International payments rely heavily on accurate account identification, and for PSPs, EMIs, and other payment businesses, this accuracy directly affects settlement timelines, reconciliation quality, compliance, and customer experience. One of the key tools that enables predictable cross-border money movement is the IBAN. IBAN is an international standard for bank account numbers, designed to unify and simplify cross-border payments.

Although IBANs are widely used across Europe, the Middle East, and other regions, many payment providers still face operational complexity when working with different domestic formats, reconciling various national bank account numbers, bank partners, and virtual IBAN schemes.

This guide explores what an IBAN is, how it works, and why it plays such a central role in global payment operations and modern FinTech infrastructures.

The International Bank Account Number (IBAN) is a unique alphanumeric code designed to streamline the identification of bank accounts across national borders. As global commerce and cross border payments have grown, the need for a standardized system to identify bank accounts has become essential for financial institutions, payment service providers, and businesses alike.

The IBAN system was developed to reduce errors and delays in international transactions by providing a single, internationally recognized format for bank account identification.

IBAN stands for International Bank Account Number and is used alongside the Bank Identifier Code (BIC) or SWIFT code to ensure that money transfers are routed accurately to the correct bank and account. By consolidating key account details into one string, the IBAN system simplifies the process of sending and receiving funds internationally, making it easier for banks and payment providers to process cross border payments efficiently.

Today, more than 70 countries have adopted IBANs, making them a cornerstone of international banking and financial operations. For any business or financial institution involved in global money movement, understanding and utilizing the IBAN system is critical for accurate and secure bank account identification.

An IBAN (International Bank Account Number) is a standardised, globally recognised identifier for a bank account. The IBAN number identifies an individual account within a bank, making it essential for international money transfers. It consolidates all the necessary routing information into a single string, reducing the risk of errors and accelerating international transfers.

For PSPs and EMIs, the IBAN is not just a compliance requirement. An IBAN consists of a country code, check digits, and a unique account number, which together ensure accurate identification of the recipient’s account. It is a foundational element of how funds are allocated, traced, and settled across borders. Whether the business sends payouts to merchants or enables users to receive international transfers, the IBAN ensures the payment lands in the correct account without additional clarification or manual checks. IBAN numbers are used by businesses and financial institutions for compliance and operational efficiency.

For regulated financial institutions and payment companies, even a small mistake in account identification can result in delays, chargeback-like investigations, costly manual work, and friction for business clients, making IBAN validation essential for ensuring accuracy. The IBAN’s built-in validation, including the use of a check digit for error detection, and its standardised structure significantly cuts the risk of misdirected transactions.

IBAN-standardised routing means PSPs and EMIs can offer more predictable settlement windows, which matters for high-volume merchants, gig platforms, FX services, and payroll providers.

KYC, AML, and payment screening workflows depend on clear account identification. IBAN reduces ambiguity, helping compliance teams validate destination accounts faster.

For providers handling thousands of incoming transfers daily, structured identifiers are essential. With IBANs, reconciliation steps are streamlined because the account and bank identifiers are already embedded in the transfer.

PSPs and EMIs serving internationally distributed merchants or corporate clients rely on IBANs to operate across SEPA, SWIFT, and other corridors without relying on multiple incompatible domestic formats. However, not all banks or regions use the IBAN system, so alternative methods such as SWIFT may be required for some international transfers. In cross-border operations, overseas banks identify accounts using the IBAN code to ensure accurate routing and verification of account details during international transactions.

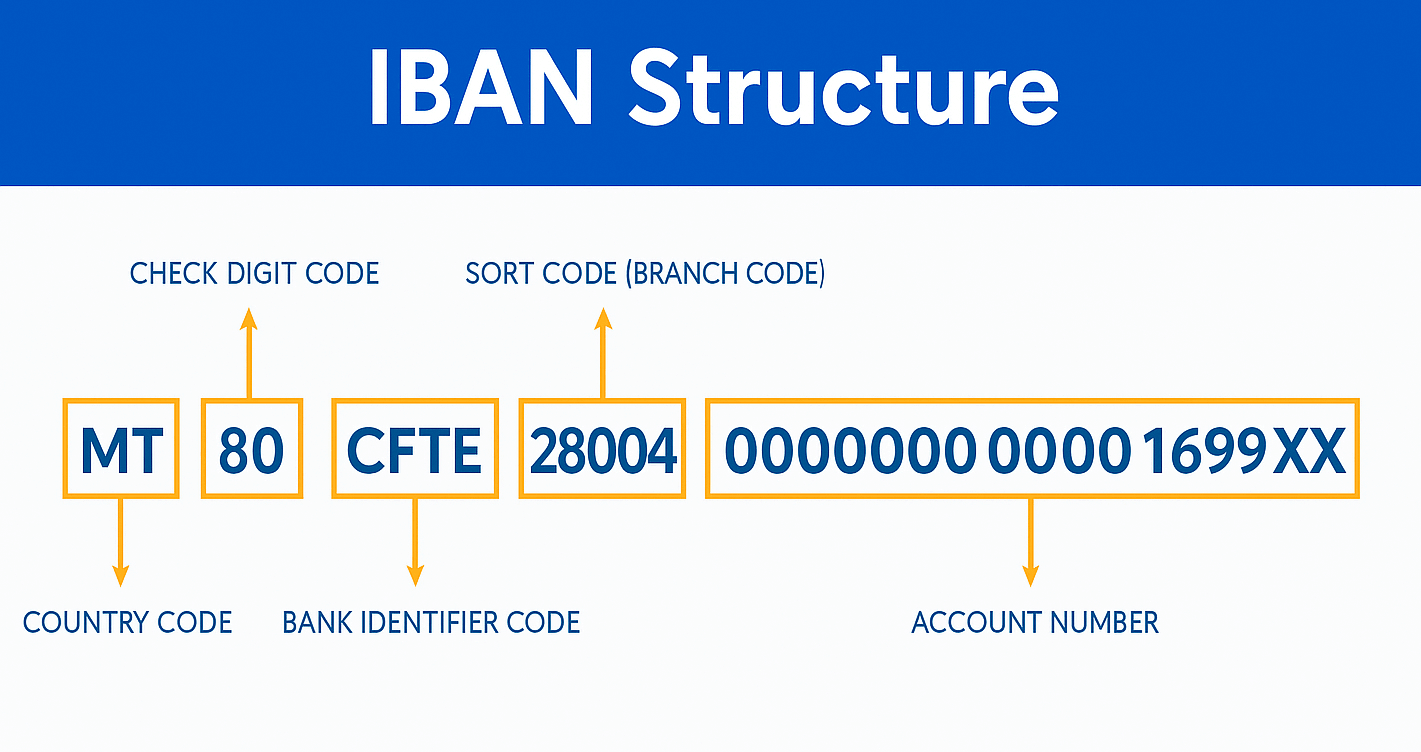

Although IBAN formats vary by country in terms of length and character composition, every IBAN follows the same high-level structure as defined by international standards.

The structure includes a country code, two check digits (known as IBAN check digits, which are calculated using algorithms like ISO 7064 MOD-97-10 to ensure the validity and integrity of the IBAN), and a Basic Bank Account Number (BBAN):

Two letters, known as the two digit country code at the start of the IBAN, designating the account’s country of origin.

Two numbers produced through an algorithm that verifies whether the IBAN is valid. This prevents mistyped account details from entering the banking system.

The remainder of the IBAN, defined by each country’s standards. It typically includes:

The bank code within the BBAN helps identify a specific bank involved in the transaction, ensuring accurate routing, especially for international transfers. For payment companies operating across multiple countries, understanding the BBAN structure is essential for building validation logic, routing rules, and automated reconciliation workflows.

PSPs and EMIs often need to collect both the IBAN and the SWIFT/BIC from their merchants or users. SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication, and it plays a crucial role in international banking by enabling secure communication between banks for global transactions. These codes complement each other:

Both are required for international transfers. In practice:

This combination is central to predictable settlement flows, especially in B2B corridors with high regulatory scrutiny.

Platforms issuing high-volume payouts (marketplaces, gig platforms, FX platforms) rely on accurate IBANs to ensure same-day or next-day settlement to merchant accounts.

Payroll services rely on IBANs to reach contractors and employees across borders with minimal transfer failures.

Corporate clients using PSP or EMI systems to pay overseas vendors, especially when making payments to a foreign bank account using IBAN, need efficient IBAN-based routing to avoid delays.

Payment providers offering local accounts rely on IBANs for predictable inbound transfers, whether through SEPA, SWIFT, or open banking rails.

Fewer failed transfers means fewer manual investigations, support tickets, or recovery procedures — a direct operational benefit for PSPs and EMIs.

For businesses, an IBAN account means having the ability to receive and send cross-border funds using a unified account identifier. International bank account numbers (IBANs) are used to identify accounts for cross-border payments, standardizing bank account formats internationally and reducing errors in international wire transfers.

For PSPs and EMIs, it also enables:

Whether the IBAN belongs to a traditional bank or is issued through a BaaS partner, it becomes a key component of the company’s money movement infrastructure. The IBAN can typically be found on a bank statement provided by the bank.

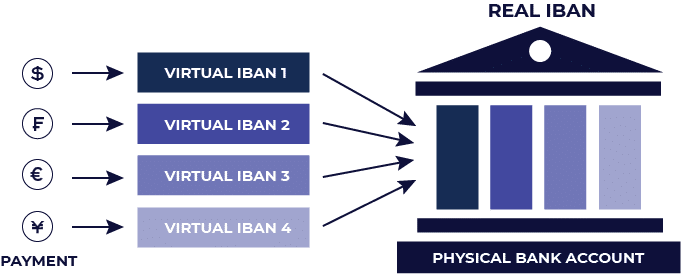

Virtual IBANs (vIBANs) are widely adopted across FinTech ecosystems due to their flexibility. Designed to meet the needs of diverse financial environments, virtual IBANs enable efficient and adaptable solutions for international transactions.

A virtual IBAN behaves like a normal IBAN but maps to a central or pooled account. This allows PSPs and EMIs to:

Each merchant, client, or transaction category can receive its own dedicated vIBAN.

Incoming transfers automatically match to the right ledger entry.

Merchants operating internationally can receive funds as if they had local accounts in multiple jurisdictions, without opening physical accounts.

Instead of maintaining dozens of accounts across different banks, PSPs and EMIs can operate one settlement account with many virtual identifiers.

Platforms can issue virtual IBANs to their users programmatically, enabling account-like experiences without becoming a bank.

Virtual IBANs have become a standard feature for modern payment businesses due to their efficiency and adaptability.

As embedded finance grows, more companies want to issue IBANs to their customers – whether to support B2B payouts, cross-border wallet top-ups, or global merchant settlements.

The registration authority, such as SWIFT, is responsible for maintaining and updating IBAN standards to ensure compliance and interoperability across countries. The designated payment authority, often the national central bank or central bank, defines and registers the IBAN format for each country, ensuring it meets both local and international requirements.

The European Committee for Banking Standards (ECBS) and the European Union have played a key role in harmonizing banking standards and mandating IBAN adoption across EU member states, facilitating standardized cross-border transactions. The importance of banking standards is critical for global interoperability and efficient payment processing.

Payment businesses can integrate IBAN issuing via APIs to:

The result is a scalable account infrastructure that supports B2B money movement in multiple regions without building a banking backend from scratch.

IBANs are a vital component in safeguarding bank account security during international payments. By providing a standardized method for identifying bank accounts, the IBAN code helps ensure that funds are transferred to the correct bank and account, minimizing the risk of errors or fraud.

The inclusion of check digits within the IBAN structure enables automated validation, helping banks and payment providers detect mistyped or incorrect account numbers before a transaction is processed. This reduces the likelihood of misdirected payments and enhances the overall security of cross-border financial transactions.

In addition, IBANs are often used in conjunction with online banking security measures, such as two-factor authentication, to provide an extra layer of protection for bank accounts. For businesses and financial institutions handling international payments, the use of IBANs is a key step in ensuring that account numbers are correct and that funds reach the intended beneficiary securely and efficiently.

The IBAN Registry serves as the authoritative catalog of countries and territories that have adopted the IBAN standard, and is maintained by the Society for Worldwide Interbank Financial Telecommunication (SWIFT). This registry outlines the specific IBAN format and requirements for each participating country, including the country code, check digits, and the structure of the Basic Bank Account Number (BBAN). By providing these details, the IBAN Registry ensures that financial institutions worldwide can interpret and validate IBANs correctly, supporting seamless cross-border payments and financial transactions.

The IBAN format is governed by the International Organization for Standardization (ISO) under the ISO 13616 standard, which guarantees consistency and interoperability across different banking systems and jurisdictions. SWIFT, as the official IBAN registrar, is responsible for updating and publishing the IBAN Registry, ensuring that all participating countries adhere to the latest specifications. This standardization is essential for supporting a wide range of financial activities, including direct debit, credit transfers, and other international transactions. For payment providers, banks, and businesses operating globally, the IBAN Registry is a critical resource for ensuring compliance and operational efficiency in international banking.

SDK.finance provides a modular digital payments and wallet platform designed for PSPs, EMIs, and enterprise FinTech teams that need reliable account infrastructure with IBAN support. SDK.finance ensures compliance with international standards for IBAN processing, including standardized formats and protocols to facilitate secure and efficient cross-border transactions.

Our platform enables:

Thanks to PCI DSS Level 1 certification, 470+ APIs, and a flexible architecture, SDK.finance helps payment businesses launch IBAN-based services faster and with full operational control. PSPs and EMIs use the platform to streamline settlements, reduce operational costs, and scale their B2B payment operations across regions with a robust transaction processing system.

Proud to announce that SDK.finance is the best FinTech startup 2015! Central European Startups Awards has… Read More

On November 10, SDK.finance was presenting demo at Bank Innovation Israel 2015 DEMOvation challenge. Bank Innovation… Read More

Great news! SDK.finance is selected for the €20.000 cash prize pitch competition at Execfintech! After… Read More

On March 8, CTO SDK.finance Pavlo Sidelov and CEO Alex Malyshev were attending one of the… Read More

On March 30, SDK.finance has been selected as a finalist for Red Herring's Top 100 Europe award,… Read More

Money 20/20, the cutting-edge FinTech conference, was held April 4 – 8 in beautiful Copenhagen… Read More

{kind=link}

{kind=link}