When people talk about ledgers in FinTech, the conversation often collapses into a single question: “Which system holds the financial records?” But product ledger and general ledger are not two names for the same thing.

They serve different purposes, operate at different layers, and failing to distinguish between them is one of the most common architectural mistakes in financial product development.

Both systems work with financial records. Both involve debits and credits. But the similarities end there.

- A product ledger (transaction ledger) is built for real-time money movement – it tracks balances, posts transactions, processes refunds, and keeps an operational audit trail.

- A general ledger is built for accounting – it organizes financial data into a chart of accounts, supports month-end close, and produces the financial statements that auditors, regulators, and finance teams rely on.

Modern FinTech products often need both. But they need them for different reasons, at different times, and with different requirements. Understanding the distinction is not just a matter of terminology – it shapes how you architect systems, where you build controls, and how you scale.

The Short Answer

A product ledger is the operational layer for money movement. It records every transaction, maintains account balances in real time, and tracks the lifecycle of funds as they move through a product.

A general ledger is the accounting and reporting layer. It structures financial data into a chart of accounts, supports journal-based workflows, and feeds the financial statements used for compliance, audit, and institutional reporting.

One does not replace the other. A product ledger tells you what is happening with money right now. A general ledger tells you how the books are structured for reporting purposes. In a well-designed FinTech architecture, the two work together – with the product ledger feeding aggregated outputs into the general ledger, rather than competing with it.

Product Ledger vs General Ledger: A Quick Comparison

| Product/Transaction Ledger | General Ledger | |

|---|---|---|

| Primary purpose | Real-time money movement | Accounting and financial reporting |

| Operates at | Transaction time | Reporting period level |

| Updates | In real time, per event | Batch / period-end |

| Tracks | Customer balances, transaction history | Company-level financial position |

| Used by | Product, engineering, ops teams | Finance, accounting, audit teams |

| Key outputs | Balances, audit trail, reconciliation data | Financial statements, journal entries |

| Handles | Wallets, PSP settlement, fees, refunds | Chart of accounts, close process, compliance |

| Replaces the other? | No | No |

What Is a Product Ledger?

A product ledger - sometimes called a transaction ledger or operational ledger - is the system that records the movement of value between accounts in real time. Every top-up, transfer, fee, refund, reversal, and settlement generates a posting in the product ledger. That posting is the source of truth for what happened, when it happened, and how it affected balances.

In practice, a product ledger captures the following:

- Transaction postings – the individual entries that record each financial event

- Debits and credits – typically following double-entry logic, where every transaction has offsetting entries

- Account balances – the current state of each wallet, sub-account, or customer position

- Fees and settlements – amounts charged or paid out as part of operation flows

- Refunds and reversals – corrections and cancellations that need to preserve audit integrity

The term “product ledger” is used because the system is purpose-built for a specific financial product – a wallet, a payment platform, a neobank – rather than being a generic accounting system. Its primary concern is operational correctness: making sure balances are accurate, transactions are consistent, and the audit trail is complete.

Why Product Ledgers Matter in FinTech

In FinTech, the product ledger is the foundation of trust. Customers expect their wallet balance to reflect the truth. PSPs need settlement figures to reconcile with bank reports. Embedded finance providers need sub-account balances to be accurate across hundreds or thousands of counterparties.

The product ledger supports this by delivering:

- Real-time balances. Unlike accounting systems that batch-process at the end of a period, a product ledger updates balances at the moment a transaction is posted. This is essential for authorization decisions, overdraft prevention, and instant payment confirmation.

- Balance integrity. Double-entry logic means every posting must balance. If a credit appears in one account, a corresponding debit appears in another. This prevents value from appearing or disappearing without a corresponding record.

- Auditability. Because entries are immutable, the full history of any account balance can be reconstructed from the ledger. This supports dispute resolution, regulatory inquiries, and internal investigations.

- Reconciliation readiness. A well-structured product ledger generates the data needed to reconcile against external reports – bank statements, payment rail summaries, provider settlement files. Without this, reconciliation becomes a manual forensics exercise.

What Is a General Ledger?

A general ledger (GL) is the accounting system that organizes a company's financial data into a structured chart of accounts. Where a product ledger is focused on operational transaction flows, a general ledger is focused on institutional financial position - what the company owns, owes, earns, and spends, structured for reporting, compliance, and financial governance.

The GL is the foundation of accounting, not payments. It organizes data into account types – assets, liabilities, equity, revenue, expenses – and supports journal entries, period-end close, and financial statement production. Finance teams work in the GL; external auditors review it; tax and regulatory filings depend on it.

What the GL is not designed for is real-time operational balance management. It receives structured inputs from the product ledger – typically as aggregated accounting feeds – and organizes them for institutional purposes.

Product Ledger vs General Ledger: The Main Difference

The most important distinction is not just terminology – it is about scope, latency, ownership, and business function.

Real-Time Operations vs Accounting Reporting

A product ledger operates at transaction time. When a customer initiates a transfer, the ledger posts the entries immediately, updates balances, and makes the result available to dependent systems – authorization engines, notification services, reconciliation pipelines – in real time or near real time.

A general ledger operates at the accounting and reporting level. It is typically updated in batches:

- daily aggregations,

- period-end journals,

- or scheduled accounting feeds.

It is not designed to handle thousands of individual transaction postings per second.

Balance State vs Financial Structure

A product ledger holds the operational truth about balances. At any moment, it can answer: what is the current balance of this account? What transactions contributed to that balance? What is pending versus posted?

A general ledger holds the accounting structure. It answers: how are the company’s assets, liabilities, revenues, and expenses organized? What is the company’s financial position for this reporting period?

These are different questions that serve different stakeholders. Product and operations teams work with the product ledger. Finance teams and auditors work with the general ledger.

Customer Money Movement vs Institutional Books

A product ledger tracks customer-level value movement. Every entry corresponds to a real event – a payment received, a fee charged, a refund issued – that affects a specific customer account.

A general ledger tracks company-level accounting visibility. In a wallet product, for example, the product ledger holds the balance of each individual wallet. The general ledger holds the aggregate liability position – how much the company owes to all wallet holders combined – as a single accounting entry.

When a Product Ledger Is the Better Fit

Wallets and Stored-Value Products

For any product that holds stored value on behalf of users – whether that is a consumer wallet, a corporate account, or a loyalty balance – the product ledger is the operational core. It records top-ups, wallet-to-wallet transfers, refunds, redemptions, and expiry events, and maintains the live balance state that drives every user-facing interaction.

PSPs and Payment Processors

Payment service providers need to track settlement balances for multiple merchants, fees collected across different operation types, and net positions across payment rails. A product ledger provides per-merchant balance structures, captures fee entries separately, and produces the reconciliation data needed to match against card scheme settlement files and bank reports.

Embedded Finance and Marketplace Payouts

Platforms that distribute money to many parties – freelancer marketplaces, e-commerce platforms with seller accounts, SaaS products with revenue-sharing features – need sub-account structures that can hold balances, execute payouts, and maintain audit trails per counterparty. The product ledger supports multi-party flows where a single incoming payment may fan out to multiple recipient accounts, with appropriate fee entries and balance visibility at each level.

When a General Ledger Is the Better Fit

Financial Reporting and Compliance

The GL is the right tool when the need is to produce financial statements for external reporting purposes – balance sheets, income statements, cash flow statements. This includes regulatory capital calculations, tax filings, investor reporting, and audit packages. These use cases require structured, period-based financial data organized into accounting categories, not real-time transaction processing.

Enterprise Accounting Workflows

Month-end close processes, journal reviews, variance analysis, and reporting packages are all GL-native workflows. Accruals for unearned revenue, recognition adjustments, and intercompany eliminations belong in the GL, not in the operational transaction ledger.

Why Many FinTech Products Need Both

This is where many product and engineering teams underestimate the architecture. The assumption is often: “If we have a product ledger, we can generate reports from it. Do we really need a separate GL?” For most regulated FinTech companies, the answer is yes – because the two systems serve genuinely different purposes.

How the Layers Work Together

The product ledger captures operational truth. It records every transaction with full detail – amounts, timestamps, account references, fee entries, status transitions. This level of granularity is essential for operations, but it is not what accounting and reporting systems consume.

The general ledger structures that truth for accounting and reporting. It receives aggregated outputs from the product ledger – typically daily summaries or event-driven accounting feeds – and organizes them into the chart of accounts that finance teams use.

In practice:

- The product ledger is the source of truth for customer balances and transaction history

- The GL is the source of truth for the company’s financial position

- The two are linked by an accounting integration that translates operational events into accounting entries

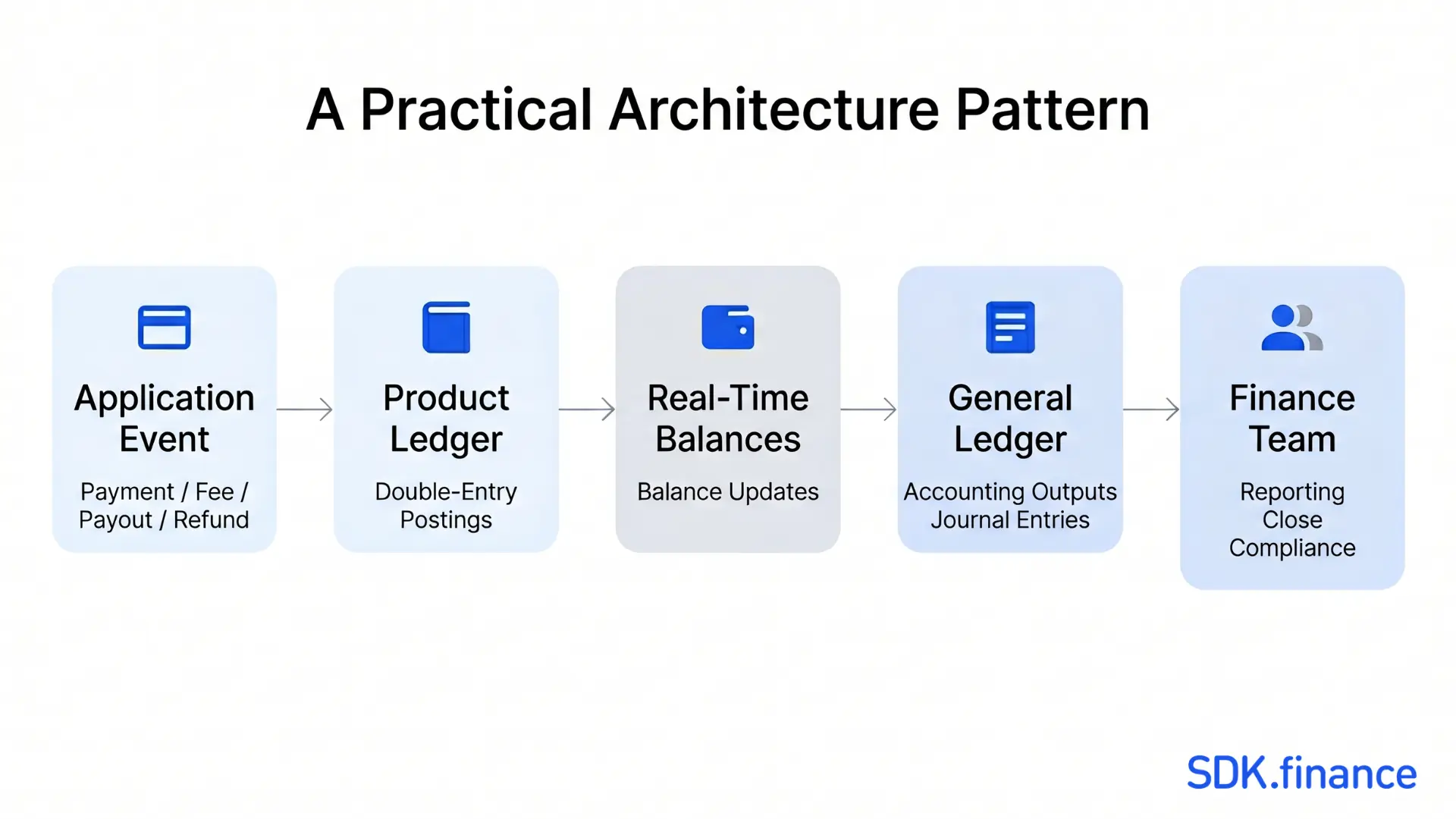

A Practical Architecture Pattern

In a well-designed FinTech stack, the flow typically looks like this:

- A financial event occurs in the application – a payment, a fee, a payout, a refund

- The event is recorded as postings in the product ledger, with double-entry integrity

- Balance projections are updated in real time

- Accounting outputs – journal entries summarizing the operational activity – are generated and fed into the general ledger

- The finance team works in the GL for reporting, close processes, and compliance

This layered model means each system does what it is best at. The product ledger handles volume, speed, and granularity. The general ledger handles structure, reporting, and accounting governance.

Common Misconceptions

A General Ledger Is Not Enough for Real-Time Balances

A GL is designed for periodic accounting, not for real-time balance management. It does not hold per-customer positions with transaction-level granularity, does not support the volume of individual postings a high-throughput payment product generates, and does not provide the pending/posted state model that authorization and settlement flows require. Attempting to use a GL as the operational backbone for a wallet or payment product creates serious risks: balance inconsistencies, reconciliation failures, and an inability to scale.

A Product Ledger Does Not Replace Accounting

A product ledger records operational transactions with the detail necessary for product operations, but it does not organize that data into the accounting categories that regulatory reporting, tax filings, or investor statements require. Treating the product ledger as the company’s books – rather than as the feed into those books – leads to reporting gaps and compliance exposure.

They Are Not Just Two Names for the Same Thing

The term “ledger” is used generically in ways that obscure important distinctions. A product ledger and a general ledger have different designs, different performance requirements, and different business functions. The distinction is not cosmetic – it reflects where operational truth lives versus where accounting structure lives.

Where ERP Fits

ERP systems often contain a GL module, which creates some confusion. An ERP integrates finance, HR, procurement, and operations into a single platform – and its finance module may well be where the general ledger lives for a given company.

But an ERP does not replace a product ledger. ERP systems are not built for real-time, high-volume transaction processing at the customer account level and do not maintain per-customer balance state with the granularity or speed that payment products require. The product ledger handles runtime money movement; the GL – whether inside an ERP or a standalone accounting system – handles institutional financial reporting.

How SDK.finance Fits

SDK.finance is a FinTech platform built for companies launching or scaling payment and banking products – wallets, PSPs, neobanks, embedded finance, and more. At its core is a real-time product ledger: a double-entry accounting engine that records transactions, maintains account balances, tracks fees across multiple currencies, and generates reconciliation-ready data.

For Operational Money Movement

For teams that need the product ledger layer in place before institutional reporting becomes the primary concern, SDK.finance provides:

- Real-time transaction processing and balance maintenance

- Double-entry posting logic with fee separation

- Multi-currency account structures

- Wallet-to-wallet transfers, top-ups, and payouts

- Reconciliation-ready data for external settlement matching

- Provider and contract-level fee configuration

For Broader FinTech Architecture

The platform is designed to fit within a larger FinTech stack. Its API-first design means that accounting outputs from the product ledger can be routed to downstream GL or ERP systems as part of a complete architecture. For teams evaluating how product ledger infrastructure relates to the broader core banking picture, Ledger vs Core Banking System: What’s the Difference? provides useful context.

Conclusion

Product ledger and general ledger are not competing systems – they are complementary layers that solve different problems at different points in a FinTech architecture.

The product ledger is the operational foundation: where money moves, where balances live, where fees are recorded, and where the audit trail begins. The general ledger is the institutional foundation: where financial data becomes structured accounting, where periods close, and where reporting is produced.

For FinTech teams, the distinction is not academic. It determines how systems are designed, where reconciliation is built, what feeds what, and how the architecture scales. Getting it right from the beginning reduces technical debt, simplifies compliance, and makes the product more resilient as it grows.

If you are building or modernizing a financial product and evaluating how to structure the operational ledger layer, SDK.finance’s real-time ledger infrastructure is a practical starting point.