The Fragile Paradox of Modern FinTech

The modern payment stack is a marvel of engineering: it can authorize transactions in milliseconds, capture funds across global jurisdictions, and trigger complex settlement logic. This article is designed for FinTech leaders, technical architects, and CFOs, offering a deep dive into payment reconciliation as a foundational pillar of financial infrastructure.

Payment infrastructure does not prove itself when a transaction is authorized, captured, or even settled. It proves itself only when a business can explain, with absolute confidence and at transaction-level granularity, what happened to every cent, what fees were applied, and what remains unresolved. When the internal ledger diverges from bank statements or PSP reports, the “innovation” facade crumbles into manual spreadsheets and regulatory risk. Reconciliation is the control layer that transforms raw payment processing into reliable financial infrastructure.

Redefining Reconciliation for the FinTech Era

What Payment Reconciliation Actually Means

Payment reconciliation in FinTech is the automated process of verifying operational truth by matching internal transaction records against external data from PSPs, banks, and networks.

Unlike traditional finance, which might compare a bank statement once a month, fintech reconciliation operates continuously and at transaction-level granularity. It manages high-velocity variables including gross-to-net settlements, FX spreads, tiered fee structures, and asynchronous events like chargebacks and partial refunds.

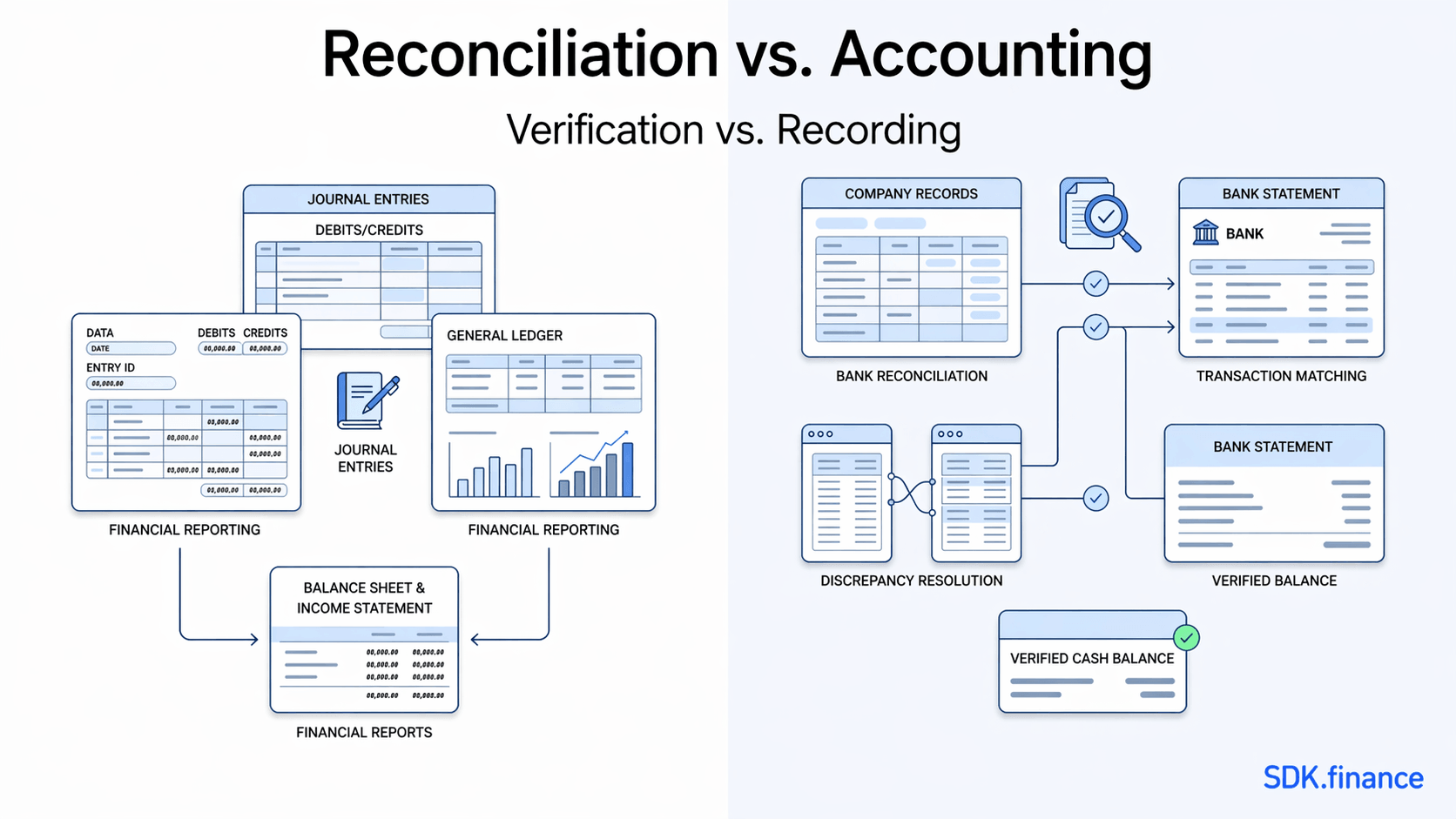

Reconciliation vs. Accounting: Verification vs. Recording

While accounting records financial outcomes for reporting, reconciliation verifies the integrity of the underlying data. Accounting tells you what was booked in the General Ledger; reconciliation tells you if the money actually exists in the bank.

Comparison of Financial Functions

| Feature | Payment Reconciliation | General Ledger (Accounting) |

| Primary Goal | Operational integrity & “Proof of Cash” | Financial reporting & Tax compliance |

| Granularity | Individual transaction/event level | Aggregated account balances |

| Data Source | PSP logs, API responses, Bank files | Internal journal entries |

| Timing | Continuous/Daily | Periodic (Monthly/Quarterly) |

| Risk Focus | Operational risk & leakages | Reporting accuracy |

The “Truth” Gap: Where Payments vs. Reality Diverge

The tension in a payment stack exists because systems are inherently decoupled. A transaction might be “Succeeded” in your database but “Pending” at the processor, or “Settled” at the processor but “Held” by the bank for compliance review.

Without a robust reconciliation engine, these discrepancies become “phantom balances” that distort your financial health. This leads to dangerous questions asked too late:

- Did we receive the full amount we expected?

- Why does the payout not match the transaction volume?

- Are we missing money, or just missing visibility?

The Architecture of Failure: Where Infrastructure Breaks

Common Failure Modes in Payment Flows

Payment infrastructure breaks when asynchronous events or system divergences disrupt the expected transaction lifecycle.

Real-World Failure Scenarios

| Scenario | What Happens | Risk |

| The Fees Leak | PSP settles $97.50 for a $100 transaction | Margin leakage/Expected cash differs |

| The Refund Orphan | Refund initiated internally but fails at the gateway | Customer risk/Paper-only refund |

| FX Volatility | Rate fluctuations during settlement window | Treasury exposure/”Dust” balances |

| The Chargeback Paradox | Funds clawed back after payout marked complete | Unexpected financial loss |

| Auth vs. Capture | Auth approved, but capture fails | Revenue loss |

Identifying “Breaks” and Exception Handling

In regulatory terms, a “break” is a discrepancy that cannot be automatically matched. Mature infrastructure treats breaks as data points, categorizing them by aging (how long they have been open) and materiality (how much money is at risk).

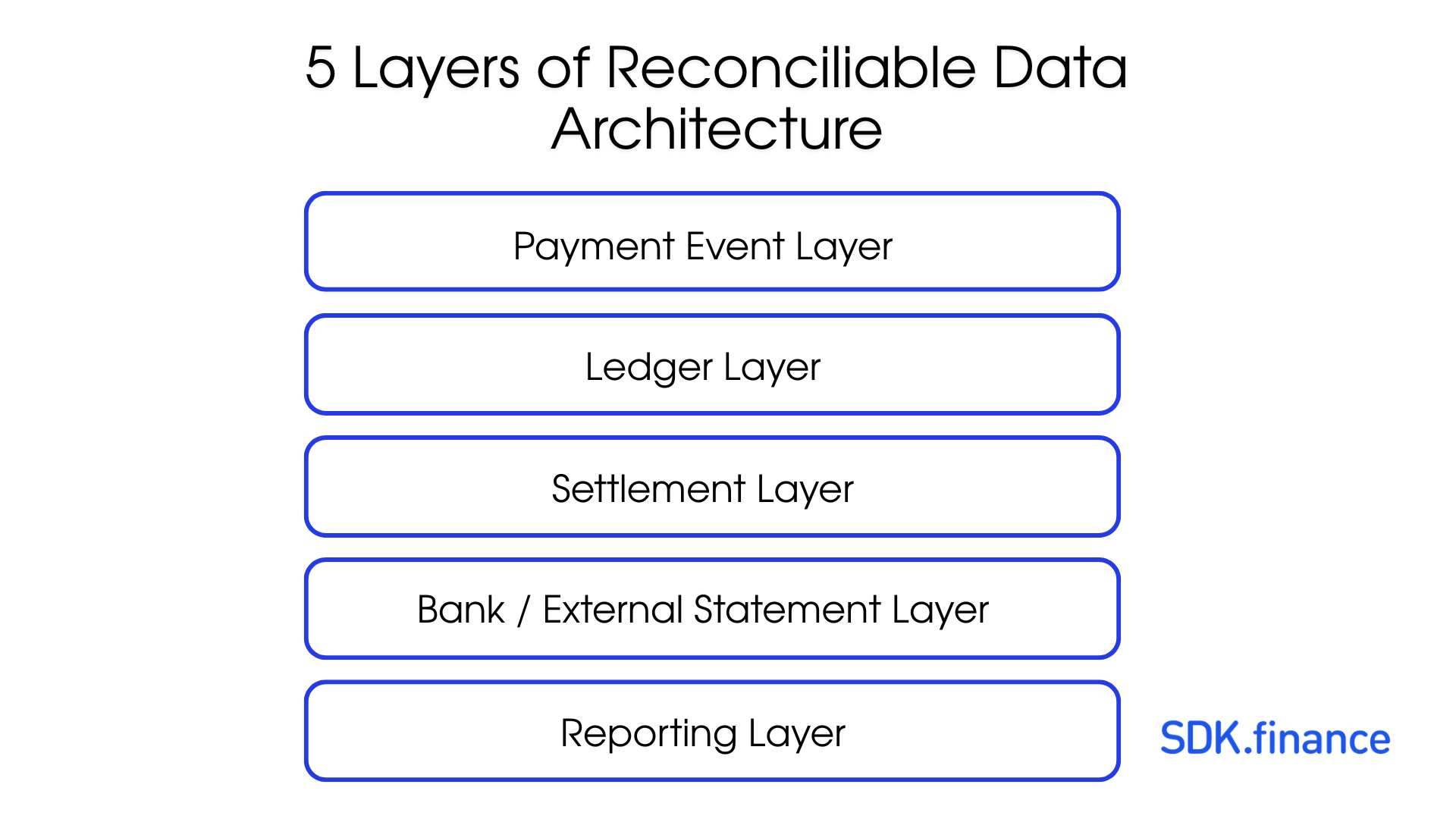

Building a Reconcilable Payment Stack

The 5 Layers of Reconciliable Data Architecture

Reliability is achieved only when these five layers are linked by deterministic, unique IDs:

- Payment Event Layer: Authorizations, captures, refunds, chargebacks.

- Ledger Layer: Double-entry records of internal operational balances.

- Settlement Layer: PSP and network-level outcomes (processor reports).

- Bank / External Statement Layer: Actual cash movement in bank statements, including transactions initiated via pay by bank API that settle directly over bank rails.

- Reporting Layer: Aggregated outputs for finance and compliance.

Settlement Is Not Reconciliation

Settlement answers “Did money move?” while reconciliation answers “Do all systems agree on what happened?”. Settlement is the physical transfer; reconciliation is the intellectual process of proving that the settled amount accurately reflects the sum of successful transactions minus fees and adjustments.

The Reconcilable Data Model: Essential Schema Fields

Automated reconciliation (“Auto-match”) is only as strong as its data model. At minimum, the schema must include:

- Identifiers: order_id, payment_attempt_id, processor_tx_id, settlement_batch_id, and ledger_entry_id .

- Timestamps: created_at, authorized_at, captured_at, settled_at, and reconciled_at. Without these links, reconciliation becomes a manual investigation rather than a validation.

The Strategic Core: Application Ledgers vs. General Ledgers

Why FinTechs Need a Transactional Ledger

A General Ledger (GL) is designed for aggregated, periodic financial reporting. A Transactional Real-TimeLedger (or operational ledger) is designed for granular, real-time transaction tracking and balance management.

| Feature | General Ledger | Transactional Ledger |

| Purpose | Reporting | Operational truth |

| Granularity | Aggregated | Transaction-level |

| Reconciliation Support | Limited | Critical |

SDK.finance Scenario:

In a multi-currency wallet swap (EUR to USD), the Transactional Ledger handles the atomic update of two balances simultaneously. If settlement is delayed, the Transactional Ledger keeps funds “blocked,” ensuring the FinTech never over-extends its reserves.

Atomic Transactions and Idempotency

A reconcilable infrastructure must be idempotent: no matter how many times a “settled” webhook is received, the ledger must only record it once. This prevents “double-counting,” a hallmark of professional-grade core banking software.

Measuring Success: Maturity & KPIs

What Mature Reconciliation Looks Like at Scale

Mature reconciliation is not defined by the absence of mismatches, but by how quickly they are resolved.

- Continuous Processing: Moving away from batch processing toward real-time matching.

- Automated Controls: Exception queues, “Maker-Checker” (four-eyes) controls, and explicit aging rules.

- Auditability: A full audit trail that satisfies regulatory requirements.

Essential KPIs for the COO and CFO

- Auto-Match Rate: Transactions matched without human intervention (Target: >98%).

- Aging of Open Breaks: Days a discrepancy remains unresolved (Target: <48 hours).

- Unreconciled Balance Exposure: Total dollar value of currently unmatched transactions.

- Fee Leakage: Delta between expected and actual PSP fees.

The Regulatory and Business Imperative

Safeguarding Compliance (PSD3/EMD)

Under PSD3 and E-Money regulations, firms must perform daily external reconciliation to ensure customer funds are insulated from corporate funds. Failure to reconcile internal customer ledgers with safeguarding accounts is a direct breach of license.

Reconciliation as a Competitive Advantage

Beyond compliance, strong reconciliation enables:

- Faster Scaling: Adding new PSPs without hiring more back-office staff.

- Trust: Instant, accurate balance updates for end-users.

- Margin Visibility: Identifying precisely where fees and FX are eroding profit.

Conclusion: The Foundation of Financial Integrity

The history of FinTech is littered with companies that scaled transactions but failed at reconciliation. If payments move money, reconciliation keeps score. In modern fintech, keeping score is not a side function – it is the core of the game. As you move from a Minimum Viable Product (MVP) to a regulated financial institution, the “plumbing” of your infrastructure becomes more important than the “porcelain” of your UI.

Modernize Your Financial Core

Don’t let your growth be throttled by manual spreadsheets. Build on a foundation of operational truth with SDK.finance’s enterprise-grade Transactional Ledger software. Explore the SDK.finance Real-Time Ledger Solution.