If you’ve spent time in fintech or banking architecture, you’ve probably heard these two terms used interchangeably. They shouldn’t be. A ledger and a core banking system solve different problems, sit at different layers of your stack, and serve different purposes depending on what kind of financial product you’re building.

This article breaks down exactly what each system does, where they overlap, where they diverge, and how to decide which one your business actually needs.

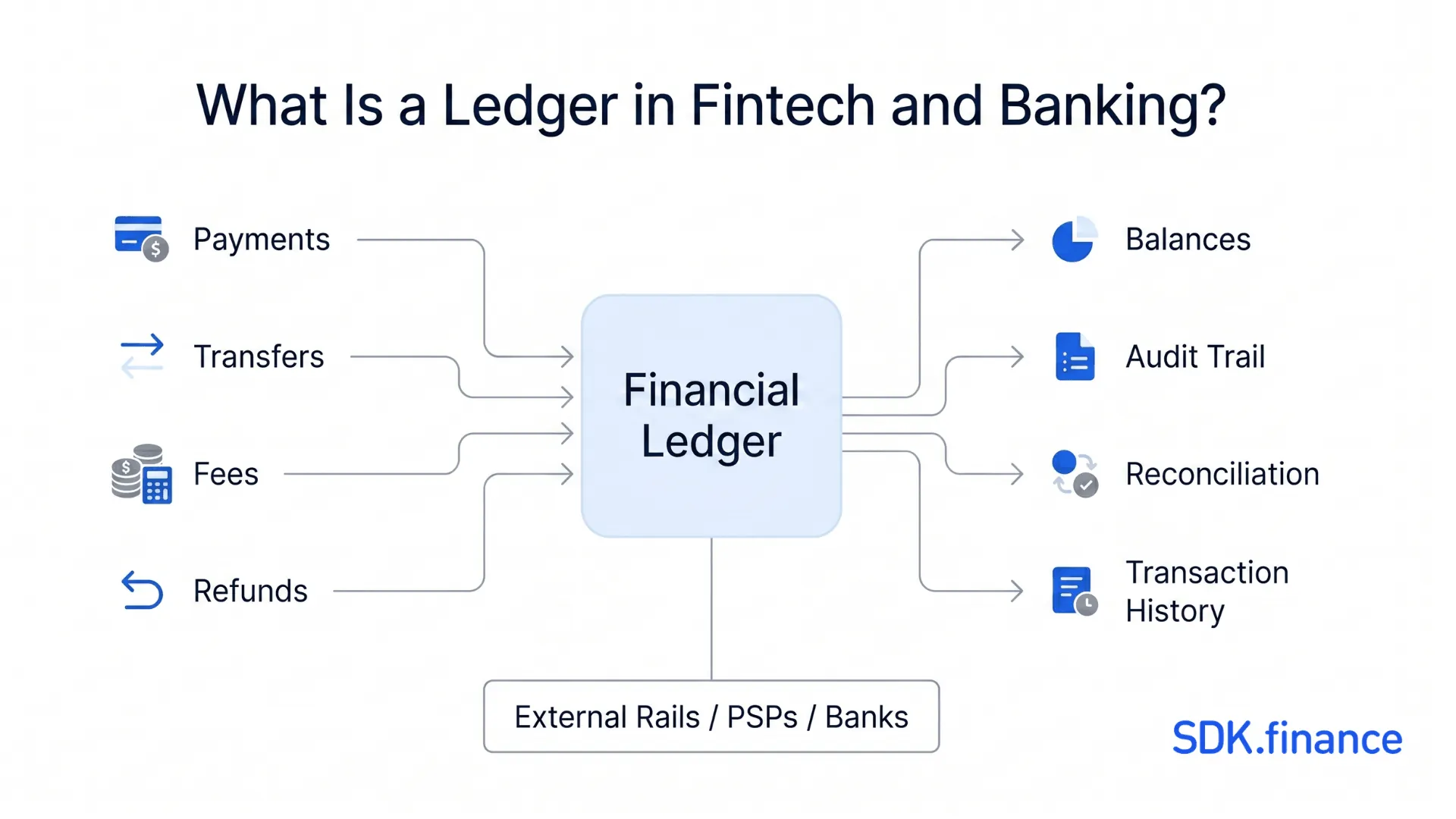

What Is a Ledger in Fintech and Banking?

A ledger is the system of record for money movement. Its job is simple but unforgiving: record every financial event accurately, maintain running balances across accounts, and never lose or corrupt a transaction.

In practice, a financial ledger handles:

- Transaction postings – every debit and credit, recorded as immutable entries

- Balance calculation – real-time or near-real-time visibility into what each account holds

- Double-entry enforcement – every value movement has an equal and opposite entry; money is never created or destroyed within the system

- Reversals and corrections – mistakes are fixed by posting a correcting entry, not by editing history

- Reconciliation readiness – the ledger produces a clean, auditable trail that maps to external rails and account states

Modern ledger infrastructure, sometimes called a real-time ledger or transaction ledger, adds sub-account structures, multi-currency support, metadata tagging, and high-throughput posting capabilities.

The ledger does not manage customer relationships, product rules, or operational workflows. It records what happened to money. That’s its entire mandate – and that narrow focus is what makes it fast and trustworthy.

What Is a Core Banking System?

A core banking system is the broader operational platform that runs a financial institution’s banking products. It handles the full lifecycle of customer accounts, deposits, loans, payments, fees, and interest - everything required to operate as a bank or regulated financial product provider.

A core banking platform typically includes:

- Customer and account management – onboarding, KYC integration, account ownership, product assignment

- Deposit and lending engines – current accounts, savings, term deposits, loans, credit lines

- Fee and interest calculation – configurable product rules, tiered rates, scheduled charges

- Payments connectivity – integration with SWIFT, SEPA, Faster Payments, card schemes, and domestic rails

- Regulatory and compliance tooling – AML screening, reporting, transaction monitoring, data residency controls

- Operational workflows – statement generation, limit management, exception handling, EOM/EOD processing

- Often an integrated or tightly coupled general ledger – the accounting layer that records product-level events

Core banking software is what a licensed bank, neobank, or EMI uses to actually run banking operations. It’s the operating environment — not just a recording system.

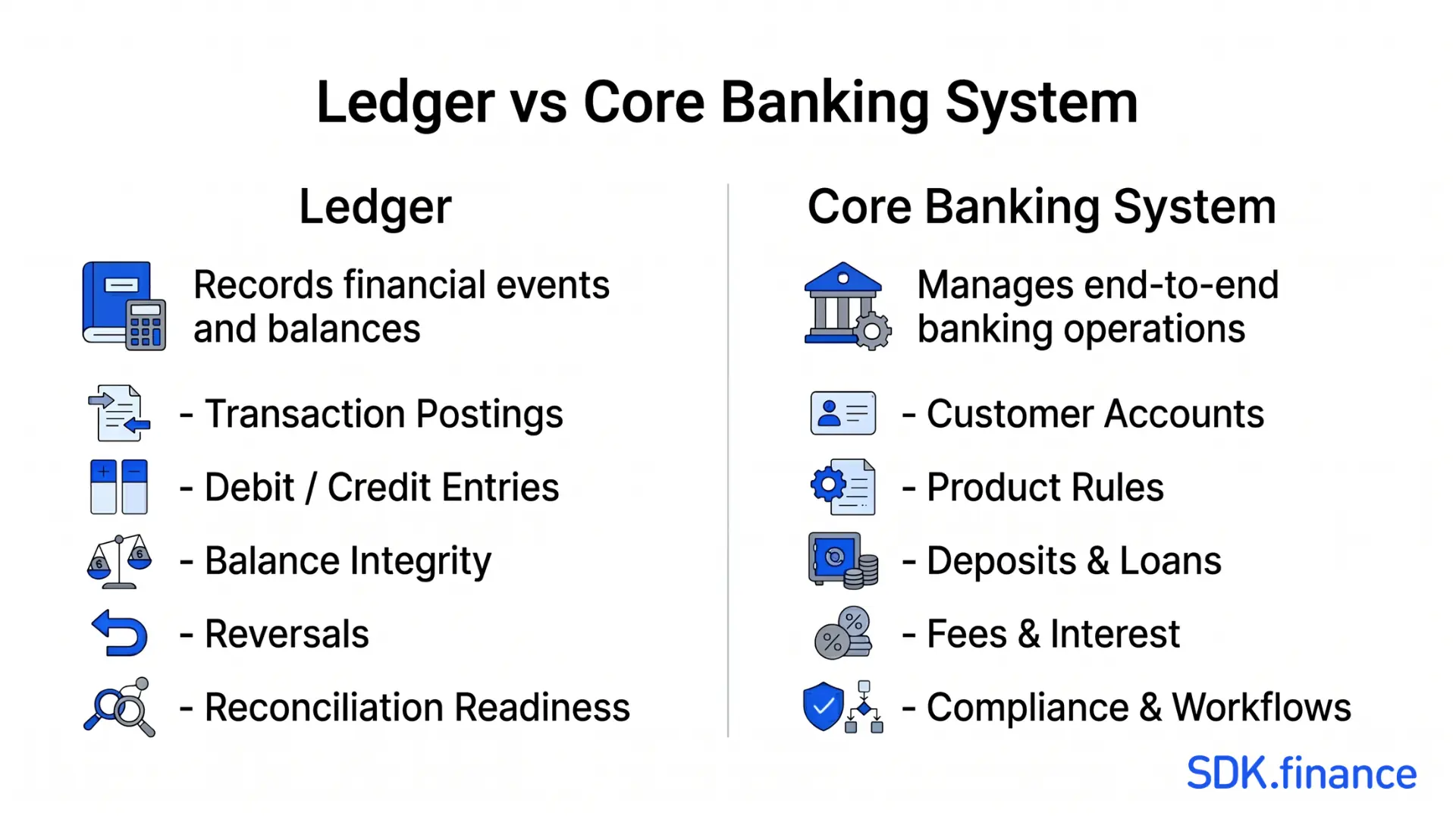

Ledger vs Core Banking System: The Short Answer

A ledger is the foundational financial record layer: it captures debits, credits, and balances with precision. A core banking system is the broader operational platform that may include a ledger but also manages products, customers, fees, compliance, and workflows. The ledger is a component. The core is the system that contains, coordinates, and extends it.

If the ledger is the source of financial truth, the core banking system is the environment in which that truth is created, consumed, and operationalized.

Confusing the two is one of the more common architectural mistakes in fintech. Building a ledger does not give you a core. Running a core does not mean your ledger is correctly isolated.

The Main Difference Between a Ledger and Core Banking

A Ledger Records Financial Events and Balances

Everything a ledger does traces back to one question: what is the current state of each account, and how did it get there? Ledger logic is narrow, deterministic, and unforgiving. It cares about:

- Posting accuracy – every entry is correct, or it isn’t posted

- Balance integrity – balances reflect all posted entries, and only posted entries

- Auditability – every balance change has a causal chain back to a specific posting

- Idempotency – duplicate messages don’t produce duplicate postings

- Immutability – history cannot be edited, only corrected forward

Ledgers also support specific architectural patterns: sub-ledger structures for wallets or escrow, authorization holds and pending states, multi-currency entries, and cross-rail reconciliation exports. These are not general-purpose capabilities – they’re built specifically to support money movement at scale.

A Core Banking System Manages End-to-End Banking Operations

A core banking system operates at a higher level of abstraction. It knows what accounts are, what products customers hold, what rules apply to those products, and what happens when something changes. It’s where:

- A customer opens a savings account and interest begins accruing

- A loan disbursement triggers a repayment schedule

- A fee event fires because an account fell below a minimum balance

- A withdrawal limit prevents a transaction from being authorized

- A statement gets generated and delivered at end of month

The core orchestrates these events. The ledger records what resulted from them. Both are essential – but they’re doing fundamentally different work.

One Is a Component, the Other Is a Broader Platform

The most important architectural point: a ledger is a component that lives inside (or alongside) a core banking system. A core banking system is the platform that contains it.

Some core banking platforms include a fully integrated ledger as one of their modules. Others are designed around API-first, modular architectures and expect you to bring your own ledger or connect to a dedicated ledger service. In modern, cloud-native deployments, the trend is toward explicit separation treat the ledger as a distinct layer with its own service boundary.

How a Ledger Fits Inside a Core Banking Architecture

Ledger as the System of Record

In any well-designed financial architecture, the ledger is the single source of truth for balances and transaction history. Everything else – product engines, risk systems, reporting layers, customer portals – should derive balance state from the ledger, not maintain their own shadow copies.

This is more important than it sounds. When systems maintain their own balance representations outside the ledger, you get reconciliation debt: discrepancies between what the product system believes and what the ledger knows. These discrepancies compound over time, create audit exposure, and are expensive to fix.

Core Banking as the Operating Environment

The core banking system is where product logic lives. When a customer deposits funds, the core determines what product that maps to, what rules apply, how fees are calculated, and what notifications are triggered. It then instructs the ledger to post the resulting financial events.

The core is the orchestrator. The ledger is the recorder. This separation is the basis of sound financial architecture.

Why Modern Architectures Separate the Layers

In legacy monolithic cores, ledger logic was deeply embedded in the product processing layer. That made sense when everything ran in batch at the end of the day. Real-time architectures require a different model.

Separating the ledger from the core gives you:

- Independent scalability – high-frequency posting workloads can scale without affecting product processing

- Testability – ledger correctness can be verified independently of business logic

- Portability – you can swap or upgrade core banking components without touching your financial record layer

- Cross-system consistency – a dedicated ledger can aggregate postings from multiple sources (card processor, payment rails, internal transfers) into a single, canonical balance view

This is the architecture pattern behind modern Ledger-as-a-Service platforms and the reason purpose-built ledger infrastructure has emerged as a distinct product category.

When Fintechs Need a Ledger but Not a Full Core Banking System

Not every fintech needs the full operational weight of a core banking system. Many financial products primarily need one thing: a reliable, real-time view of where money is and how it got there. A dedicated ledger is often the right fit for:

Digital Wallet Providers

Wallet products are fundamentally a ledger problem. Each user has a balance. Transactions move value between balances. The system needs to track states (available, pending, reserved), enforce constraints (no negative balances), and support instant visibility. A well-designed transaction ledger handles this directly – you don’t need a full core banking platform to run a wallet.

Payment Service Providers (PSPs)

PSPs route payments across multiple rails and need to reconcile their internal money state against external clearing. A dedicated ledger provides the sub-account and posting model required to track inflows, outflows, holds, settlements, and reversals across rails – without the product overhead of a full core.

Embedded Finance Products

If you’re embedding financial functionality inside a non-bank platform – marketplace payouts, B2B spend management, creator monetization, or freelancer earnings – the core requirement is accurate fund-state management, not full banking product logic. A ledger sits cleanly as an internal service without pulling in the regulatory and operational complexity of a core banking deployment.

Payout Platforms and Marketplaces

Platforms that manage FBO (For Benefit Of) structures, escrow, or multi-party payouts need precise sub-balance tracking and clear audit trails. Ledger infrastructure purpose-built for this use case is far more appropriate than trying to bend a core banking system to serve a non-banking product model.

When a Business Needs a Full Core Banking System

If the product you’re building involves regulated banking operations at scale, you need a core banking system. The signal is usually product breadth: you’re not just tracking balances, you’re managing customer relationships, running interest calculations, issuing statements, and operating under banking licenses. This typically applies to:

Neobanks and Digital Banks

A neobank offering current accounts, savings products, and debit cards is operating a regulated bank. That requires a full product engine, customer lifecycle management, fee and interest processing, and the compliance infrastructure that comes with a core banking deployment.

Licensed Banks and Credit Unions

Traditional and digital-first licensed institutions need the full operational capability of a core banking platform: deposit servicing, lending, payments integration, statement production, regulatory reporting, and the ability to manage complex product portfolios across customer segments.

EMIs and Financial Institutions with Full Product Logic

Electronic Money Institutions offering complex product stacks — multiple account types, credit products, spend controls, multi-currency operations – need the configurable product engine and operating depth that a core banking system provides. A ledger alone is not sufficient.

Can a Fintech Use Both?

Yes – and increasingly, this is the normal architecture for sophisticated financial products.

The hybrid model separates concerns cleanly: the core banking system manages the regulated product layer (account servicing, customer relationships, compliance, product rules), while a dedicated ledger handles high-frequency money state tracking, sub-balance logic, cross-rail reconciliation, and real-time balance visibility.

This pattern is particularly common in:

- Sponsor-bank ecosystems – the sponsor bank runs core banking for regulated operations; the fintech runs its own ledger for product-level state

- Embedded finance platforms – a core handles the banking wrapper while a ledger tracks wallet or sub-account activity

- Digital bank modernization – the legacy core remains the legal account processor while a new ledger layer handles real-time postings and reconciliation for digital products

- Neobanks with complex money movement – the core manages products; a purpose-built ledger handles authorization holds, reversals, and cross-currency posting at speed

The key design rule: define clearly which system owns each domain. The ledger owns posting truth. The core owns product state. Reconciliation runs between them. As long as those boundaries are enforced, the hybrid model is clean and scalable.

Common Misconceptions

A Ledger Is Not the Same as Accounting Software

Finance teams use accounting or ERP software – QuickBooks, NetSuite, SAP – to manage institutional accounts, P&L, and external reporting. A financial ledger in the product architecture sense is not this. It’s an operational system that records real-time transaction events and maintains live customer or product balances. The two interact – the product ledger feeds the general ledger – but they’re built for different purposes and operate at different cadences.

Core Banking Is Not Just a Ledger

Some teams assume that because a core banking system tracks balances, it’s doing ledger work. This conflates output with mechanism. A core banking system produces balance-related outputs, but its internal accounting model may not offer the posting integrity, immutability, or real-time auditability of a purpose-built ledger. When you need strong posting guarantees – at scale, in real time, across rails – a dedicated ledger is the right tool, not the accounting layer of a product system.

Real-Time Balances Alone Do Not Equal Core Banking

A real-time ledger that gives you instant balance visibility is not a core banking system. It doesn’t manage product rules. It doesn’t calculate interest. It doesn’t produce regulated statements. It doesn’t handle customer onboarding workflows. Real-time balances are necessary for modern financial products – they’re not sufficient for operating a bank.

Ledger vs Core Banking: Side-by-Side Comparison

| Dimension | Ledger | Core Banking System |

| Primary purpose | Record financial events and maintain balance integrity | Operate banking products and customer accounts |

| Scope | Narrow and precise: postings, balances, audit trail | Broad: products, fees, interest, compliance, workflows |

| Transaction model | Double-entry, immutable, idempotent | Product-driven events, configurable business logic |

| Balance visibility | Real-time, posting-accurate | Derived from product and posting layer |

| Compliance role | Audit trail and reconciliation readiness | Full regulatory product servicing and reporting |

| Typical users | Fintechs, wallets, PSPs, embedded finance, marketplaces | Banks, neobanks, EMIs, licensed lenders |

| Can operate standalone? | Yes, for wallet/sub-balance use cases | Usually yes, but ledger depth and real-time posting capabilities vary by platform |

| Best combined? | Yes – ledger for precision, core for product breadth | Yes – delegate posting truth to dedicated ledger |

How SDK.finance Supports Both Ledger and Core Banking Use Cases

SDK.finance is built to serve both ends of this architecture spectrum – whether you need precise real-time ledger infrastructure, a full core banking operating layer, or a combination of both.

SDK.finance Ledger

The SDK.finance Ledger is designed for transaction integrity and real-time balance visibility. It provides a dedicated posting engine with double-entry enforcement, sub-account structures, multi-currency support, and reconciliation-ready audit trails. If your core requirement is knowing exactly where the money is – across wallets, payouts, escrow, or internal accounts – the ledger layer handles this as a precise, independent service.

This is the right starting point for wallet products, PSP infrastructure, marketplace FBO models, and embedded finance platforms that need strong posting guarantees without full core banking overhead.

SDK.finance Core Banking Software

The SDK.finance Core Banking platform covers the full operational layer:

- account and customer management,

- deposit and lending products,

- fee and interest engines,

- payments connectivity, and compliance tooling.

This is built for institutions and fintech products that need the complete banking operating environment – not just a balance engine.

The platform is API-first and modular, which means the ledger and core layers are architecturally distinct and can be deployed together or independently depending on your product needs.

Conclusion

The difference between a ledger and a core banking system is not a matter of scale – it’s a matter of scope and function:

- A ledger is a precision instrument: it records financial events, maintains balances, and provides the audit trail your entire stack depends on.

- A core banking system is the operating environment: it manages the products, customers, rules, and workflows that make banking work.

Getting this distinction right has real architectural consequences. Building a ledger when you need a core leaves you without the product logic to operate at scale. Assuming your core is doing ledger work when it isn’t leaves you with reconciliation debt and audit exposure.

For most sophisticated financial products – and increasingly for neobanks, embedded finance platforms, and sponsor-bank ecosystems — the right answer is a clear separation of both layers with explicit ownership over each domain.

SDK.finance provides both: a dedicated Real-Time Ledger for transaction integrity and balance precision, and a Core Banking Software platform for full banking product operations. Whether you need one, the other, or both, the architecture is designed to let you deploy cleanly at each layer.