AI is showing up in nearly every banking and payments roadmap right now. And the opportunity is real: McKinsey estimates that generative AI and advanced analytics could add between $200 billion and $340 billion in annual value to the global banking sector – roughly 2.8 to 4.7 percent of industry revenues – mostly through productivity gains.

But most institutions are still stuck in pilot mode. A McKinsey and IACPM survey of banking executives found that only 12 percent of North American respondents had fully deployed any generative AI use case at all, even though more than half had named AI adoption a strategic priority. The gap between ambition and production is wide, and it is rarely about the model.

It is usually the infrastructure. If transaction data is scattered across systems, if the ledger is not real-time or auditable, if reconciliation still runs on spreadsheets, and if there is no clean way to log who approved what – AI has nothing solid to stand on. It can generate a summary or a suggestion, but it cannot be trusted with anything that touches money.

This is the real story behind AI in banking software: before you ask what AI can do, you need to ask whether your banking software or payment software can support it safely. That means clean APIs, a real-time ledger, governed data, and workflows where AI recommends and humans, or pre-approved rules, decide.

This article walks through what that looks like in practice – for banks, but just as much for PSPs, EMIs, wallets, and other FinTechs building on modern payment infrastructure.

What AI in banking software really means

AI in banking gets used as a catch-all, but the use cases underneath it vary enormously in risk and maturity. It helps to separate them into rough categories:

- Customer support and operations – chat assistants, internal knowledge search, and ticket triage built on top of documentation and product data.

- KYC/KYB document processing – extracting and pre-validating data from IDs, business registries, and compliance documents before a human reviewer signs off.

- Fraud and anomaly detection – pattern recognition across transactions to flag unusual behavior for review.

- Reconciliation and settlement support – spotting mismatches between internal records and external statements or provider reports.

- Transaction monitoring – surfacing patterns relevant to AML and compliance obligations.

- Payment routing recommendations – suggesting which provider, rail, or corridor is likely to be cheapest or most reliable for a given transaction.

- Merchant risk and account behavior analysis – scoring merchants or accounts based on transaction patterns over time.

- Financial insights and reporting – turning raw transaction data into digestible summaries for operators or business users.

Some of these – a support assistant answering questions from a knowledge base – carry low risk if it gives a wrong answer. Others – a model influencing which transactions get flagged for AML review – carry real regulatory and financial exposure if they are wrong, opaque, or unsupervised. Treating all AI in banking software use cases as equivalent is where a lot of strategy documents go wrong.

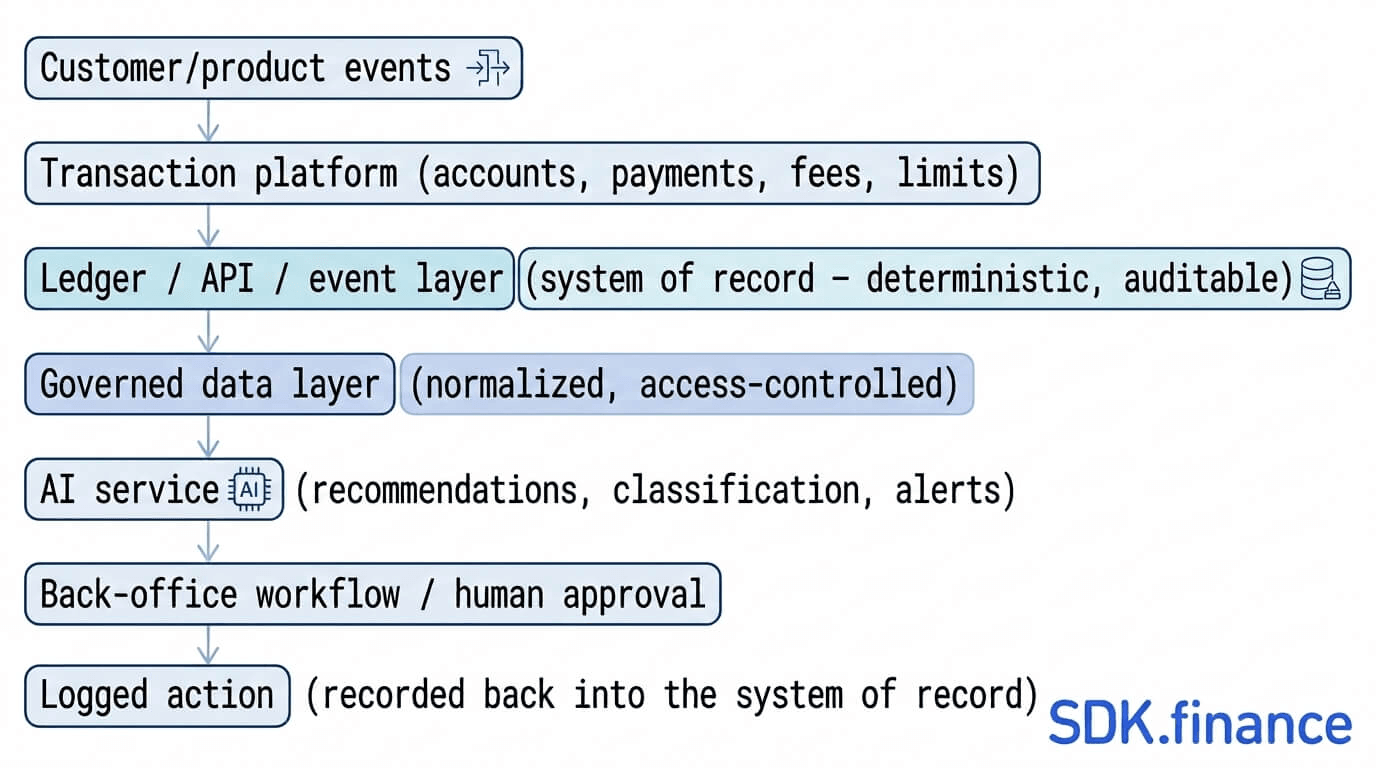

Why the ledger is the boundary AI should respect

Image source: SDK.finance General Ledger Solution interfaces

In any core banking software or payment processing system, the ledger is the system of record for money. Every debit and credit has to be deterministic, traceable, and reproducible – not just useful, but provably correct, because auditors, regulators, and reconciliation processes all depend on it.

This is the line that matters most in any AI-in-FinTech strategy: AI should not autonomously change balances, approve payouts, or move funds. Large language models and machine learning systems are probabilistic – the same input does not always guarantee the same output, and their reasoning is not fully auditable in the way a rule-based ledger posting is. That is fine for a support suggestion. It is not acceptable for a debit entry.

The productive framing is not whether AI should touch the ledger. It is how AI can support decisions around the ledger without being allowed to write to it directly. AI can flag a suspicious transaction, summarize a reconciliation exception, or recommend a payout hold. A human operator, or a pre-approved rules engine, still executes the action, and the ledger still records it the same deterministic way it always has.

Regulators are converging on the same principle

This is not just a risk-management preference – it lines up with where supervisors are heading. European banking supervisors have highlighted that institutions need clear accountability for AI-driven decisions, effective senior management oversight, and robust challenge mechanisms involving risk management, compliance, and internal audit. One recurring concern supervisors have raised is fragmented ownership of AI systems, with responsibility split across IT, data science, business lines, and control functions, without a clear accountability framework.

In practice, this means AI outputs need to be explainable enough for a human to review, challenge, and approve before they translate into a financial action. Keeping AI outside the ledger is not just good architecture – it is consistent with the direction of regulatory expectations around accountability, oversight, and auditability.

AI-ready banking infrastructure: what needs to exist first

Before AI creates real value in banking or payment software, certain infrastructure needs to already be in place:

- API-first architecture – so AI services can read data and trigger workflows without touching the core directly.

- Clean, structured transaction data – consistent fields, consistent statuses, no silent gaps.

- Real-time event streams or transaction updates – AI working on stale data produces stale recommendations.

- A double-entry ledger – the deterministic backbone that AI observes but does not override.

- Currency-specific balance management – critical for any product operating across corridors or asset types.

- Multi-entity account structure – support for individuals, businesses, and nested organizational relationships.

- Reconciliation-ready records – transactions traceable end-to-end against provider and bank statements.

- Role-based access controls – so AI-surfaced recommendations route to the right operator, not everyone.

- Audit logs – every recommendation, alert, and resulting action recorded.

- Configurable fees and limits – so AI-driven insights, like routing suggestions, can be acted on within existing commercial rules.

- A compliance and fraud operations workspace – where flagged items land for human review.

- A reporting layer – turning ledger and transaction data into something AI can summarize meaningfully.

Without this layer, AI pilots tend to produce demos that never make it to production – because there is no safe, governed place for the AI output to land.

Safe AI use cases for banking, PSPs, EMIs, and FinTechs

| Use case | What AI does | Risk | Infrastructure needed | Why it matters |

| Customer support knowledge assistant | Answers questions using product docs and account data | Low | API access to account/product data, governed knowledge base | Reduces support load without touching financial actions |

| KYC/KYB document pre-check | Extracts and validates document data before human review | Medium | Document ingestion pipeline, structured KYC data model | Speeds onboarding while keeping approval human-led |

| Transaction anomaly detection | Flags unusual transaction patterns | Medium | Real-time transaction feed, historical data | Surfaces risk earlier without blocking transactions automatically |

| AML/fraud alert prioritization | Ranks and clusters alerts for investigators | Medium-High | Transaction monitoring workspace, case management | Helps compliance teams focus on the highest-risk cases first |

| Reconciliation exception analysis | Explains and clusters mismatches between systems | Medium | Reconciliation-ready ledger and provider data | Helps reduce manual investigation effort on settlement discrepancies |

| Merchant payout risk scoring | Scores merchants based on transaction behavior | Medium-High | Merchant transaction history, back-office review flow | Informs, not replaces, payout hold decisions |

| Payment routing suggestions | Recommends optimal rail/provider per transaction | Medium | Multi-provider routing data, cost/performance metrics | Improves cost and success rates while rules stay in control |

| Back-office reporting assistant | Summarizes operational and financial reports | Low | Reporting layer with governed data access | Saves analyst time on recurring reporting tasks |

| Customer behavior insights | Surfaces usage patterns and segment trends | Low | Aggregated, anonymized transaction data | Supports product decisions without touching individual accounts |

| Dispute/chargeback triage | Classifies and prioritizes incoming disputes | Medium | Dispute case data, transaction history | Speeds initial triage; final decisions stay with operators |

Architecture: AI beside the core, not inside the ledger

A workable architecture keeps AI adjacent to the transaction core rather than embedded inside it:

The ledger stays the single source of truth. The AI layer reads from it – never writes to it directly. Every recommendation the AI produces gets logged alongside whatever action a human or rules engine eventually took, which matters as much for audit and model evaluation as it does for compliance.

SDK.finance helps FinTech teams build this foundation with an API-first Transaction Platform, real-time Ledger, reconciliation-ready records, and back-office workflows that AI services can safely connect to.

AI in payment software: why PSPs and EMIs need the same foundation

This is not only a banking story. PSPs, EMIs, digital wallets, merchant platforms, cross-border payment products, remittance providers, and embedded finance platforms face the same infrastructure requirements – often with higher transaction volumes and more currencies to manage.

For these companies, the highest-value AI use cases tend to cluster around:

- Settlement and reconciliation – matching high volumes of transactions across multiple providers and corridors.

- Fraud detection at scale – spotting patterns across large transaction volumes faster than manual review allows.

- Merchant balance and payout risk – flagging unusual merchant behavior before payouts go out.

- Multi-currency flow monitoring – surfacing anomalies across currency pairs and exchange operations.

None of this works without the same foundation: real-time ledgers, currency-specific balances, reconciliation-ready records, and a back-office layer where AI-surfaced items land for review.

Build vs. buy: why infrastructure shortcuts matter

Companies that already have a working transaction platform, ledger, API layer, and back-office tend to move faster on AI – not because they have better models, but because they are not spending the first year building the plumbing AI needs to be useful and safe.

If your banking software or payment software already has APIs, a real-time ledger, reconciliation tooling, roles and permissions, and compliance workflows, adding an AI layer is a matter of integration. If those pieces do not exist yet, AI becomes the least of the engineering effort – most of the work is building, or rebuilding, the transaction and ledger core it needs to sit on top of.

AI-generated code can also create supply-chain risk

AI risk in banking software is not limited to customer-facing chatbots or fraud models. It can also enter the software supply chain through AI-generated code. Security researchers have documented a threat known as slopsquatting, where code-generating LLMs invent non-existent package names. Attackers can then register malicious packages under those hallucinated names, hoping developers will install AI-suggested dependencies without checking whether they are legitimate.

In a large-scale study of 576,000 AI-generated code samples, researchers found that hallucinated packages appeared in at least 5.2 percent of outputs from commercial models and 21.7 percent of outputs from open-source models.

For banks, PSPs, EMIs, and FinTech companies, this matters because even a small unverified dependency can become a path into payment infrastructure, customer data, internal APIs, or transaction systems. AI-generated code should therefore go through the same controls as any other production code: dependency validation, software composition analysis, locked package versions, code review, security testing, and approval before deployment.

This reinforces the same principle: AI can accelerate development and operations, but it should not bypass verification layers in financial software.

This is where a modular, API-first platform like SDK.finance fits – not as a source of built-in AI, but as the transaction and ledger foundation that makes AI integration realistic and safe.

How SDK.finance supports AI-ready financial products

Image source: SDK.finance banking software interfaces

SDK.finance provides the transaction, ledger, API, and back-office foundation that AI services can connect to – it does not claim to be an AI product itself. What it offers is the infrastructure layer described above, already built:

- Transaction Platform covering wallets, accounts, payments, merchants, fees, limits, and contracts

- Finance Ledger – a real-time double-entry accounting layer that turns product events into balanced, auditable journal entries

- Multi-currency balances for products operating across corridors and asset types

- Reconciliation and settlement support including structured records suited to automated matching

- AML/fraud officer workspace for human-in-the-loop review of flagged activity

- Flexible reporting across transactions, accounts, and operations

- Roles and permissions for controlling who can act on AI-surfaced recommendations

- 570+ REST APIs giving AI services and internal tools structured access to platform data

- Source code access for teams that need to customize workflows as AI use cases evolve

- Security and compliance credentials including PCI DSS Level 1 Service Provider status, ISO 27001:2022 certification, and GDPR-ready architecture

In practice, this means a bank, PSP, EMI, or FinTech can connect AI services to SDK.finance APIs and event data – for fraud triage, reconciliation analysis, or reporting – while the ledger itself remains the deterministic, auditable system of record it needs to be.

AI-readiness checklist

Before investing heavily in AI features, it is worth checking whether the underlying infrastructure can actually support them:

- Can you access transaction data via APIs?

- Are balances tracked in a real-time ledger?

- Are ledger postings auditable and traceable?

- Can you separate balances by currency and by entity?

- Do you have reconciliation-ready transaction records?

- Can operators review and approve AI-suggested actions before they execute?

- Are roles and permissions configured for AI-surfaced workflows?

- Are logs available for audit and compliance review?

- Can your infrastructure support dedicated fraud and compliance workflows?

- Can your team customize the system as AI use cases evolve?

If most of these are no, the priority is not picking a model – it is building the infrastructure the model will depend on.

Conclusion

AI in banking software is not mainly a model problem – it is an infrastructure, data, ledger, governance, and workflow problem. The value on the table is real, but so is the gap between pilots and production, and infrastructure is usually what separates the two. The companies that get real value from AI are not necessarily using the most advanced models; they are the ones whose transaction platforms, ledgers, and back-office workflows were ready for AI to plug into safely. Getting that foundation right – clean APIs, a real-time ledger, reconciliation-ready data, and clear human approval points – is what turns AI from a demo into something regulators, auditors, and customers can actually trust.

Explore how SDK.finance can provide the transaction platform, ledger, and API foundation for AI-ready banking and payment products.

Create your digital banking solution in weeks

Talk to Our Team