The word “ledger” covers several different product categories in financial infrastructure. A real-time transactional ledger engine, a developer-facing Ledger-as-a-Service API, a payments platform with embedded balance tracking, and a banking subledger for multi-GAAP accounting are not the same product. They solve different problems, serve different buyers, and come with different assumptions about deployment, technical maturity, and regulatory context.

Flattening all of these into one list creates more confusion than clarity. This article compares software relevant to real-time balance management, money movement, and operational ledger infrastructure for banks and FinTechs, with explicit category labels so each vendor is assessed on the right terms. This is not a ranked list by score, but a category-aware comparison of vendors relevant to banks and FinTechs.

At a Glance

The ledger software market for banks and FinTechs spans four distinct product categories:

- transactional ledger engines,

- ledger API / ledger-as-a-service platforms,

- payments infrastructure with embedded ledger,

- banking subledger / accounting hubs.

These are not interchangeable, and the best fit depends on operating model, technical posture, deployment needs, and regulatory context.

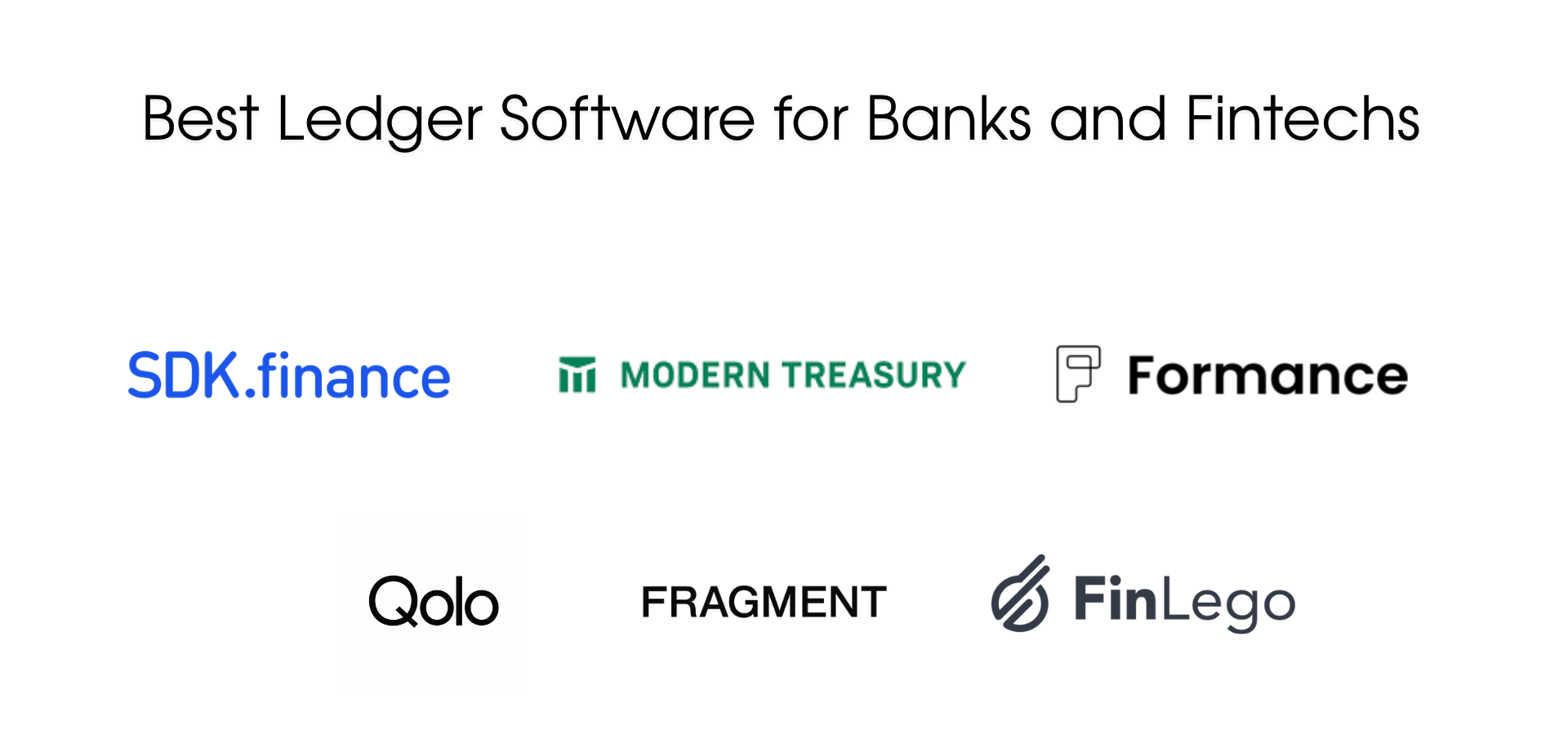

Some vendors, including SDK.finance, Modern Treasury, Formance, Fragment, FinLego, and Qolo, can be compared directly as core operational ledger products. Others, including TigerBeetle, Fiserv, Matera, Nilus, and Wolters Kluwer OneSumX Ledger, are relevant to the market but sit in adjacent categories and need more framing before a safe comparison can be made.

How We Define Ledger Software in This Comparison

| Category | Description |

|---|---|

| Transactional ledger engine | An operational system of record for balances and money movement. It posts transactions in real time, enforces double-entry semantics, and maintains an immutable audit trail. |

| Ledger API / Ledger-as-a-Service | Developer-facing ledger infrastructure exposed through APIs, usually in a managed or cloud-hosted model. The product is the ledger itself, accessed over an API. |

| Payments infrastructure with embedded ledger | A broader payments platform where ledgering is one component of the stack rather than a standalone product. |

| Banking subledger / accounting hub | A bank-grade accounting layer built for instrument-level accounting, multi-GAAP reporting, consolidation, and regulatory finance workflows. |

Out of scope for this article:

- Generic accounting and GL software

- Crypto or hardware wallets

- Full core banking suites evaluated as a whole

- Treasury-only and reconciliation-only tools

For foundational context on ledger categories, see What Is a Ledger in Banking and FinTech and Product Ledger vs General Ledger.

Quick Comparison Table

| Vendor | Category | Best For | Deployment | Pricing Model | Key Watchout |

|---|---|---|---|---|---|

| SDK.finance | Transactional ledger engine | Banks, PSPs, and FinTechs needing either standalone real-time ledger software or a broader ledger-based platform | Standalone SaaS; wider platform and Source Code options | Monthly SaaS subscription plus per-transaction fee; custom license fee for Source Code | Broader than a lightweight ledger API |

| Modern Treasury | Ledger API / LaaS | Developer teams building wallets, FBO/omnibus structures, and payments operations | Fully managed SaaS | Annual terms, usage-based pricing, minimum commitment | Payments-platform orientation, not a bank accounting hub |

| Formance | Ledger API / LaaS | Teams wanting open-source or self-hosted programmable ledger | Open-source self-managed or enterprise deployment | Free open-source core plus enterprise annual subscription | Strong for engineers, less turnkey for finance teams |

| Fragment | Ledger API / LaaS | Developer-heavy startups wanting schema-driven ledgering | Managed hosted platform | Public hosted pricing with usage-based structure | Enterprise deployment posture and some infrastructure claims are less explicit publicly |

| FinLego | Ledger API / LaaS | Wallets, embedded finance, and FinTech teams wanting a modular ledger | Standalone module or integrated platform | Not publicly disclosed; modular commercial model | Weaker fit for finance-team and large-bank accounting use cases |

| Qolo | Payments infrastructure with embedded ledger | Payment programs, virtual accounts, and multi-rail operations | Integrated platform / vendor managed | Not publicly disclosed; enterprise sales-led pricing | Ledger is part of the Qolo stack and is less documented as a standalone product |

Additional relevant vendors, including TigerBeetle, Fiserv, Matera, Nilus, and Wolters Kluwer OneSumX Ledger, are covered below with the category context that affects how they should be evaluated.

Best Ledger Software for Banks and FinTechs

SDK.finance

SDK.finance

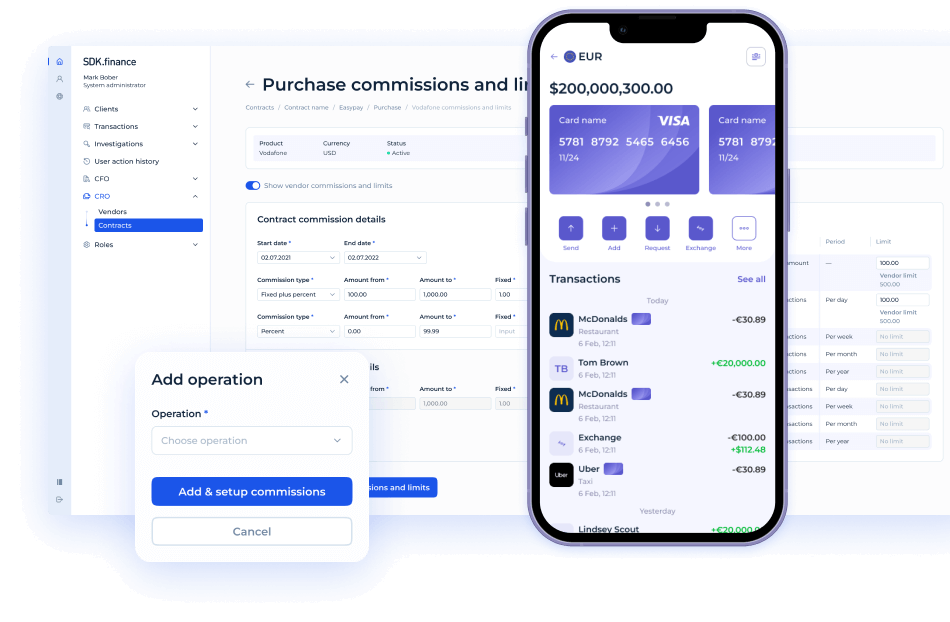

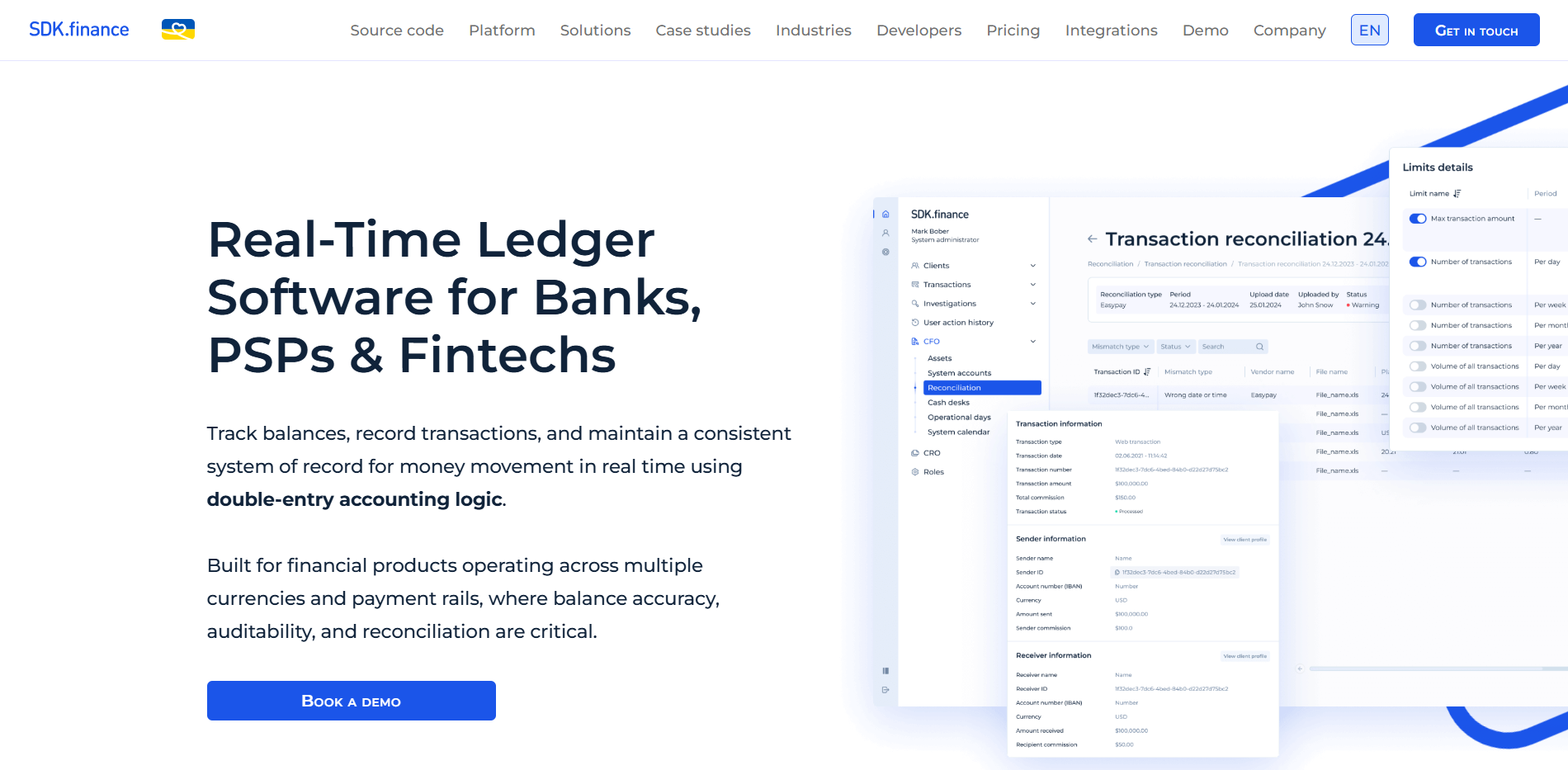

What it is. SDK.finance offers real-time ledger software for banks, PSPs, EMIs, neobanks, wallets, and embedded-finance products. For teams that need more than a standalone ledger, the company also provides a ledger-based FinTech software platform covering payments, accounts, wallets, reconciliation, and related operational flows. In practice, that makes SDK.finance relevant both for buyers looking for a dedicated ledger layer and for those evaluating a fuller payments or banking stack built around that ledger core.

Market context. Founded in 2013, SDK.finance is an EU-based company with presence in Lithuania and the UK. Over more than a decade, it has built a strong position in software for banks, PSPs, and regulated FinTech products, serving clients across the US, Canada, the EU, the UK, and MENA. SDK.finance has also been recognized in recent market research and awards programs, including 2026 studies by Everest Group, Market.us, and Business Research Insights, as well as finalist placements in PayTech Awards and Banking Tech Awards. Typical buyers include banks, EMIs, PSPs, neobanks, and wallet teams that need either standalone ledger software or a broader ledger-based platform.

Best for. Banks, PSPs, and FinTechs that want real-time ledger software with strong support for regulated financial products, multi-currency balance logic, and high-volume transaction processing. It is especially relevant for teams that may start with ledger needs and later expand into a wider payments or FinTech stack.

Why it stands out. SDK.finance combines real-time posting, double-entry accounting, multi-currency balance management, reconciliation, multi-entity subaccounts, crypto support, and support for high-volume transaction processing. The platform also exposes 570+ REST APIs across accounts, payments, wallets, onboarding, compliance, cards, reporting, and integrations. That breadth makes it relevant both as a standalone ledger layer and as the operational core of a broader FinTech platform.

Pricing model. For standalone ledger adoption, SaaS is the most natural commercial model for many buyers. For larger or more specialized implementations, the company also offers broader platform scope and alternative delivery approaches, including Source Code, depending on deployment and control requirements.

Watchouts. SDK.finance is broader than a lightweight ledger API, so it should not be evaluated too narrowly against developer-only LaaS products. Buyers looking for a quick self-serve API trial will find a different scope and buying motion here. On the other hand, teams that want a SaaS-first ledger today with the option to grow into a wider platform later may see that broader scope as a practical advantage.

Modern Treasury

Modern Treasury

What it is. Modern Treasury is a payments infrastructure platform with a dedicated Ledgers product. It exposes real-time double-entry ledgering through a developer API, tightly connected to money movement, payment operations, and FBO/omnibus account management.

Market context. Founded in 2018, Modern Treasury is a US-based company headquartered in San Francisco. Its public positioning is developer-first, but increasingly broader across payments infrastructure. Typical buyers include FinTech product teams, platforms, and payment operators that want programmable money movement and operational visibility without running core ledger infrastructure themselves.

Best for. Developer-led teams building wallets, payments operations, or omnibus/FBO money movement systems. Strong FinTech, PSP, and wallet fit; medium bank fit.

Why it stands out. Modern Treasury has a strong API posture, clear documentation, and a natural fit for programmable money movement workflows. It is especially strong for FinTech, PSP, and wallet use cases.

Pricing model. Modern Treasury publicly describes annual terms, usage-based pricing, and a minimum commitment. Exact commercial terms still depend on payment volume, rails, and account structure.

Watchouts. It is best understood as a payments infrastructure product, not a banking accounting hub. Multi-currency support at the ledger layer is also not especially prominent on the main ledger product page.

Formance

Formance

What it is. Formance is an open-source programmable ledger platform with enterprise options. Its core ledger module uses Numscript, a domain-specific language for encoding transaction logic. The platform extends to reconciliation, payment connectivity, and flow orchestration.

Market context. Founded in 2021, Formance is a France-based company with roots in Paris and a global open-source financial infrastructure posture. Its center of gravity is developer-first and infrastructure-oriented, with strong appeal to engineering teams that want ledger control without building from zero. Its commercial motion follows an open-core pattern: free adoption at the core, enterprise engagement when teams need support, deployment help, or broader platform services.

Best for. Teams wanting open-source or self-hosted programmable ledger with reconciliation and orchestration adjacencies. Strong FinTech, PSP, and wallet fit; medium bank fit.

Why it stands out. Formance offers a permissive open-source core, explicit programmability, real-time posting, double-entry, multi-currency support, and strong appeal for engineering-led teams that want to build on a flexible ledger foundation.

Pricing model. The core ledger is free and self-hostable. Enterprise deployment, support, and broader platform services are sold on an annual subscription and custom quote basis.

Watchouts. Formance is not a turnkey finance-team product. It is strongest when the buyer has technical resources and wants a programmable infrastructure layer rather than a simple managed ledger service.

Fragment

Fragment

What it is. Fragment is a developer-first ledger API with schema-driven ledger design, balance management, reporting primitives, and consistency controls. Teams define their ledger schema, account types, transaction templates, and balance views through a programmable workflow. It is built primarily for FinTechs, brokers, marketplaces, and other product teams dealing with complex money movement.

Market context. Fragment is a US-based infrastructure company with a New York presence and a strongly engineering-led public posture. Its product messaging is aimed at teams that want more flexibility than a pre-opinionated ledger platform offers. The buyer profile is startup and scale-up product teams that want ledger primitives with modern developer ergonomics.

Best for. Developer-heavy startups that want flexible schema-driven ledgering and reporting primitives. Strong FinTech and wallet fit; medium PSP fit; weak bank fit.

Why it stands out. Fragment gives teams precise control over account structures, transaction templates, balance views, and ledger behavior. It is especially relevant for FinTech, wallet, marketplace, and broker use cases.

Pricing model. Fragment publishes hosted pricing publicly. The commercial model is usage-based and tied to hosted deployment, though buyers with more specialized requirements still need direct commercial conversations.

Watchouts. Some infrastructure claims, including immutability and enterprise deployment posture, are less explicit publicly than with some peers. It should be positioned as a developer-first ledger platform, not a bank-grade operational core.

FinLego

FinLego

What it is. FinLego is an API-first banking and wallet infrastructure vendor with a Real-Time Ledger Engine product. It is positioned as a modular ledger module for wallet builders, payment providers, card issuers, and embedded-finance teams, available either as a standalone module or within a broader FinLego platform integration.

Market context. Founded in 2020, FinLego is a UK-based company headquartered in London. Its messaging is global and modular, appealing to FinTechs, neobanks, wallet teams, and embedded-finance operators that want pre-built infrastructure components rather than a ground-up ledger build. The buyer profile leans toward product teams looking for flexibility without taking on full ledger engineering in-house.

Best for. Wallets, P2P, embedded finance, and FinTech teams wanting a modular, API-integrated ledger without a custom build. Strong PSP and wallet fit; medium bank fit.

Why it stands out. FinLego has a clear modular story, good fit for wallet and card use cases, and strong messaging around subaccounts, auditability, and real-time balance logic. It is especially relevant when the buyer wants a ledger component rather than a full banking stack.

Pricing model. FinLego does not publish a standard price card for its ledger product. The commercial model appears modular and custom, depending on which components are adopted.

Watchouts. It is more FinTech- and product-oriented than finance-hub oriented. It is not the natural first choice for large incumbent-bank accounting transformation.

Qolo

Qolo

What it is. Qolo is a payments infrastructure platform with an embedded Quantum Ledger product. It serves payment programs, virtual card operations, multi-rail orchestration, and commercial payment platforms. The ledger provides real-time balance tracking, double-entry accounting, and reconciliation inside Qolo’s unified payments stack.

Market context. Founded in 2018, Qolo is a US-based company focused primarily on North American payment programs and financial institutions. Its buyer profile includes banks, FinTechs, vertical SaaS companies, and commercial payment operators that want a unified stack for payment programs and virtual-account management. The go-to-market leans enterprise and program-oriented rather than startup self-serve.

Best for. Payment programs, virtual accounts, and multi-rail operations that need a unified operational ledger alongside payment processing. Strong bank, FinTech, and PSP fit; medium wallet fit.

Why it stands out. Qolo is strongest where the ledger is only one part of a broader payments operating environment. Its fit is especially strong for program management, virtual accounts, and multi-rail payment operations.

Pricing model. Pricing is not publicly disclosed. The commercial model appears enterprise and sales-led, with pricing likely shaped by broader platform scope rather than a standalone ledger fee.

Watchouts. Qolo should be evaluated as a broader payments platform with embedded ledgering, not as a neutral standalone ledger engine.

Relevant Vendors in Adjacent Categories

These vendors are relevant to buyers scanning the broader ledger landscape, but they should not be treated as direct equivalents to the core group above.

TigerBeetle (Transactional ledger engine, database layer)

TigerBeetle (Transactional ledger engine, database layer)

TigerBeetle is an open-source financial transactions database built for high-throughput double-entry workloads. It is relevant for teams that want to build ledger infrastructure at the database layer rather than buy a turnkey ledger platform.

That is the key distinction: TigerBeetle gives engineering teams a specialized foundation, not a finished operational ledger product. Multi-currency, multi-entity, and product-level logic are implemented by the buyer.

Fiserv FinTech Ledger (Banking infrastructure vendor)

Fiserv FinTech Ledger (Banking infrastructure vendor)

Fiserv is a US-based financial technology company founded in 1984. Its FinTech Ledger belongs in a broader banking infrastructure conversation shaped by sponsor-bank programs, institutional distribution, and enterprise bank-tech relationships.

It is relevant for large institutions and FinTech-bank partnerships, but it is not the same kind of product evaluation as a developer-led ledger API or a standalone FinTech ledger engine. Procurement is enterprise-led, and public product detail is more limited.

Matera Digital Twin (Core modernization platform)

Matera Digital Twin (Core modernization platform)

Founded in 1987, Matera is a Brazil-based banking technology company with strong roots in Latin America and growing North American presence. Its Digital Twin is designed as a real-time transaction layer for banks that want modern payments and always-on balance updates without replacing the core banking system.

This makes Matera highly relevant in bank modernization programs, especially where instant payments, core augmentation, and real-time operational balance visibility matter. It is not a natural fit for PSPs, wallet builders, or developer-first teams comparing standalone ledger APIs.

Nilus Unified Ledger (Finance operations platform with customer ledger layer)

Nilus Unified Ledger (Finance operations platform with customer ledger layer)

Nilus is positioned as a finance operations platform that connects customer-level ledger visibility with ERP synchronization, reconciliation, and close-process workflows. Its public messaging leans more toward finance control and operational visibility than toward developer-first ledger infrastructure.

That makes Nilus relevant for FinTechs, marketplaces, and finance operations teams that need customer balance visibility alongside accounting workflows. It is less clearly a bank-core ledger platform and less clearly a programmable ledger primitive in the way API-led vendors are.

Wolters Kluwer OneSumX Ledger (Banking subledger / accounting hub)

Wolters Kluwer OneSumX Ledger (Banking subledger / accounting hub)

Founded in 1836, Wolters Kluwer is a Netherlands-based global software and information-services company. OneSumX Ledger is a banking subledger and accounting hub built for instrument-level accounting, multi-GAAP consolidation, and regulatory-grade finance processes.

This is a different buyer conversation from operational ledger software. It is designed for bank finance, risk, and regulatory reporting teams rather than for developers building wallets, PSP infrastructure, or real-time money movement systems.

Which Ledger Model Fits Your Business Best

For banks and regulated financial institutions

Banks typically need either a transactional ledger engine for real-time operational balance management or a banking subledger/accounting hub for instrument-level finance and regulatory reporting. Those are different products for different functions, and some institutions may need both.

For operational ledger infrastructure, SDK.finance and Qolo are strong candidates. For core modernization without full replacement, Matera Digital Twin is more relevant. For regulatory-grade subledger and multi-GAAP accounting, Wolters Kluwer OneSumX Ledger belongs in the evaluation. Fiserv is relevant where a broader enterprise banking technology relationship is part of the decision.

For PSPs and payment programs

PSPs and payment programs need real-time balance accuracy, multi-entity subaccounts, reconciliation, and usually multi-rail support. SDK.finance, Modern Treasury, FinLego, and Qolo all have strong fit here. Fragment and Formance can also work well for developer-first teams that want more control over ledger design and implementation.

For wallets and embedded-finance products

Wallet and embedded-finance builders usually care about real-time posting, subaccount logic, and API-first integration. Modern Treasury, Formance, Fragment, and FinLego are all strong in this segment. SDK.finance also fits well where the ledger needs to support a broader product stack around wallets and payments.

For wallet-specific ledger architecture, see What Is a Wallet Ledger and Wallet Ledger Software.

For developer-led teams building programmable money movement

Developer-first teams that want maximum control over ledger schema and transaction logic should look closely at SDK.finance, Formance, Fragment, and Modern Treasury. TigerBeetle is the lowest-level option for teams willing to build the surrounding infrastructure themselves.

For finance-heavy accounting and subledger environments

When the primary requirement is multi-GAAP instrument accounting, GL consolidation, and regulatory reporting rather than real-time product ledgering, banking subledger and accounting-hub products are the right category. Wolters Kluwer OneSumX Ledger is the clearest example here. Nilus is more relevant where customer-ledger visibility needs to connect with finance operations and ERP workflows.

For background on the distinction between product ledgers and general ledgers, see Product Ledger vs General Ledger and What Is a General Ledger.

What to Watch Out for When Comparing Ledger Vendors

Not every ledger is a real-time operational ledger. Some products position as ledgers but are really accounting or reporting systems with batch or end-of-day logic.

Not every ledger API is bank-grade. Developer-first LaaS products can be excellent for FinTech and wallet use cases without meeting the deployment, audit, or regulatory expectations of licensed banks.

Some products are embedded inside broader payment stacks. In those cases, the value proposition is the combined platform, not a standalone ledger layer.

Some products are accounting hubs, not runtime ledgers. Comparing those directly to operational ledger engines without category labels leads to misleading conclusions.

Open-source engines are not the same as turnkey ledger software. TigerBeetle and open-source Formance give teams strong building blocks, but they assume more engineering ownership.

Banking infrastructure and core modernization vendors follow different procurement models. Fiserv and Matera involve enterprise engagement models, longer sales cycles, and broader institutional context than API-led vendors.

Pricing opacity is common across this market. Even where pricing posture is public, exact commercial terms often depend on deployment mode, support scope, payment rails, or usage volume.

Payment Reconciliation: Core Fintech Infrastructure.

How SDK.finance Fits Into This Landscape

SDK.finance fits the transactional ledger engine category, but it is better understood as more than a narrow ledger API alternative. It offers real-time ledger software for banks, PSPs, EMIs, neobanks, wallets, and embedded-finance products, while also providing a broader ledger-based fintech platform for teams that want more than a standalone ledger layer.

Its core capabilities include real-time posting, double-entry accounting, multi-currency support, reconciliation, multi-entity subaccounts, crypto support, high-volume transaction processing, and 570+ REST APIs across accounts, payments, cards, compliance, onboarding, wallets, reporting, and integrations.

That makes SDK.finance especially relevant for organizations that want standalone SaaS ledger software today, but may later need a broader platform around that ledger core.

Choosing the Right Ledger Model

The ledger software market for banks and fintechs is fragmented across meaningfully different product categories. Transactional ledger engines, API-led Ledger-as-a-Service platforms, embedded payments ledgers, and banking subledger/accounting hubs are not interchangeable. They solve different problems for different buyers operating under different constraints.

Category discipline matters. A developer-first LaaS platform is not the same as a bank-grade subledger system. An open-source database engine is not the same as a turnkey fintech ledger platform. A payments stack with an embedded ledger is not the same as a standalone ledger infrastructure product.

The right approach is to map your requirement to a category first, then compare vendors within that category on the specifics that matter for your operating environment, regulatory context, and technical posture. Commercial model and deployment posture are part of that decision, not afterthoughts.