Central Bank Digital Currency (CBDC) is a hot topic in the world of money and payments. This article provides an easy-to-understand overview of what CBDCs are, why they matter, and how they could affect the financial market.

A CBDC (Central Bank Digital Currency) is a digital form of a country’s official currency issued and regulated by its central bank, carrying the same value and backing as the nation’s physical cash.

CBDC is essentially state-backed electronic money. Unlike the money in your bank account, which technically belongs to a private bank until you withdraw it, a CBDC is a direct claim on the central bank.

In other words, it’s like having digital notes and coins guaranteed by the government, stored on your phone instead of in your pocket. Here is a helpful video that defines CBDC clearly and in an easy-to-understand way:

The idea of CBDCs didn’t come out of nowhere. It’s part of a bigger journey in how we use money:

In the 1990s and 2000s, online banking and card payments made cash less central to everyday life.

In 2009, Bitcoin appeared, showing the world that digital currencies could exist outside banks.

By 2014, China’s central bank began experimenting with the digital yuan, kickstarting official CBDC research.

In 2020, The Bahamas launched the Sand Dollar, the first nationwide CBDC.

Today, more than 130 countries are looking into CBDCs, and some are already piloting or using them.

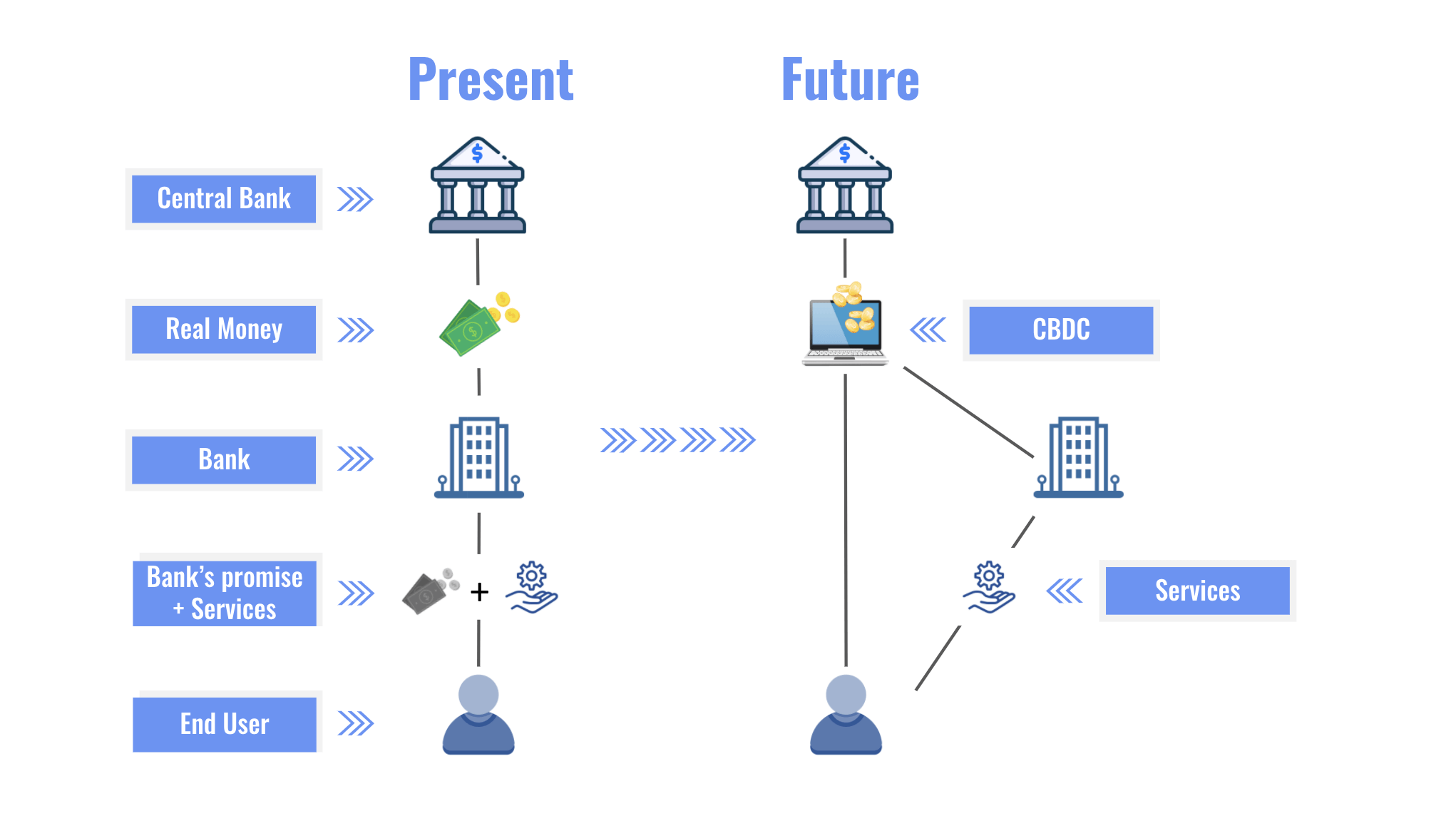

At its core, a CBDC works like digital cash issued directly by the central bank. Instead of holding notes and coins, you would have a balance in a digital wallet or mobile app that represents money guaranteed by the state.

When you pay with CBDC:

The money moves directly between your wallet and the recipient’s wallet.

Transactions are settled instantly on the central bank’s digital ledger.

There is no need for multiple intermediaries, such as commercial banks or card networks, to process the payment.

This is different from today’s digital payments. For example, if you use a debit card at a shop:

The transaction request goes from the shop’s payment terminal to a payment processor (like Visa or Mastercard).

It is then routed to your commercial bank to check if you have funds.

Only then is the payment authorised and settled, sometimes taking a day or more behind the scenes.

CBDCs simplify this process by letting the central bank itself provide the settlement layer. This could mean:

Faster payments, because settlement happens in real time.

Lower costs, since fewer middlemen are involved.

Greater financial inclusion, as people could hold CBDC wallets even without a traditional bank account.

At the same time, commercial banks and payment companies might continue to play important roles, such as providing user-friendly apps, wallets, and services built on top of the central bank’s digital currency.

A medium-sized online electronics store with a monthly turnover of about $500,000 currently pays around 2% of that amount in card and processing fees, which equals roughly $10,000 every month or $120,000 a year. These costs do not directly benefit the business but simply cover the services of intermediaries such as banks and payment networks. After the introduction of a CBDC, however, payments could move directly from the customer’s wallet to the merchant’s wallet without passing through multiple middle layers. If the technical fee were set at just 0.1%, the monthly cost would fall to about $500, or $6,000 per year.

The result would be significant savings:

Monthly savings: $9,500

Yearly savings: $114,000

| Metric | Current System (cards, ~2% fee) | After CBDC (0.1% fee assumed) | Savings |

|---|---|---|---|

| Monthly turnover | $500,000 | $500,000 | – |

| Monthly transaction cost | $10,000 | $500 | $9,500 |

| Yearly transaction cost | $120,000 | $6,000 | $114,000 |

For a medium-sized business, after the introduction of CBDC, this level of savings could mean:

Investing in growth,

Offering lower prices to customers,

Or simply enjoying a more sustainable profit margin.

CBDC is not meant to immediately replace cash. Most central banks plan for digital money and physical cash to exist side by side for now. Cash offers privacy and accessibility, while CBDC can bring convenience and efficiency.

CBDCs are sometimes compared to cryptocurrencies like Bitcoin, but the differences are big:

Who’s in charge: CBDCs are run by central banks, while cryptocurrencies are usually decentralised.

Value: CBDCs are tied to the national currency, while crypto prices can swing wildly.

Purpose: Crypto often acts more like an investment. CBDCs are designed to be used like everyday money.

CBDC offers potential benefits for everyone:

For people: They can send and receive money instantly without bank delays, even outside of banking hours.

For businesses: Lower fees and smoother international transactions. Makes cross-border payments (sending money between countries) quicker and cheaper.

For governments: Better visibility into financial flows and stronger tools to manage the economy.

It’s not all positive. There are concerns too:

CBDCs are more than just theory. Many countries are experimenting with or already using CBDCs:

The digital yuan (e-CNY) is in large-scale pilot testing. During the 2022 Winter Olympics in Beijing, it was one of three forms of payment accepted. Additionally, the PBOC has partnered with tech giants like Tencent and Alibaba to facilitate digital yuan transactions through platforms such as WeChat and Alipay, ensuring broad accessibility.

By 2024, China’s digital yuan had grown significantly, with around 180 million personal wallets in use, which equals roughly one in eight citizens, and cumulative transactions amounting to several trillion RMB.

The “Sand Dollar” is one of the world’s first fully launched CBDCs. Currently, $1.4 million of the currency is in circulation, up 30% from 2022, but still representing under 1% of currency in circulation. There are over 100,000 registered wallets, equivalent to about 25% of the population. There are 1,800 registered merchants, and 9 SandDollar authorized financial institutions – — all figures referring to usage within the Bahamas.

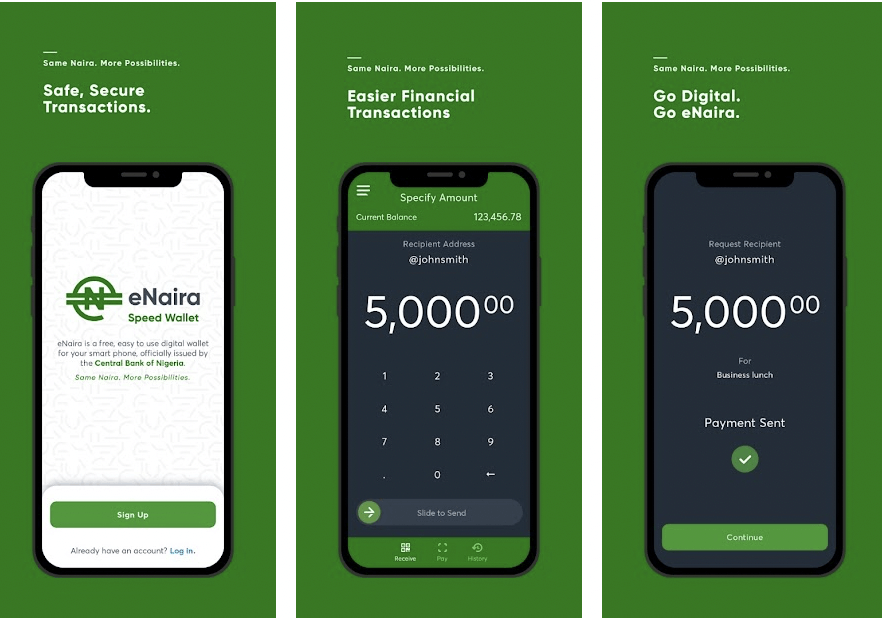

By early 2025, Nigeria’s eNaira had about NGN 18.31 billion in circulation (roughly USD 11.4 million), which made up only 0.37% of all cash in the country. Adoption has been growing, with around 12% of the population opening eNaira wallets by mid-2024 and millions of transactions completed. Still, the early phase showed challenges: by mid-2023, around 13 million wallets had been created, but many of them remained inactive, pointing to significant room for further growth.

By mid-2024, Jamaica’s JAM-DEX had been officially recognised as legal tender, making it the first CBDC in the region with the same status as cash. The currency was distributed through commercial banks and authorised payment service providers, giving citizens access via digital wallets. Early adoption was encouraged with government incentives, and several merchants began accepting it for everyday transactions. Still, overall uptake has been modest, reflecting the challenges of building trust and awareness, but it shows clear potential for advancing financial inclusion in a country where many people remain outside the traditional banking system

By early 2025, the digital euro remained in its preparation phase, which began in November 2023. This stage focuses on finalising the rulebook and infrastructure while also piloting the technical components needed for a potential launch. Around 70 fintech companies, banks, merchants, and start-ups have been involved in testing design choices and user needs through innovation platforms.

These conversations are also taking place at international gatherings. At the Global Digital Monetary Institute Symposium, fintech leaders, policymakers, and experts debated how CBDCs could reshape money. SDK.finance’s CTO joined the discussion, sharing hands-on insights about making central bank digital money secure and practical in the real world read more here.

The European Central Bank expects to conclude this phase in late 2025, after which a final decision on issuing a digital euro will be made.

Several countries outside the traditional financial centres are also making steady progress with CBDCs, each focusing on different priorities. In Kazakhstan, the central bank launched the digital tenge pilot in 2023, testing its use in retail payments, government services, and cross-border transactions, with a nationwide rollout planned by 2025.

The United Arab Emirates has taken a leading role in international CBDC cooperation through Project mBridge, working with China, Hong Kong, and Thailand under the Bank for International Settlements to explore faster and cheaper cross-border transfers.

Meanwhile, Saudi Arabia partnered with the UAE on Project Aber, one of the earliest regional pilots, which successfully trialled a shared digital currency for interbank payments. Together, these initiatives show how CBDCs are being shaped not only for domestic use but also for regional and global payments, highlighting their potential to reduce costs, improve efficiency, and strengthen financial sovereignty

Globally, over 130 countries are investigating CBDCs in some form.

Like many big ideas, the answer is: it depends. CBDCs could make money more inclusive and payments more efficient, but they could also bring risks around privacy and the role of traditional banks. Much will come down to how each country designs its version.

CBDCs are still in their early stages, but their potential is huge. Imagine paying for your coffee, receiving your salary, or sending money overseas instantly, all with digital cash guaranteed by your central bank.

Whether CBDCs become a regular part of our daily lives depends on how they’re rolled out. But one thing is clear: they’re set to be a big chapter in the ongoing story of how money evolves.

Proud to announce that SDK.finance is the best FinTech startup 2015! Central European Startups Awards has… Read More

On November 10, SDK.finance was presenting demo at Bank Innovation Israel 2015 DEMOvation challenge. Bank Innovation… Read More

Great news! SDK.finance is selected for the €20.000 cash prize pitch competition at Execfintech! After… Read More

On March 8, CTO SDK.finance Pavlo Sidelov and CEO Alex Malyshev were attending one of the… Read More

On March 30, SDK.finance has been selected as a finalist for Red Herring's Top 100 Europe award,… Read More

Money 20/20, the cutting-edge FinTech conference, was held April 4 – 8 in beautiful Copenhagen… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}