive regulatory coverage and a broad functional stack for complex, multi-market operations.

| Vendor | Embedded Banking Use Cases | Delivery Model | Strengths |

|---|---|---|---|

| SDK.finance | Digital wallets, neobanks, PSPs, money transfers, embedded finance, embedded payments, super apps, FX, multi-asset accounts | SaaS or full source code licence | API-first, 570+ endpoints, modular design, PCI DSS Level 1, transactional ledger, high performance, full code ownership, supports merchants |

| Mambu | Digital banks, lending products, deposits, embedded finance use cases | SaaS | Composable core, strong lending/deposit capabilities |

| Unit | Wallets, cards, bank accounts, payouts (US), embedded payments, embedded finance use cases | API + BaaS | Fast US launches, combined tech and compliance, supports merchants |

| Railsr | Cards, payments, account issuing, embedded payments, embedded finance use cases | SaaS + BaaS | Card issuing ecosystem in Europe |

| Finxact | Enterprise banking modernisation, embedded finance use cases | SaaS | Scalable cloud architecture for large institutions |

| Temenos | Tier 1–2 banks, global deployments, embedded finance use cases | SaaS / on-premise | Comprehensive functionality and compliance depth |

SDK.finance stands out because it combines the benefits of a ready-made FinTech core with the flexibility typically associated with custom systems. Key differentiators include:

For companies building embedded payments products – wallets, neobanks, multi-merchant systems, telecom money, or payment platforms – SDK.finance provides the infrastructure needed to move quickly while maintaining long-term control.

Proud to announce that SDK.finance is the best FinTech startup 2015! Central European Startups Awards has… Read More

On November 10, SDK.finance was presenting demo at Bank Innovation Israel 2015 DEMOvation challenge. Bank Innovation… Read More

Great news! SDK.finance is selected for the €20.000 cash prize pitch competition at Execfintech! After… Read More

On March 8, CTO SDK.finance Pavlo Sidelov and CEO Alex Malyshev were attending one of the… Read More

On March 30, SDK.finance has been selected as a finalist for Red Herring's Top 100 Europe award,… Read More

Money 20/20, the cutting-edge FinTech conference, was held April 4 – 8 in beautiful Copenhagen… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}