How much does it cost to start or build a bank in 2026? The answer depends on the type of banking business you want to launch, the licensing model, regulatory capital requirements, core banking software, infrastructure, integrations, and the size of your development team.

For a fully licensed bank, startup costs can reach several million dollars once regulatory capital, legal advisory, compliance, technology infrastructure, and operational setup are included. A digital bank or neobank can be launched with a lower initial budget, especially if you use a ready-made core banking platform, licensed partners, or a white-label banking software solution instead of building every component from scratch.

In this guide, we break down the main cost categories behind starting a bank, from licensing and compliance to UI/UX design, banking software development, infrastructure, product launch, and ongoing maintenance.

How much does it cost to start a bank?

The cost of starting a bank can range from tens of thousands of dollars for early legal setup or a partner-based digital banking product to several million dollars for a fully licensed institution. The final budget depends on your jurisdiction, license type, regulatory capital requirements, technology stack, product scope, and operating model. Below is a high-level breakdown of the main cost categories involved in building a bank.

Bank startup cost breakdown

| Cost category | Estimated cost |

|---|---|

| Licensing and legal setup | From $25,000 to several million |

| Regulatory capital | Depends on jurisdiction and bank type |

| Core banking software | $100,000-$500,000+ for custom development; lower with a ready-made platform |

| UI/UX and prototyping | $10,000-$40,000 |

| Infrastructure | $300-$600/month for cloud; $50,000-$200,000+ for on-premise infrastructure |

| Development team | Varies by region and team size |

| Launch and marketing | From $5,000+ |

| Maintenance and support | From $8,000/month |

The cost of starting a bank depends heavily on the type of banking business you want to launch. A traditional bank, digital bank, neobank, or banking product built with licensed partners will require different levels of regulatory capital, licensing, infrastructure, compliance, and software development.

- Traditional banks, often referred to as brick-and-mortar banks, usually have the highest startup costs. They need physical branches, larger operational teams, extensive regulatory approval, security infrastructure, and significant capital reserves. For entrepreneurs asking how much money is needed to start a bank, a fully licensed traditional bank is usually the most expensive path.

- Digital banks and neobanks operate with a different cost structure. Instead of building and maintaining a branch network, they rely on digital channels, mobile banking apps, core banking software, payment integrations, KYC/AML tools, and cloud or on-premise infrastructure. This can reduce some operational costs, but technology, compliance, licensing, cybersecurity, and ongoing maintenance still require serious investment.

For many FinTech companies, the most cost-efficient route is not to build every banking component from scratch. A digital banking product can be launched faster by using a ready-made core banking platform, white-label banking software, Banking-as-a-Service providers, or licensed partners. This approach can reduce development time, lower technical risk, and help control the initial cost of building a digital bank.

Digital banking market context

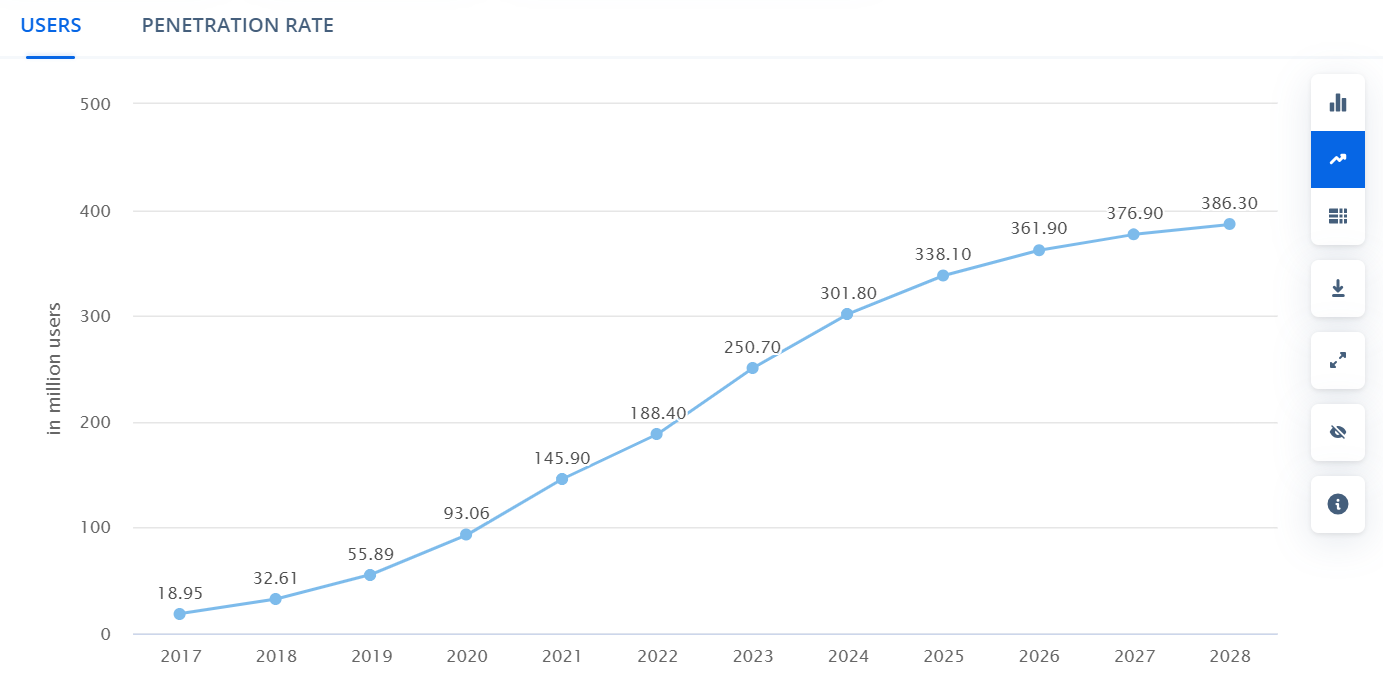

Digital banking continues to grow as customers shift toward mobile-first financial services, instant payments, lower fees, and 24/7 account access. According to Statista, the number of digital banking users worldwide is projected to reach 386 million by 2028, while digital banks’ net interest income is expected to continue growing as adoption increases.

This market growth makes digital banking attractive for startups, FinTech companies, and established financial institutions. However, it does not remove the cost and complexity of launching a bank. Even digital-first banking businesses must budget for licensing, regulatory compliance, banking software, payment integrations, fraud prevention, customer support, infrastructure, and ongoing maintenance.

The number of digital banking users 2017-2028

Source: Statista

Key functionality that affects digital bank development cost

The functionality you include in your banking product has a direct impact on development cost, implementation time, infrastructure requirements, and ongoing maintenance. A simple digital banking MVP with account management and basic payments will cost less than a full-scale neobank with card issuing, business banking, lending, analytics, and multiple third-party integrations.

Below are the main feature groups that usually shape the cost of building a digital bank.

| Feature group | What affects the cost |

|---|---|

| Customer onboarding and account management | Digital registration, customer profiles, account opening, document collection, and user verification flows. Cost impact: High, because onboarding must be secure, compliant, and easy to use. |

| KYC, AML, and compliance tools | Identity verification, sanctions screening, transaction monitoring, audit logs, and reporting workflows. Cost impact: High, especially in regulated markets. |

| Core banking functionality | Accounts, balances, ledger logic, transaction history, fees, limits, statements, and account rules. Cost impact: Very high, as this is the foundation of the banking system. |

| Payments and money transfers | P2P transfers, bank transfers, bill payments, recurring payments, and payment gateway integrations. Cost impact: High, depending on payment methods, countries, and providers. |

| Card issuing and card management | Virtual cards, physical cards, card limits, card controls, and Visa/Mastercard integrations. Cost impact: Medium to high, depending on issuing partners and integration complexity. |

| Mobile and web banking apps | iOS, Android, and web interfaces for customers and administrators. Cost impact: High, especially if both customer-facing and back-office interfaces are needed. |

| Business banking features | Corporate accounts, role-based access, approvals, payroll, invoicing, and merchant services. Cost impact: Medium to high, depending on workflow complexity. |

Additional cost drivers may include analytics and reporting, fraud prevention, third-party integrations, back-office functionality, and customer support tools.

How much does it cost to build a bank? Full cost breakdown of building a bank

After defining the type of bank and the core functionality, the next step is to break down the main expenses involved in launching and operating the product. The largest cost categories usually include licensing and regulatory compliance, product design, technology infrastructure, software development, integrations, launch, and ongoing maintenance.

The final budget will vary depending on jurisdiction, license type, product complexity, development approach, and whether you build the banking system from scratch or use a ready-made platform.

Regulatory compliance

Banking license and regulatory compliance costs are among the largest expenses when starting a bank. The exact amount depends on the jurisdiction, license type, business model, regulatory capital requirements, and the services your institution plans to offer. A fully licensed bank usually requires significant capital reserves, legal support, regulatory reporting, insurance, AML/KYC processes, data protection controls, and ongoing compliance operations. A digital bank, EMI, MSB, or neobank working with licensed partners may have a different cost structure, but compliance still remains a major part of the overall budget.

| Cost factor | Europe | USA |

|---|---|---|

| Capital requirement | From €350,000 to €5,000,000, depending on license type and jurisdiction | For MSBs, capital requirements may start from $0; for smaller regulated companies, from $25,000 |

| EMI or payment institution license | From €1,000-€5,000 in application-related fees, depending on jurisdiction | Money transmitter or MSB licensing can vary by state |

| Legal and advisory fees | From €50,000; specialized bank setup may require significantly higher advisory costs | MSL-related costs may range from $500 to $2,000 per state, with legal fees varying by state |

| AML, KYC, and data protection compliance | Depends on business scope, customer risk profile, and required compliance tooling | Depends on federal and state-level requirements, transaction volume, and compliance setup |

These figures are indicative and can vary significantly depending on the regulator, country, license type, and business model. In addition to licensing and legal setup, banks must also budget for AML procedures, KYC verification, data protection, audit trails, transaction monitoring, reporting, and ongoing compliance staff or external advisors.

Prototyping and UI/UX design

Prototyping and UI/UX design are important cost factors when building a digital bank, because they define how customers will open accounts, pass verification, manage balances, make payments, and interact with financial services.

Before development begins, prototypes help stakeholders test the product flow, validate user journeys, and identify usability issues early. This is especially important for banking products, where onboarding, KYC, account management, payment flows, and security steps must be both intuitive and compliant.

Basic clickable prototypes can start from around $10,000, while more advanced interactive prototypes and full UI/UX design work may start from $15,000-$40,000, depending on the number of screens, platforms, user roles, and customization level.

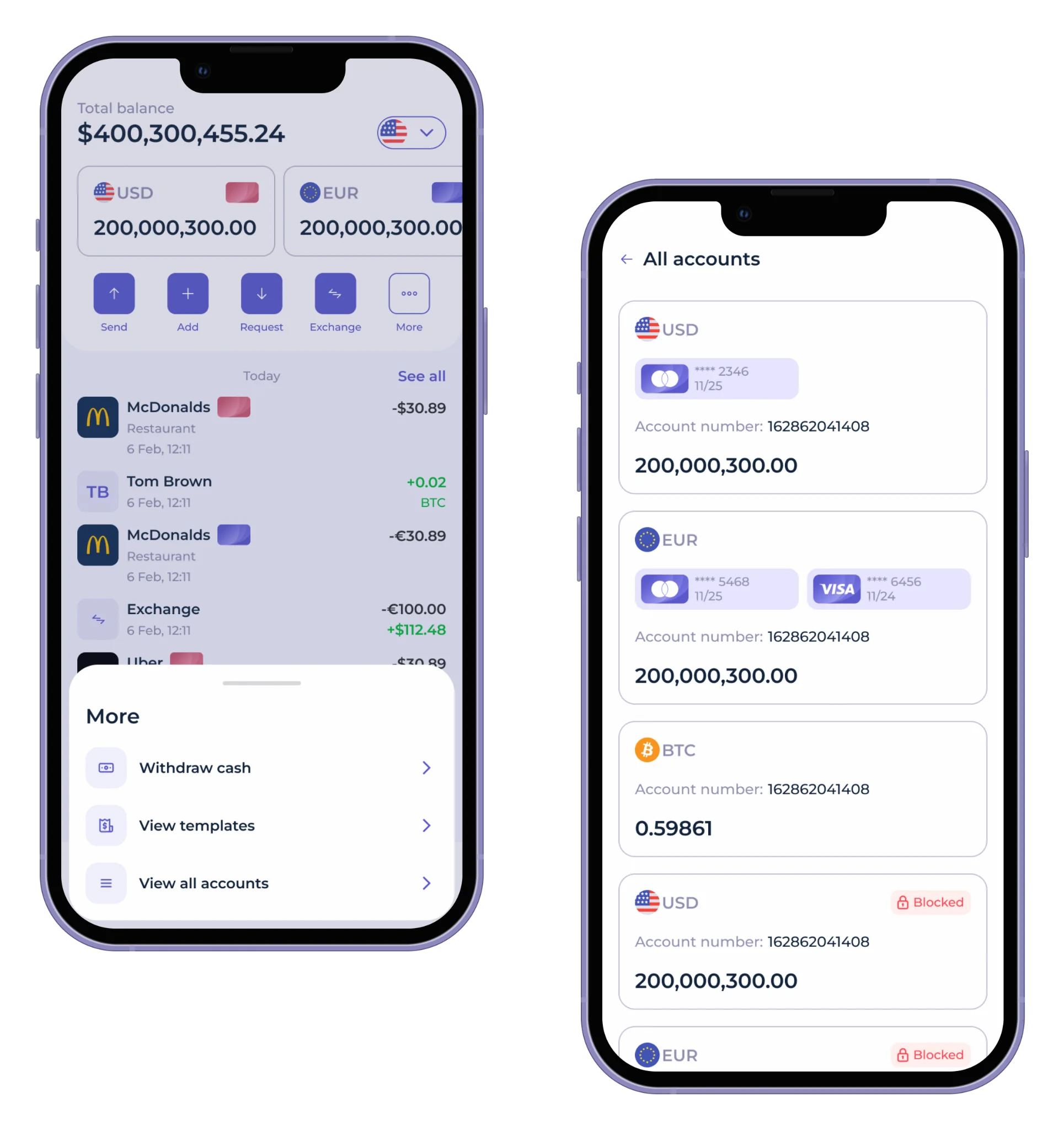

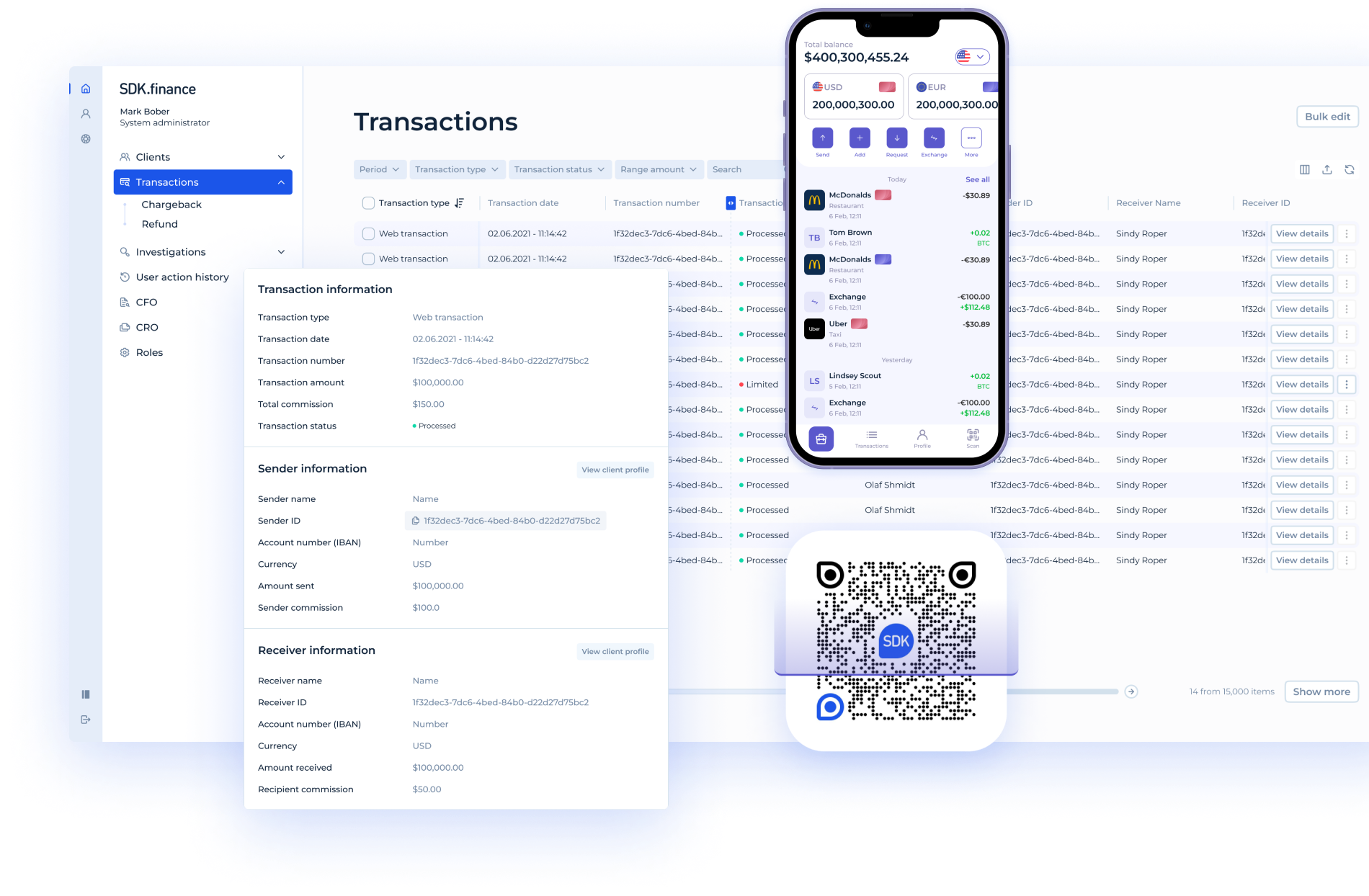

SDK.finance provides a mobile banking app UI/UX design kit to accelerate digital bank launch. It includes ready-made design components for digital banking, ewallet, and payment apps, compatible with iOS and Android.

Watch our video showcases the user-friendly mobile mobile banking app UI of SDK.finance Platform, designed to empower you to create secure and feature-rich bank in record time:

The cost of UI/UX design for a banking app depends on the number of screens, supported platforms, product complexity, and the level of customization.

A simple digital banking MVP with basic onboarding, account overview, and payments will require fewer design hours than a full-scale neobank with personal finance tools, card management, business banking, lending, and back-office workflows. The design budget is also affected by how many user roles and journeys need to be covered.

For example, a customer-facing mobile app may include onboarding, KYC, account management, money transfers, card controls, notifications, and support flows. A more advanced banking product may also require web banking, admin panels, compliance dashboards, transaction review screens, and business account workflows.

Typical UI/UX design costs for a banking app may include:

| Design stage | Estimated cost |

|---|---|

| Product discovery and user flow mapping | From $5,000-$10,000 |

| Basic clickable prototype | From $10,000 |

| UX/UI design and interactive prototyping | From $15,000-$40,000 |

| User testing and design iteration | From $5,000-$10,000 |

| Full design system for mobile and web apps | From $20,000-$50,000+ |

Using ready-made mobile and web interfaces can reduce these costs. SDK.finance provides customizable interfaces for digital banking, ewallet, and payment products, helping businesses save time on UI/UX design and focus resources on branding, compliance, integrations, and launch-specific customization.

Technology infrastructure

Technology infrastructure is one of the key cost drivers when building a digital bank. It affects not only the initial setup budget, but also ongoing operational expenses, scalability, security, compliance, and system reliability.

A banking product needs infrastructure that can support account operations, transaction processing, API integrations, data storage, monitoring, backups, access controls, and security requirements. The final cost depends on the hosting model, transaction volume, compliance requirements, data residency rules, and whether the system is built from scratch or deployed on top of an existing banking platform.

Cloud vs. on-premises hosting

- Cloud hosting is usually the more flexible option for digital banks and neobanks. Cloud providers such as AWS, Microsoft Azure, or Google Cloud make it easier to scale resources as the product grows. For an early-stage banking product, basic cloud infrastructure may start from around $300-$600 per month, but costs can increase as traffic, storage, monitoring, security, and compliance requirements grow.

- On-premises hosting requires a larger upfront investment in servers, networking equipment, security infrastructure, maintenance, and technical staff. Initial setup costs can range from $50,000 to $200,000 or more, depending on the scale and security requirements. This model may be relevant for institutions with strict internal policies, data residency requirements, or legacy infrastructure constraints.

Backend infrastructure

Backend infrastructure includes the systems that process transactions, manage customer accounts, store financial data, connect APIs, and keep the banking product available and secure. These costs depend on the architecture, database setup, hosting model, traffic load, security requirements, and the number of integrations.

Database management systems can also influence the budget. Commercial database licenses may cost $7,000-$15,000 per year, while open-source options such as PostgreSQL can reduce licensing costs but may require more engineering and maintenance effort.

Load balancing, monitoring, logging, backups, and disaster recovery should also be included in the infrastructure budget. Managed load balancer services can cost around $1,000-$3,000 per month, depending on provider, traffic volume, and configuration.

Integration with financial systems

- Integrations with financial systems are another major infrastructure-related cost. A digital bank may need to connect with payment processors, card issuers, KYC providers, AML tools, accounting systems, notification services, and other third-party platforms.

- Payment gateway integrations often include transaction-based fees. Depending on the provider, costs may range from $0.30-$0.50 per transaction, plus a percentage fee of around 1.5%-2.9% of the transaction amount.

- Core banking integrations can be more expensive, especially when custom development is required. Connecting to or building around a core banking system may cost $100,000-$500,000, depending on the complexity, number of APIs, compliance requirements, and level of customization.

Using a ready-made banking platform with pre-built APIs and integration capabilities can reduce infrastructure complexity and lower development costs compared with building every backend component and integration from scratch.

Development team

The development team has a major impact on the overall cost of building a banking app or digital bank. Team size, seniority, location, technical stack, and delivery model all influence the final budget. However, for banking and FinTech projects, general software development experience is not enough.

The team should have proven expertise in banking, payments, compliance, security, integrations, and financial product architecture. Banking software involves sensitive customer data, transaction logic, regulatory requirements, audit trails, KYC/AML workflows, and integrations with payment providers, card issuers, and core banking systems. A team without relevant banking or FinTech experience may underestimate complexity, increase delivery risk, and create expensive rework later.

Custom software development rates by role and country per hour

Hourly rates vary depending on the specialist’s seniority, location, FinTech experience, and engagement model. Banking and payment software usually requires more experienced engineers, solution architects, QA, DevOps, and compliance-aware specialists, so the lowest market rates are not always the safest option.

| Region | Business & design roles | Development & QA roles | Architecture, DevOps & compliance |

|---|---|---|---|

| North America | $70-$150/hour | $60-$170/hour | $100-$220/hour |

| Western Europe | $60-$130/hour | $50-$150/hour | $80-$180/hour |

| Central & Eastern Europe | $35-$80/hour | $30-$90/hour | $50-$120/hour |

| Latin America | $35-$80/hour | $30-$90/hour | $50-$120/hour |

| South Asia | $20-$60/hour | $20-$70/hour | $35-$90/hour |

These rates are indicative and can vary depending on project complexity, vendor reputation, and the level of banking or FinTech expertise required. For a digital bank, domain experience is critical: choosing a cheaper team without payment, compliance, security, or core banking knowledge can increase the risk of delays, rework, and regulatory issues.

Create your digital banking solution in weeks

Talk to Our TeamProduct launch and maintenance

Following a successful bank development, there are ongoing costs associated with product launch and maintenance. Below are approximate costs for these activities, based on market prices.

Product launch costs

To create awareness and drive user adoption, invest in marketing strategies such as digital advertising, public relations, and promotions. This can range from $5,000 and more, depending on the scale and channels used.

Ongoing maintenance costs

Regular updates, bug fixes, and feature enhancements can add $5,000 per month, depending on the frequency and complexity of updates.

Maintaining a support team to handle user inquiries, issues, and feedback. This could cost from $3,000 per month, depending on the size of the support team and the volume of requests.

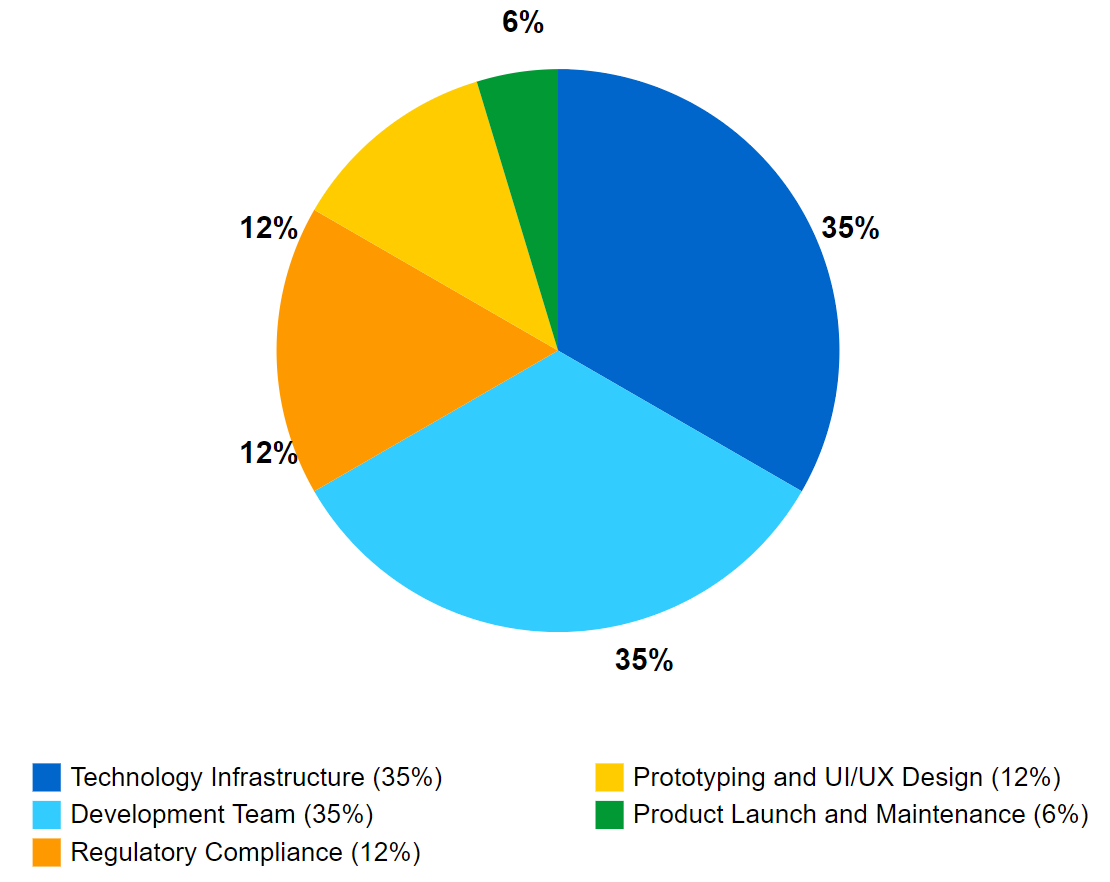

Percentage breakdown of costs for bank development

The cost of starting a bank is substantial and can vary widely depending on numerous factors. It’s essential to conduct thorough research, consult with experts, and develop a detailed business plan to accurately estimate the costs involved and make informed decisions.

How SDK.finance helps reduce the cost and time of building a digital bank

Building a bank from scratch requires a large budget, an experienced FinTech development team, regulatory knowledge, core banking functionality, payment integrations, back-office tools, infrastructure, and ongoing maintenance. For many companies, the biggest cost driver is not only development itself, but the time spent designing, building, testing, integrating, and stabilizing all core components before launch.

SDK.finance helps reduce these costs with a ready-made banking Platform for building digital banks, neobanks, and payment products. Instead of developing every component from scratch, businesses can start with a pre-developed foundation and customize it for their business model, branding, compliance needs, and target market.

The Platform can accelerate up to 70% of the development process by providing ready-to-use functionality, APIs, back-office tools, and integration capabilities. This helps reduce engineering workload, shorten time-to-market, and lower the risks associated with building complex banking infrastructure from zero.

Key SDK.finance digital banking features

SDK.finance provides a flexible feature set for launching and scaling digital banking and payment products, including:

- Multi-currency accounts

- Payments and money transfers

- P2P transfers

- Currency exchange

- Card issuing integrations

- Customer management

- Transaction management

- Configurable fees and limits

- Back-office tools

- API-based integrations

- Mobile and web interfaces

By using SDK.finance, companies can avoid much of the cost and complexity of building a digital banking system from the ground up. The Platform gives you a ready-made technical foundation while still allowing customization for your business logic, customer experience, compliance requirements, and go-to-market strategy.

Launch your digital bank in weeks, not years

Talk to Our TeamWrapping up

The cost of starting or building a bank depends on licensing, regulatory capital, compliance, product scope, infrastructure, integrations, development team, and ongoing maintenance. A fully licensed bank may require several million dollars to launch, while a digital bank or neobank can reduce upfront costs by using licensed partners, ready-made banking software, and modular FinTech infrastructure. The most important step is to define the type of banking product you want to build, estimate the required functionality, and choose the right development approach.

Building everything from scratch gives full control, but it also increases cost, timeline, and technical risk. Ready-made platforms like SDK.finance help reduce development time, optimize engineering costs, and accelerate launch by providing core banking functionality, APIs, back-office tools, and customizable interfaces out of the box. This allows businesses to focus resources on market strategy, compliance, integrations, and customer acquisition instead of rebuilding the entire banking infrastructure from zero.

Ready to reduce the cost of building your digital bank? Use SDK.finance to reduce development time, lower engineering costs, and focus your resources on compliance, integrations, branding, and customer acquisition.

Contact us to discuss how SDK.finance can help you launch your digital bank faster and more cost-efficiently.