A wallet ledger is the operational balance layer behind digital wallets, payment apps, PSP flows, and stored-value products. It records every money movement – top-ups, transfers, fees, refunds, and payouts – updates balances consistently, preserves an immutable transaction history, and supports reconciliation against external payment rails.

In many FinTech architectures, a wallet ledger also functions as a payments ledger for internal value movement. It is not just a number in a database; it is the system that explains how every balance was formed and why it changed.

The Short Answer

A wallet ledger is a real-time system of record that:

- Records every financial event related to a user wallet or payment account

- Keeps balances accurate and consistent across all operations

- Supports internal transfers, fee collection, refunds, reversals, and payouts

- Acts as the authoritative source for stored value – what each user can spend, right now

In practice, a wallet ledger often acts as a payments ledger for internal value movement within the product.

What Is a Wallet Ledger?

At its most basic, a wallet ledger is a structured log of financial events that determines what a user's balance is at any given moment. Where a simple database column stores a single number representing a balance, a wallet ledger stores the sequence of events that explain how that number was reached. Each event - a top-up, a transfer out, a fee - is recorded as an entry. The current balance is derived from this history, not stored as a mutable field someone can accidentally overwrite.

This distinction matters for two reasons. First, it makes the system auditable: any question about why a balance is what it is can be answered by reviewing the event history. Second, it greatly reduces the risk of balance drift, because the visible balance is tied back to the same underlying source of truth rather than maintained as an isolated editable field.

A wallet ledger is sometimes called a product ledger or operational ledger to distinguish it from accounting-focused general ledgers. Its job is to power the live experience of a financial product, not to produce year-end financial statements.

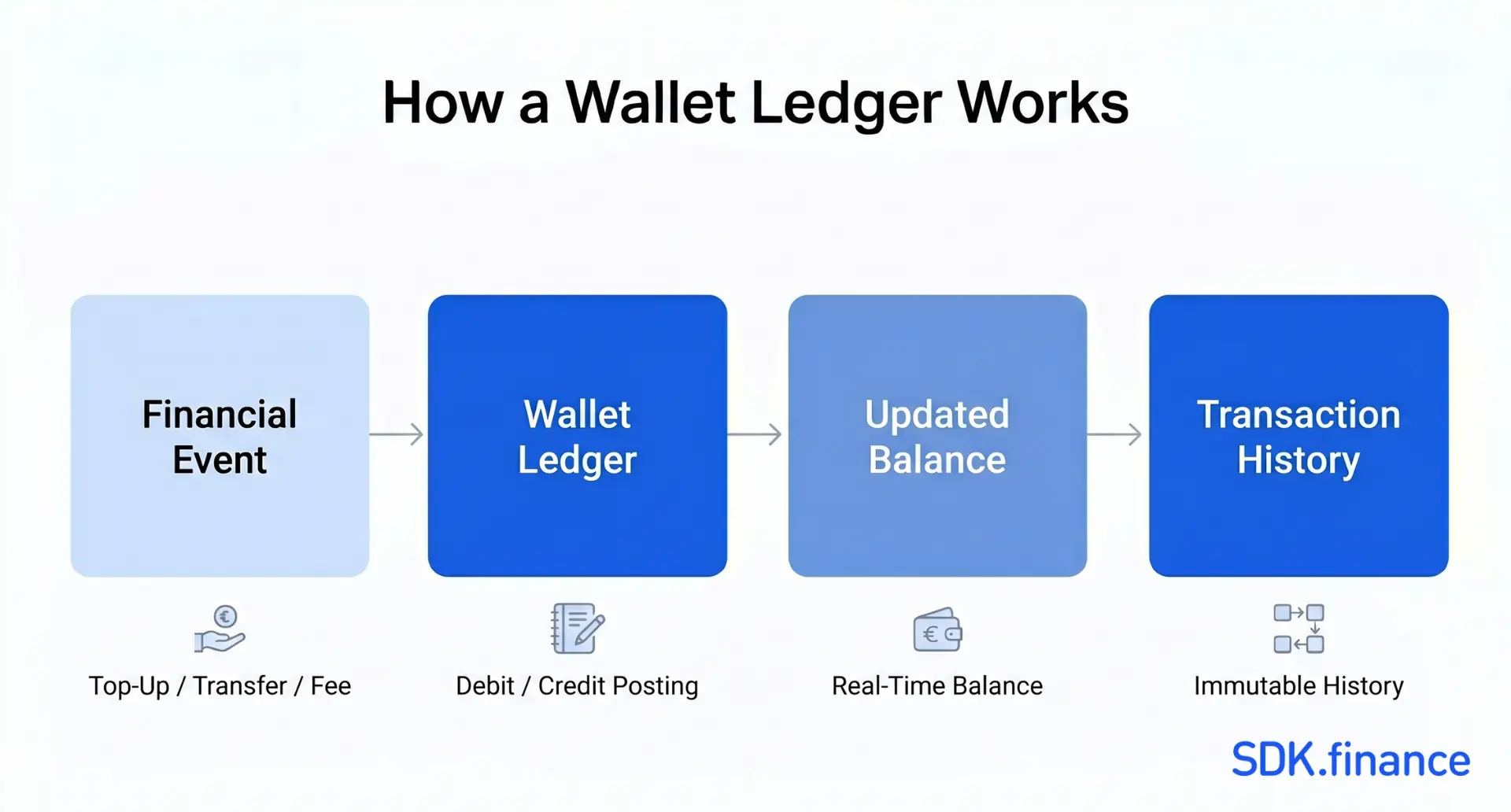

How a Wallet Ledger Works

Recording money movement between accounts

Every financial event in a wallet system becomes a ledger posting. When a user tops up their account, a posting records the credit. When they send funds to another user, a debit is recorded on the sender’s account and a credit on the recipient’s. When the platform charges a fee, that too becomes a posting – to the user’s account and to the platform’s revenue account.

The key principle here is that money is never created or destroyed. Every debit has a corresponding credit somewhere in the system. This zero-sum structure is what makes the ledger reliable: it is mathematically difficult for funds to appear or disappear without a traceable event.

Updating balances in real time

Users expect to see their balance change the moment they complete a transfer or receive a payment. A wallet ledger must support this. In practice, high-volume systems maintain a computed “balance after this entry” on each ledger row, or cache a running balance that is updated atomically with each new posting. The goal is the same: the balance the user sees must reflect posted activity quickly and consistently.

Preserving transaction history

Because entries in a wallet ledger are immutable – never deleted, never modified – the entire history of an account remains intact. Errors are corrected through compensating transactions, not by editing existing records. This gives operations teams, compliance officers, and auditors the ability to reconstruct the full history of any account at any point in time.

What a Wallet Ledger Typically Tracks

A wallet ledger records the full lifecycle of funds within a payment product:

- Wallet top-ups – funds loaded from a card, bank account, or external provider

- Wallet-to-wallet transfers – internal movements between user accounts on the same platform

- Card or bank-funded loads – deposits triggered by external payment rails

- Fees and commissions – deducted at the time of a transaction or on a schedule

- Payouts – withdrawals to an external destination (bank account, card, crypto address)

- Refunds and reversals – money returned to a user after a failed or cancelled transaction

- Settlement-related events – entries that record the reconciliation of virtual balances against external bank positions

Each of these event types requires specific handling in the ledger’s posting logic, but all share the same structure: a debit somewhere, a credit somewhere else, and a full record of when it happened and why.

Why PSPs, Neobanks, and Payment Apps Need a Wallet Ledger

PSPs and payment processors

A payment service provider handles money on behalf of many merchants. Each merchant has a balance with the PSP — funds collected from their customers, minus processing fees, minus amounts already paid out. The wallet ledger is what tracks this at the individual merchant level.

When a customer pays a merchant through the PSP, the ledger records the incoming funds, calculates the platform’s processing fee, credits the net amount to the merchant’s account, and records the settlement event when the PSP transfers funds to the merchant’s bank. Without a dedicated ledger, teams often end up relying on slower, more manual, and less scalable reconciliation processes as transaction volumes grow.

Neobanks and digital banking apps

Neobanks hold customer money and must give users accurate, real-time visibility into their balances. Many also offer product features like savings pockets, sub-accounts, or round-up rules that require tracking money across multiple virtual accounts under a single user.

The wallet ledger is what makes this possible. It tracks each sub-account separately while keeping the total balance coherent. It records every movement between pockets, every fee charged, every interest credit. And it provides the foundation for reconciling user-visible balances against the real bank account where the actual funds are held.

Payment apps and stored-value wallets

A closed-loop payment app – where users top up a balance and spend it within the platform – is entirely dependent on a wallet ledger. The ledger records what each user loaded, what they spent, and what they still hold. Since the money never leaves the platform for most transactions, the ledger is the only source of truth. P2P transfers between users are pure ledger entries: a debit on one account, a credit on another, with no movement of real funds at all.

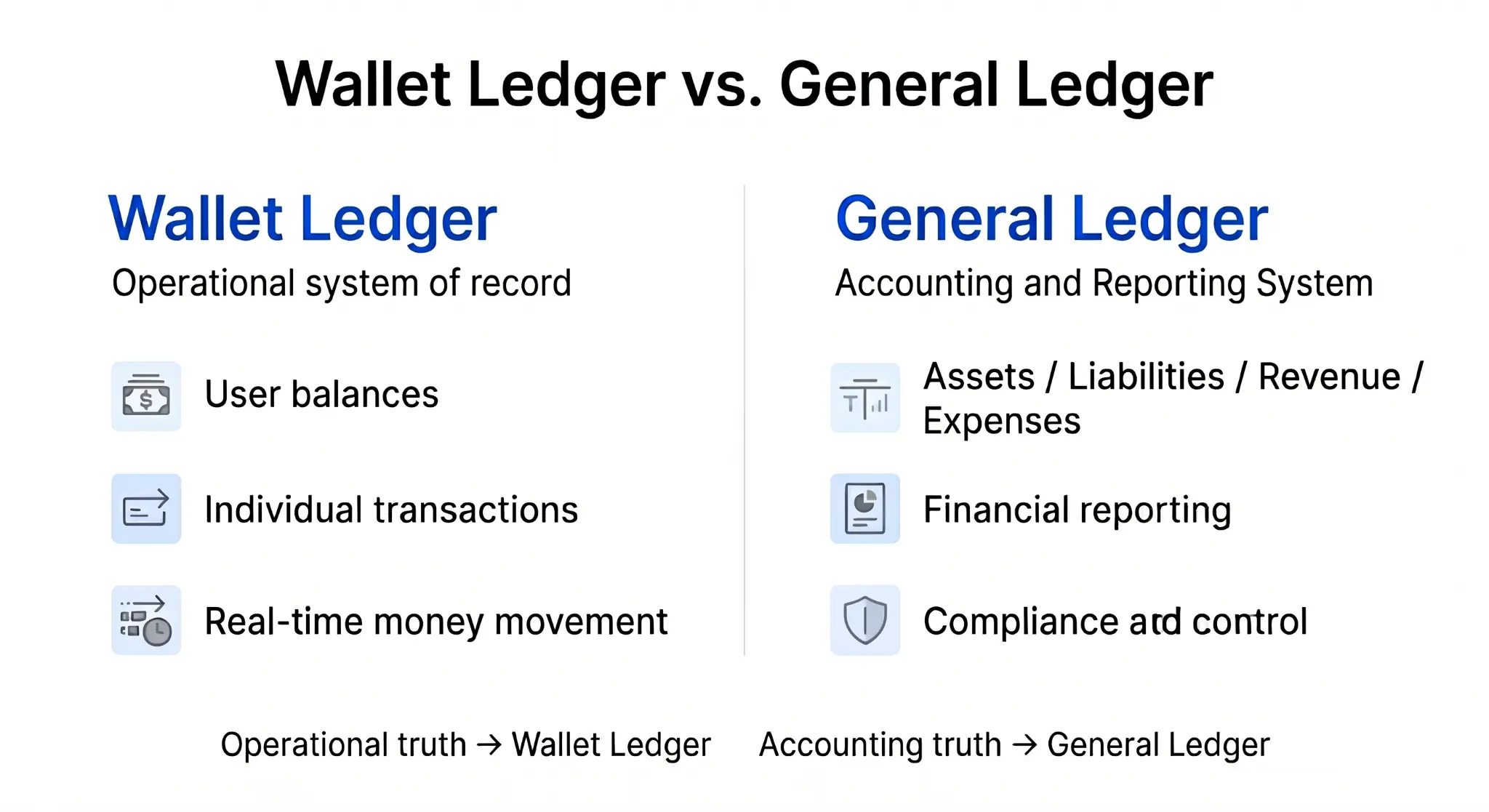

Wallet Ledger vs. General Ledger

These two systems serve different purposes and operate at different layers.

A wallet ledger is an operational system. It works at the level of individual user accounts and individual transactions. Its job is to power the product: to track what a user can spend now, record every balance-changing event, and preserve the history behind that balance.

A general ledger is an accounting system. It works at the level of financial categories such as assets, liabilities, revenue, and expenses. Its job is to support reporting, compliance, and financial control across the business.

In a well-architected FinTech stack, the wallet ledger is the source of operational truth, while the general ledger structures that truth for accounting and reporting.

Wallet Ledger vs. Core Banking System

A core banking system manages the broader lifecycle of banking products: customer onboarding, account configuration, compliance workflows, product rules, and regulated banking operations.

A wallet ledger is narrower. It is the balance and posting layer responsible for recording what happened to money and keeping balances accurate. In many modern architectures, the wallet ledger supports real-time balance visibility and transaction integrity, while the core banking system manages the wider operating environment around it.

Common Wallet Ledger Use Cases

Customer top-ups

A user adds EUR 50 to their digital wallet via debit card. The wallet ledger records a credit of EUR 50 to the user’s wallet account and a debit to the platform’s pooled bank account. The user sees their balance update immediately. The entry is timestamped and linked to the card payment’s reference ID for reconciliation.

Wallet-to-wallet transfers

User A sends EUR 20 to User B within the same app. The wallet ledger records a debit of EUR 20 from User A’s account and a credit of EUR 20 to User B’s account. Both entries happen atomically – either both post or neither does. There is no intermediate state where one account is debited but the other is not yet credited.

Merchant payouts

A marketplace holds funds on behalf of sellers. When a payout is triggered, the wallet ledger records a debit from the merchant’s balance and a credit to a payout-in-progress account. When the bank transfer completes, a final entry marks the settlement as resolved. The full chain is auditable at every step.

Fee collection

When a platform charges a 1.5% fee on each transfer, the wallet ledger captures this as a separate posting: a debit from the user’s account for the fee amount, and a credit to the platform’s revenue account. The fee is not subtracted from the transfer silently – it has its own entry with its own timestamp and reference.

Refunds and reversals

A user’s payment failed, and their funds need to be returned. Rather than editing the original entry, the wallet ledger records a new transaction: a credit back to the user’s account, and a debit from the merchant’s or platform’s account. The original failed payment remains in the history. The refund is a separate, traceable event.

What Makes a Modern Wallet Ledger Reliable

Not every implementation delivers the same reliability. These are the characteristics that separate a robust wallet ledger from a fragile one:

- Real-time balance visibility. Balances must reflect posted events immediately. Users should not see stale data after a transfer completes.

- Double-entry logic. Every transaction must produce balanced entries – a debit and a corresponding credit. This mathematical consistency is what prevents money from appearing or disappearing unexpectedly.

- Immutable records. Entries cannot be edited or deleted after posting. Corrections are made through compensating entries, not overwrites. This is what makes the ledger auditable.

- Reconciliation readiness. Each entry should carry enough metadata – external reference IDs, provider identifiers, timestamps – to be matched against bank statements and payment processor records during reconciliation.

- Support for sub-wallets and sub-accounts. A single user may have multiple virtual accounts – a main balance, a savings pocket, a cashback wallet. The ledger must model these as separate account objects while keeping the aggregate balance coherent.

Common Mistakes in Wallet Ledger Design

These patterns lead to data inconsistencies, reconciliation failures, and compliance risk:

- Treating balances as standalone values. Storing a balance as an editable column in a database, without an underlying event log, means the balance can be updated without any traceable reason. When something goes wrong, there is no history to investigate.

- Weak refund and reversal handling. Implementing refunds by decrementing a balance rather than creating a new ledger entry breaks the audit trail. Every return of funds needs its own posting.

- Mixing runtime balance logic with reporting. The wallet ledger should be optimized for operational speed, not for running complex analytics queries. Mixing these concerns creates both a performance problem and a design problem.

- Poor support for concurrency and idempotency. In high-volume systems, the same payment event can arrive multiple times – from retries, from network errors, from provider callbacks. Without idempotency controls, duplicate entries will corrupt balances.

- Weak reconciliation design. If ledger entries do not carry external reference IDs from payment providers, banks, or settlement partners, reconciliation becomes slower, more manual, and harder to scale.

How SDK.finance Supports Wallet Ledger Use Cases

SDK.finance provides the technical foundation for companies building payment and banking products. The platform’s ledger capabilities cover the core requirements of wallet-based products:

- Multi-currency accounts with support for fiat, crypto, virtual, and bonus currencies

- Balance integrity through transactional processing of all account operations

- PSP flows including top-ups, payouts, fee collection, and provider-level reconciliation

- Sub-account structures through configurable contracts and account types

- Reconciliation-ready records with complete transaction histories and external reference tracking

- Webhook-based event architecture that allows external systems to react to ledger events in real time

The platform is available as SaaS for teams that want to start quickly, and as Source Code for organizations that need technical ownership and full control over their financial infrastructure.

Conclusion

A wallet ledger is the operational foundation for any product that holds, moves, or accounts for user money. It is what makes a digital wallet’s balance trustworthy, a PSP’s merchant payouts auditable, and a neobank’s transaction history defensible in a compliance review. Whether the product is a payment app, an embedded wallet, or a full neobank, the wallet ledger is the layer that makes it work with integrity.

Building on a solid ledger – one that handles real-time balances, double-entry logic, reconciliation, and sub-account hierarchies correctly – is what separates products that scale from products that break.

Build Wallet Products on a Reliable Ledger Foundation

If you are launching a wallet, PSP, or payment application, the ledger layer should not be an afterthought. It is the foundation of balance integrity, transaction traceability, and reconciliation at scale.