A double-entry ledger is the core system that records how money moves inside a fintech product. Every transaction is captured as balanced entries across accounts, helping keep balances, transaction history, and downstream reporting aligned.

In modern fintech systems, this is not just accounting logic. A double-entry ledger acts as a system of record for money movement, supporting real-time balances, audit trails, and reconciliation workflows across wallets, payments, and settlements.

What is a double-entry ledger?

A double-entry ledger is a financial ledger where every transaction is recorded as at least two entries: a debit in one account and a corresponding credit in another.

The core principle is straightforward:

- Every movement of value has a source and a destination.

- The total of all debits equals the total of all credits.

- The system remains mathematically consistent over time.

In most fintech products, double-entry logic is the foundation for balance integrity and transaction consistency. Depending on the architecture, it can function as an operational product ledger or as part of a broader accounting system.

How double-entry accounting works

Double-entry accounting is based on three core ideas:

- Paired debit and credit entries

- Balanced transactions

- A chronological record of financial events

In software systems, this is typically implemented through atomic transaction posting, where all entries in a transaction are committed together or not at all.

This helps prevent partial updates and supports consistency across transaction-processing workflows.

What counts as an account in a ledger system

In a FinTech ledger system, accounts represent different types of value storage and movement, not just traditional accounting categories.

They can include:

- Customer wallet balances

- Merchant funds

- Platform fees and revenue

- Treasury or liquidity accounts

- Settlement or clearing accounts

This structure allows fintech systems to model real-world financial flows while maintaining consistent accounting logic.

Why FinTech products rely on double-entry ledgers

FinTech systems operate across multiple providers, payment rails, and asynchronous processes. That creates a constant risk of inconsistencies between internal records and actual funds.

A double-entry ledger helps reduce this risk by acting as a control layer that structures financial events into verifiable records.

Wallets, customer balances, and internal transfers

Wallet-based products depend on accurate ledgering to:

- Track balances in real time

- Support peer-to-peer transfers

- Prevent inconsistencies during concurrent operations

Without structured ledger logic, systems often fall back to simple balance updates, which are much more likely to break under scale or concurrency.

PSP flows, settlements, and fees

Payment flows typically involve:

- Incoming funds from users

- Platform fees and commissions

- Payouts to merchants

- Settlement with external providers

A ledger helps ensure these flows are recorded consistently and can later be reconciled against external systems.

Refunds, reversals, and corrections

Modern FinTech products must support more than successful payments. They also need to handle:

- Refunds

- Reversals

- Chargebacks

Instead of modifying historical data, ledger systems record compensating entries. This preserves a complete and auditable transaction history.

Double-entry ledger vs general ledger

A common source of confusion is treating all ledgers as the same. In practice, fintech products often rely on two different layers.

| Dimension | Product (Double-Entry / Transactional) Ledger | General Ledger |

|---|---|---|

| Primary purpose | Track financial movements and maintain real-time balances | Organize financial data for reporting and compliance |

| Core function | Records transactions as balanced debit/credit entries | Aggregates and structures financial data into accounts |

| System role | Operational system of record for money movement | Accounting and reporting system |

| Timing | Real-time or near real-time updates | Periodic or event-driven updates (often downstream) |

| Granularity | Transaction-level (high detail) | Aggregated financial data |

| Balance logic | Drives actual balances used in product flows | Reflects summarized balances for reporting |

| Use cases | Wallets, payments, transfers, fees, settlements | Financial statements, audits, compliance reporting |

| Data model | Entry-based (debits and credits per transaction) | Account-based (chart of accounts structure) |

| Immutability | Typically append-only with full transaction history | Depends on accounting system (often controlled adjustments allowed) |

| Users | Product, engineering, payments operations | Finance, accounting, auditors |

| External alignment | Supports reconciliation with PSPs, banks, rails | Supports regulatory and financial reporting standards |

| Error handling | Corrections via reversing entries | Adjustments, accruals, accounting entries |

| Dependency | Independent runtime system | Often receives data from product ledger |

How they work together

- A product ledger (double-entry), also called an operational or transactional ledger, tracks money movement in real time.

- The general ledger consumes this data and organizes it into a structure required for accounting, reporting, and compliance.

In most FinTech architectures, transactional ledger acts as the source of operational truth, while the general ledger acts as the source of financial reporting.

Why many FinTech companies need both

Most FinTech architectures use both layers:

- Product ledger for operational accuracy

- General ledger for reporting and compliance

What makes a modern ledger system different

A modern FinTech ledger does more than keep debits and credits balanced. It also supports the operational requirements of real-time financial products.

Real-time balance updates

For most modern financial products, delayed balance updates create both operational and customer-experience risks.

Real-time balances are essential for:

- Authorization decisions

- Available balance checks

- Accurate customer-facing balance displays

Atomic posting and transaction integrity

Modern ledgers rely on atomic posting, where all entries within a transaction are processed as a single unit.

This helps ensure:

- No partial transactions

- Consistent balances across accounts

- Reliable recovery from failures

Immutable records and auditability

Modern ledgers are typically:

- Append-only

- Immutable

- Audit-ready

Corrections are recorded as new entries, not retroactive updates.

Sub-accounts, multi-currency, and segregation

A single system may support:

- Millions of user sub-accounts

- Multiple currencies per account

- Segregation of funds across users, merchants, and the platform

This is especially important for PSPs, wallets, embedded finance products, and digital banks.

Reconciliation readiness

A ledger should make reconciliation easier by:

- Structuring transactions consistently

- Storing references to external systems

- Enabling matching against bank or PSP data

A practical FinTech example

The examples below are simplified for clarity. Account structure and debit or credit direction depend on the ledger model and chart of accounts used by a given platform.

Example 1: wallet top-up

A user deposits $100.

Simplified ledger entries:

- Debit: external funding account

- Credit: user wallet

The result is a higher wallet balance, while the overall ledger remains balanced.

Example 2: transfer plus fee

A user sends $100 to another user and pays a $2 fee.

Simplified ledger entries:

- Debit $102 from the sender

- Credit $100 to the recipient

- Credit $2 to the platform fee account

All movements are recorded within one transaction, preserving a full record of both the transfer and the fee.

Example 3: refund or reversal

A $100 payment is refunded.

Simplified ledger entries:

- Debit merchant account

- Credit user wallet

The original transaction remains unchanged. The refund is recorded as a separate event, which keeps the history complete and auditable.

Common mistakes in ledger design

Treating balances as editable values

Storing only balances without transaction history creates:

- Limited auditability

- Reconciliation challenges

- Poor traceability when something goes wrong

Ledger entries should remain the source of truth, even when systems use cached balances for performance.

Mixing product operations with reporting logic

Combining operational and reporting layers often leads to:

- Inconsistent data models

- More complicated reconciliation

- Unnecessary system complexity

Ignoring idempotency, concurrency, and reconciliation

Double-entry alone is not enough.

Reliable FinTech systems also require:

- Idempotent APIs

- Concurrency control

- Reconciliation workflows

Together, these controls help ensure financial correctness in real-world conditions.

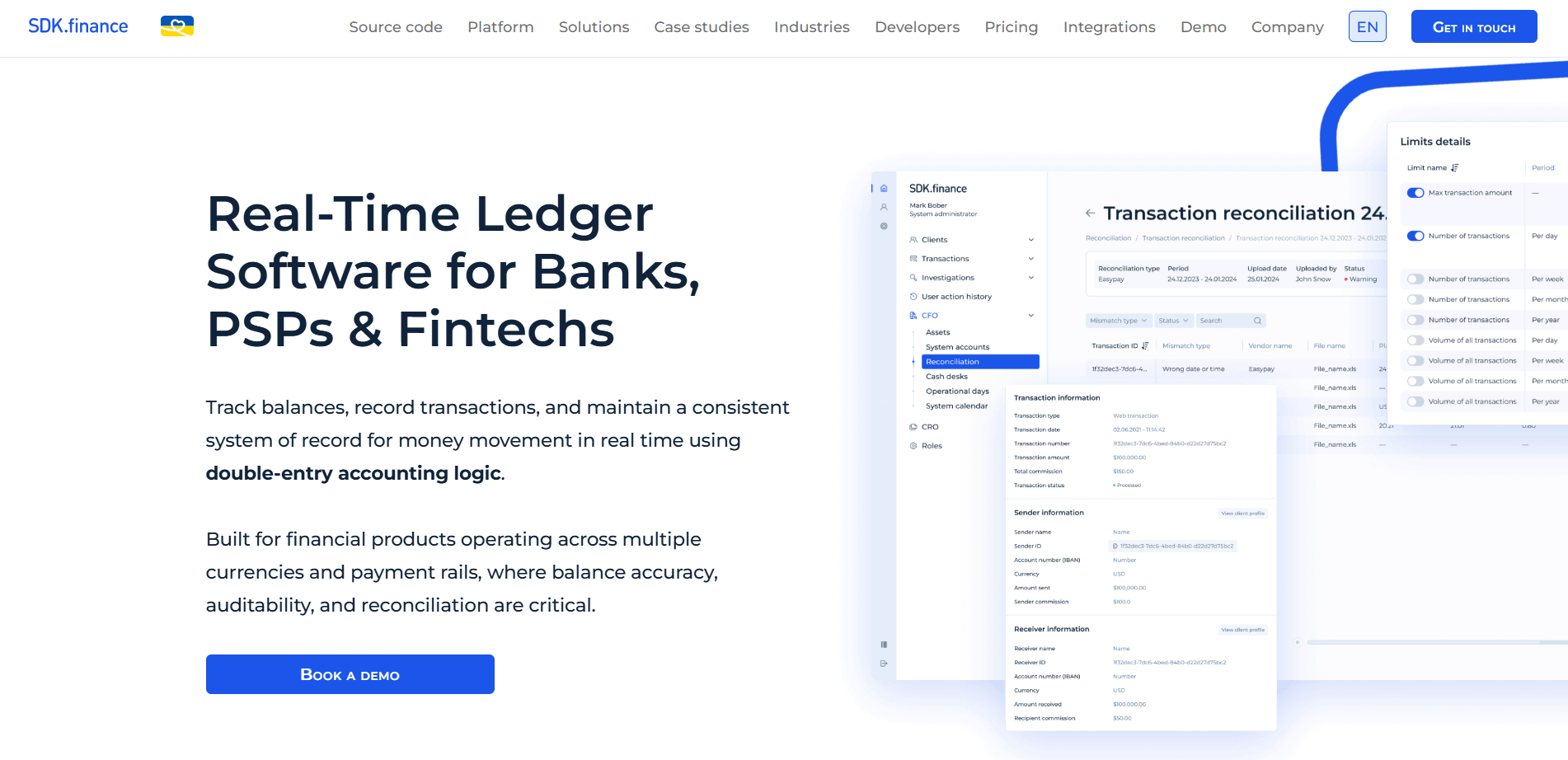

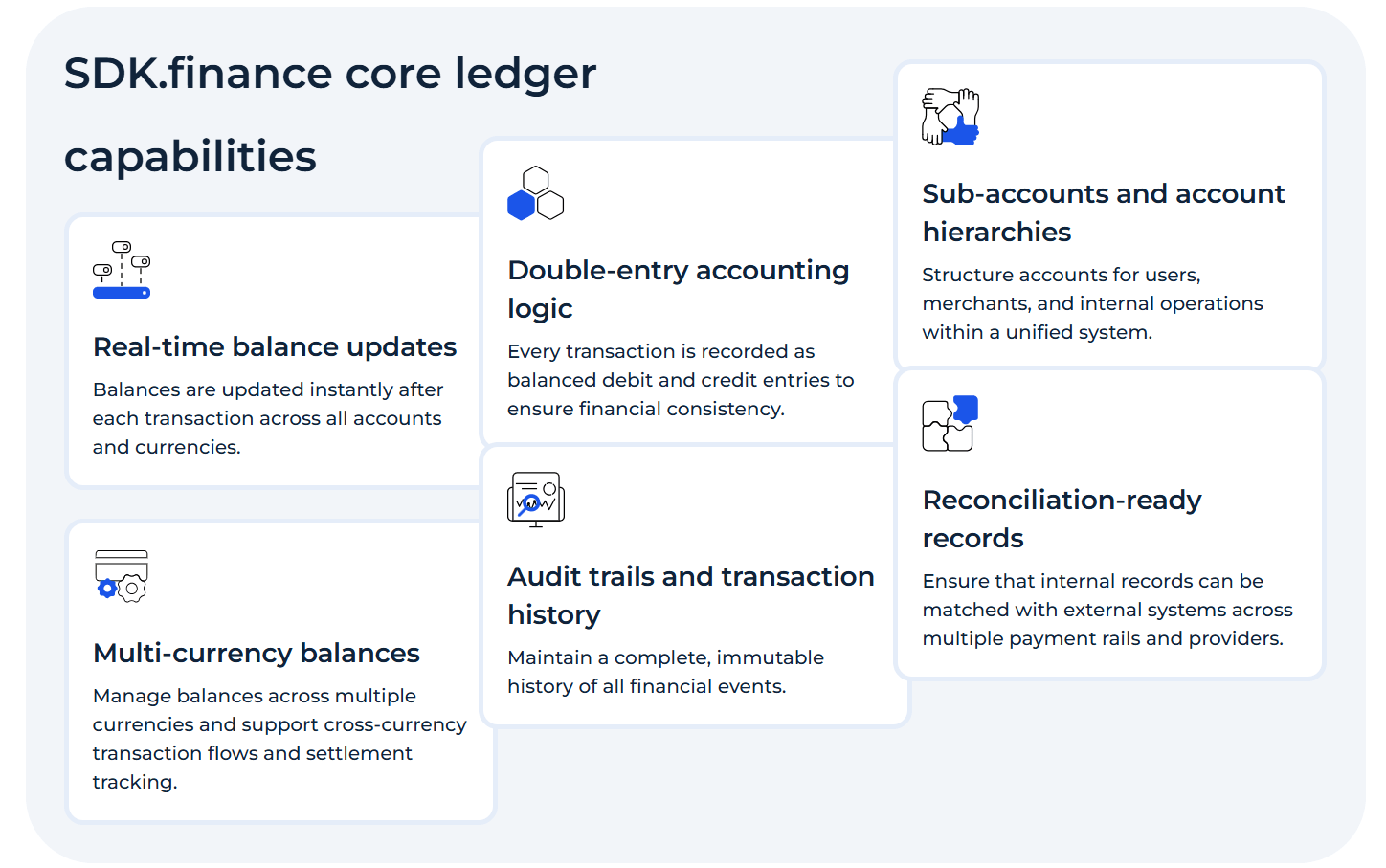

How SDK.finance supports real-time ledger operations

SDK.finance provides real-time ledger software for FinTech teams that need:

- Accurate balances

- Transaction integrity

- Reconciliation-ready records

The platform supports:

- Double-entry transaction processing

- Real-time balance updates

- Multi-currency accounts

- Integration with external payment systems

This helps FinTech teams reduce operational complexity while maintaining financial correctness at scale.

Conclusion

A double-entry ledger provides the structural foundation for managing money in FinTech systems.

While it originates from accounting, in modern products it functions as an operational system of record, supporting real-time balances, transaction traceability, and reconciliation workflows.

For FinTech teams building scalable financial products, it remains one of the most reliable ways to maintain balance integrity while managing complexity over time.

Explore SDK.finance real-time ledger software to see how you can implement a production-ready ledger architecture without building it from scratch.