Digital Banking Software for Banks, EMIs and FinTech Companies

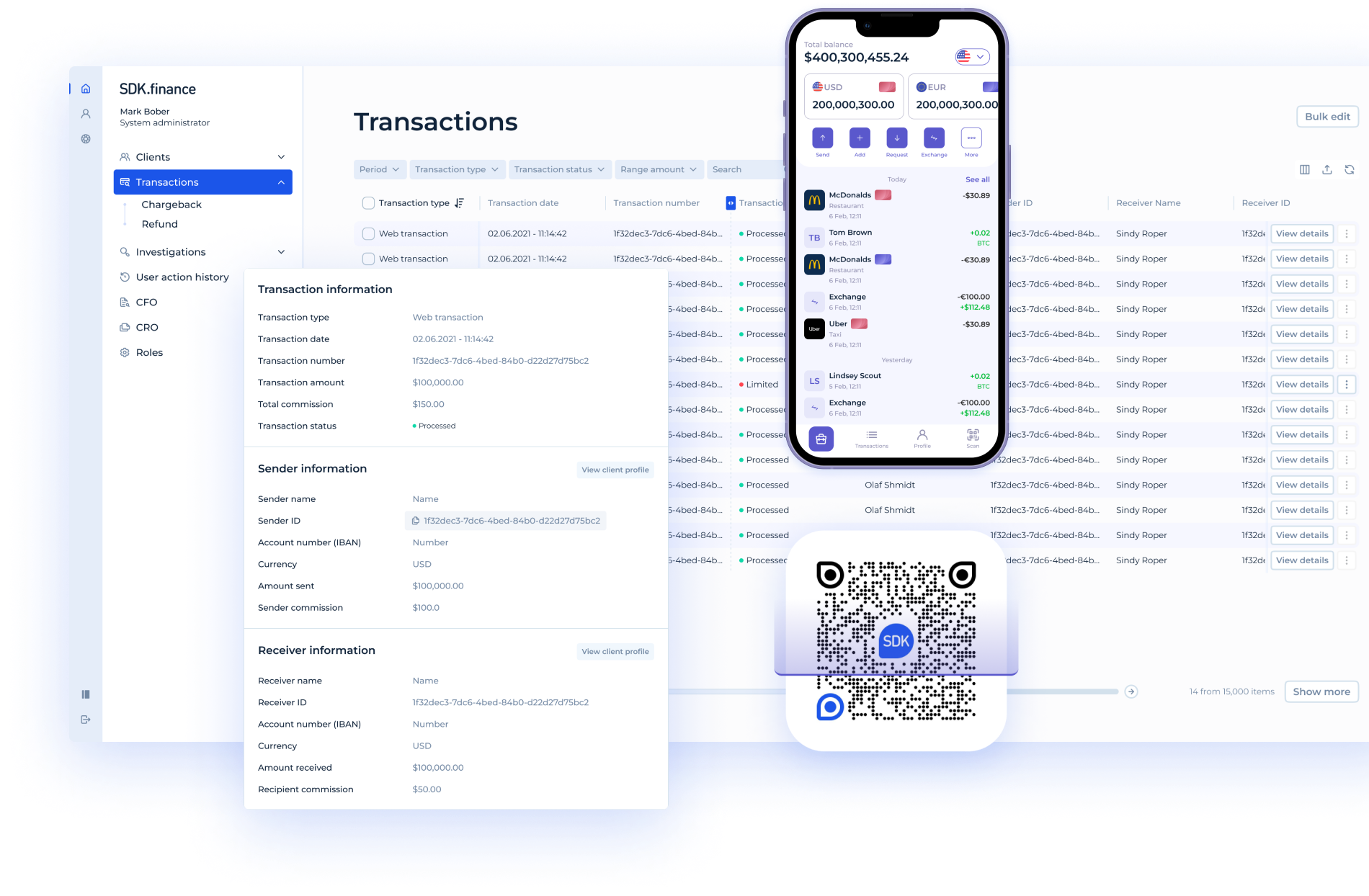

SDK.finance delivers banking software infrastructure designed to power regulated financial institutions and licensed payment providers. The Platform combines a modular banking backend with 570+ APIs to support account management, payment processing, card operations, and compliance workflows within a single banking environment.

Built for banks, Electronic Money Institutions (EMIs), and FinTech companies, SDK.finance supports card issuing integrations, payment gateway connectivity, IBAN infrastructure, AML monitoring, and reporting tools, forming a structured and auditable banking system rather than a standalone application layer.

What Is Digital Banking Software?

Digital banking software is the backend infrastructure that enables financial institutions to deliver banking services through digital channels. It manages core transaction processing, account logic, payment execution, card operations, and compliance workflows within a structured and auditable system.

Unlike an online banking interface, which focuses on the customer-facing layer, digital banking software operates at the operational and accounting level. It ensures that every deposit, transfer, fee, card transaction, and settlement event is recorded, reconciled, and processed in real time.

Digital banking software differs from traditional core banking software in scope and flexibility. Core banking systems were historically designed for branch-based banking models. Modern digital banking platforms are built around API-first architecture, modular services, and real-time processing to support mobile banking, embedded finance, and multi-channel financial products.

An API-driven approach allows institutions to integrate with KYC providers, card issuers, payment gateways, Open Banking services, and external financial systems without restructuring the core. Real-time processing ensures accurate balance updates, immediate transaction posting, and consistent double-entry accounting across all channels.

Why Digital Banking Infrastructure Matters in 2026

Digital banking has become the primary operating model for many banks, EMIs, and payment providers. According to Statista, global digital banking platform revenues are projected to exceed USD 40 billion in the coming years, reflecting sustained demand for mobile-first and API-driven financial services.

Research from McKinsey & Company shows that a majority of banking customers in developed markets rely on digital channels as their main point of interaction. This shift requires institutions to modernise backend infrastructure, not only customer-facing applications.

At the same time, Gartner reports that legacy core systems remain a significant constraint for digital transformation. Layered architectures, where new interfaces depend on outdated processing engines, often create integration bottlenecks and operational complexity.

As financial services expand into embedded finance, Open Banking, and cross-border payments, institutions need modular, API-first infrastructure capable of real-time processing, multi-currency support, and regulatory reporting. In 2026, competitive advantage depends on the stability and scalability of the transaction backbone behind digital products.

Looking for a scalable digital banking software?

Speak with our team to explore how SDK.finance can serve as the backend infrastructure for your banking or payment product.

Get in touchCore Components of Digital Banking Software

Digital banking software is built around several interconnected layers that ensure consistent transaction processing, regulatory compliance, and operational control. These components form the backbone of a modern digital banking infrastructure.

Ledger and Transaction Engine

A real-time transactional ledger forms the foundation of digital banking infrastructure. Its key capabilities include:

-

double-entry accounting for every financial event

-

atomic transaction posting to maintain balance consistency

-

real-time balance updates across accounts

-

high-throughput processing measured in thousands of transactions per second

-

multi-asset support, including fiat currencies, digital assets, and custom internal units

-

full audit trails for reconciliation and regulatory review

This engine ensures accounting integrity across all product layers.

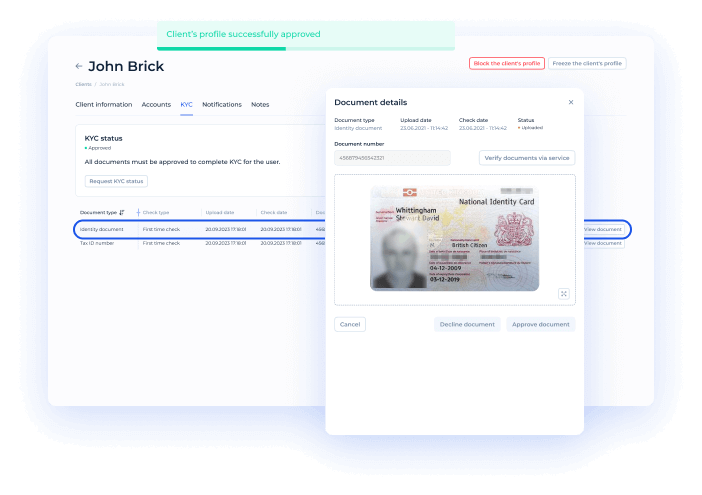

Customer onboarding and KYC/KYB

Structured onboarding workflows are essential for regulated institutions. Digital banking software typically provides:

-

configurable onboarding flows for individuals and businesses

-

integration with external KYC and KYB providers

-

document verification and screening processes

-

risk scoring and compliance status tracking

-

ongoing monitoring integrated into account lifecycle management

Compliance logic is embedded directly into backend operations rather than handled as a separate layer.

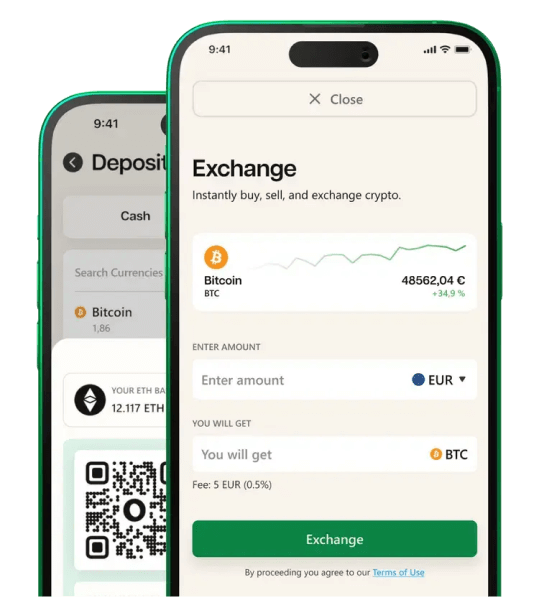

Multi-currency accounts and digital assets

Modern banking platforms operate in multi-currency environments by default. Core capabilities include:

-

management of multiple fiat currencies within a single customer profile

-

automated FX rate handling and currency conversion logic

-

configurable fee and commission structures

-

support for digital assets and tokenised balances

-

unified ledger reflection across all asset types

All balances remain accounted for within a single accounting framework.

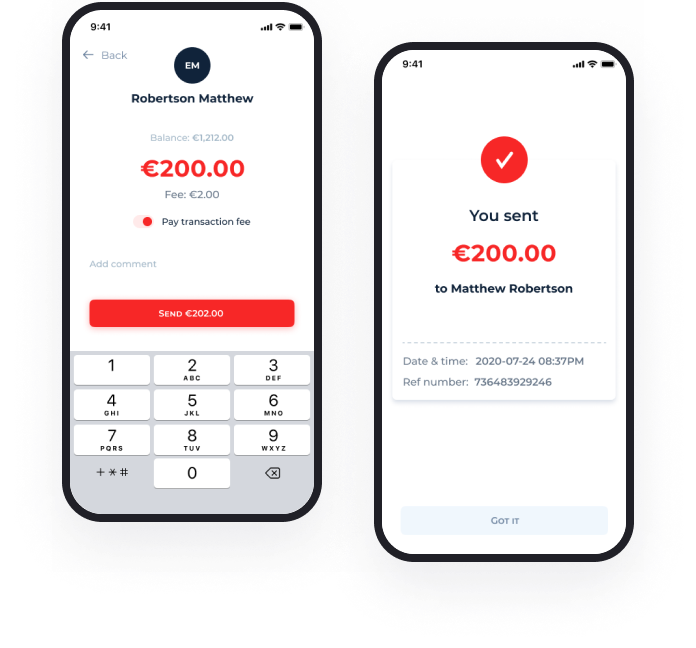

Payments and card issuing

Digital banking software must support complete payment and card workflows, including:

-

inbound and outbound transfers

-

domestic and cross-border payments

-

integration with payment gateways and clearing systems

-

BIN sponsor and card processor connectivity

-

transaction routing and authorisation handling

-

IBAN allocation and account linking

-

settlement and reconciliation management

These functions operate within the same backend infrastructure to ensure operational reliability.

Back office and operational control

A structured backoffice environment supports operational governance and auditability. Core features include:

-

role-based access control for operational teams

-

transaction monitoring and review tools

-

AML and fraud management workspaces

-

configurable fees, limits, and product parameters

-

reconciliation modules and reporting tools

-

detailed user activity logs and audit trails

This layer ensures transparency and regulatory readiness at scale.

Architecture of Modern Digital Banking Platforms

Modern digital banking platforms are built as layered, modular infrastructures rather than monolithic banking systems. Architecture determines how efficiently an institution can scale, integrate with partners, and introduce new financial products without rewriting core logic.

A robust digital banking architecture typically includes the following structural elements.

Real-time ledger foundation

SDK.finance is built around a real-time double-entry ledger that records every transaction consistently across accounts. This ensures balance integrity, accurate reconciliation, and full audit visibility for regulated financial operations.

Multi-asset and multi-currency support

The system supports multiple fiat currencies, digital assets, and custom balance types within a unified accounting framework. FX logic, fee application, and settlement flows operate within the same ledger structure.

API-driven integration layer

With 570+ APIs, SDK.finance enables structured integration with KYC providers, payment gateways, card processors, Open Banking services, and external financial systems without altering core accounting logic.

Modular banking backend

The Platform provides a modular backend covering accounts, payments, cards, limits, fees, and compliance workflows. Each functional domain can be configured independently without restructuring the core transaction engine.

Card and payment infrastructure

The Platform supports inbound and outbound payments, IBAN allocation, BIN sponsor integrations, transaction routing, authorisation handling, and settlement processing within a single backend environment.

Operational and compliance control

A structured backoffice provides role-based access, transaction monitoring, reconciliation tools, AML workflows, and reporting capabilities to ensure transparency and regulatory readiness.

Deployment Models for Digital Banking Software

Digital banking infrastructure must align with regulatory requirements, internal IT policies, and long-term scalability plans. Modern platforms typically support multiple deployment approaches.

Source Code License

AvailableA one-time purchase that provides full ownership of the platform’s codebase. This option is ideal for enterprises and financial institutions that require maximum control, unlimited customisation, and independence from the vendor. With the source code license, you can host the solution on-premise or in your preferred cloud infrastructure.

View detailsSaaS

AvailableA subscription-based model designed for startups and growing fintechs that need a quick launch with minimal upfront costs. The SaaS option gives you access to the full white-label banking software environment, pre-built mobile and web apps, and ongoing updates managed by SDK.finance.

View detailsWho Uses Digital Banking Software?

Digital banking software is used by regulated financial institutions and technology-driven organisations that require structured transaction processing and accounting infrastructure. Typical user segments include:

providers

SDK.finance Digital Banking Software

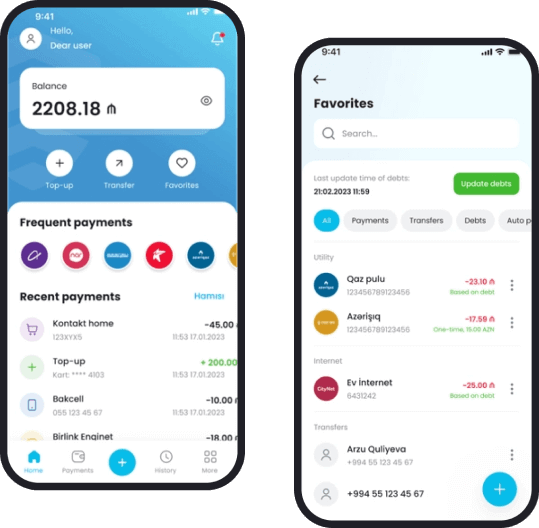

Real-time transactional ledger

At the core of the Platform is a real-time double-entry transactional ledger that records every financial event consistently across accounts. All deposits, transfers, fees, settlements, and card transactions are posted atomically to maintain balance integrity and audit accuracy.

60+ functional modules

The Platform includes more than 60 configurable modules covering accounts, wallets, payments, cards, limits, compliance workflows, treasury logic, and reporting. Each module operates within the same ledger-based framework.

570+ APIs

SDK.finance provides 570+ REST APIs for structured integration with KYC providers, payment gateways, card processors, Open Banking services, and internal systems. All integrations connect directly to the core transaction engine.

PCI DSS Level 1 certified backend

The Platform backend is PCI DSS Level 1 certified, supporting secure processing of card-related data and compliance with international payment security standards.

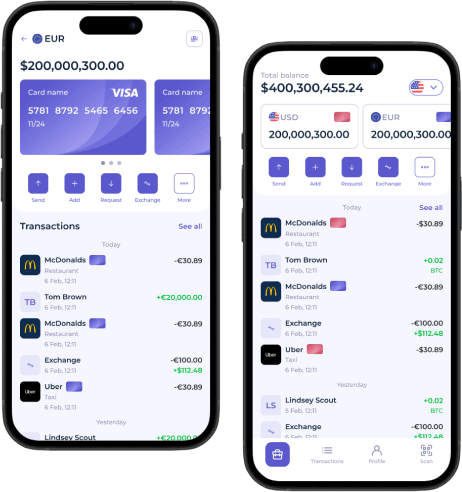

Multilingual web and mobile frontend

SDK.finance provides a ready-to-deploy multilingual web and mobile frontend that connects to the same backend infrastructure and APIs. The interface supports localisation, configurable branding, and role-based user access while maintaining consistent transaction logic at the core.

Crypto and digital asset support

The Platform supports accounting and operational logic for digital assets alongside fiat currencies within the same ledger structure. It enables internal balance management, crypto-to-fiat flows, and integration with custody and on/off-ramp providers without separating accounting models across systems.

Continuous updates

Maintain the ability to customize and scale your solution while benefiting from our regular updates, patches and enhancements.

Solutions Powered by Digital Banking Software

White-label banking solution

AvailableWhite-label banking solutions are built on digital banking infrastructure to enable branded financial services without developing core transaction logic from scratch. The backend manages accounts, payments, cards, compliance workflows, and reporting while the frontend layer is customised to match the institution’s brand and market positioning.

View product pageCore banking

AvailableDigital banking software can operate as a modern core banking layer for institutions seeking to replace or extend legacy systems. The platform manages customer accounts, transaction posting, balance logic, settlement processes, and regulatory reporting within a structured ledger environment.

View product page

Digital wallet platforms

AvailableDigital wallet solutions rely on digital banking infrastructure to manage stored value accounts, peer-to-peer transfers, merchant payments, and internal settlement flows. All wallet balances are reflected within the same accounting framework as traditional banking accounts.

View product page

Payment processing

AvailablePayment processing solutions use digital banking software to manage merchant balances, settlement logic, payout automation, commission structures, and transaction monitoring. The backend centralises accounting across acquiring flows, merchant payouts, and internal balance movements.

View product page

Embedded finance solutions

AvailableEmbedded finance models integrate digital banking infrastructure into non-financial platforms such as marketplaces, telecom operators, and service ecosystems. The backend enables wallet management, internal ledger logic, and regulated payment processing within third-party digital environments.

View product page

Crypto banking

Coming soonCrypto banking solutions combine digital asset operations with fiat infrastructure under a unified ledger structure. The platform supports internal balance accounting, crypto-to-fiat settlement flows, and integration with custody and on/off-ramp providers while maintaining consistent double-entry records.

View product page

Ready to get started?

Latest insights from the SDK.finance blog

Frequently Asked Questions

Digital banking software is backend infrastructure that enables financial institutions to operate accounts, process transactions, manage payments, issue cards, and maintain regulatory compliance through digital channels. It combines a real-time ledger, transaction engine, and API integration layer within a structured and auditable system.

Core banking software traditionally focuses on managing customer accounts and transaction processing within branch-based banking models. Digital banking software extends this foundation with API-first architecture, real-time integrations, multi-channel support, and modular services designed for mobile, embedded finance, and online-first operations.

Yes. Modern digital banking platforms can support digital assets alongside fiat currencies within the same ledger structure. This includes internal balance accounting, crypto-to-fiat settlement flows, and integration with custody and on/off-ramp providers while maintaining consistent double-entry records.

Yes. When designed with structured audit trails, role-based access control, AML integrations, and security certifications such as PCI DSS and ISO 27001 alignment, digital banking software can operate within regulated banking and EMI environments.