In the last decade, payments have quietly become one of the most strategic layers of the digital economy. Companies across sectors now treat payments not as a supporting function, but as a growth engine and a competitive advantage. It’s no coincidence that global names like Revolut, Coinbase, Shopify, Airbnb, Bolt, and Uber have invested heavily in their own payment infrastructure.

By doing so, they’ve gained the ability to shape customer experience, reduce fees, support global payments, and support new business models that off-the-shelf PSPs simply weren’t designed for.

What used to be an engineering challenge reserved for banks is now far more accessible. Open APIs, cloud platforms, and ready-made financial cores have dramatically lowered the barrier to entry. As a result, fintechs, digital exchanges, marketplaces, and even traditional enterprises are taking deeper control of how money moves through their systems.

This guide walks through the building blocks behind payment systems, the reasons companies create their own, and the practical decisions that shape a long-term payment strategy – including where white-label PSP platforms fit into the picture.

What Is a Payment System and How Does It Work?

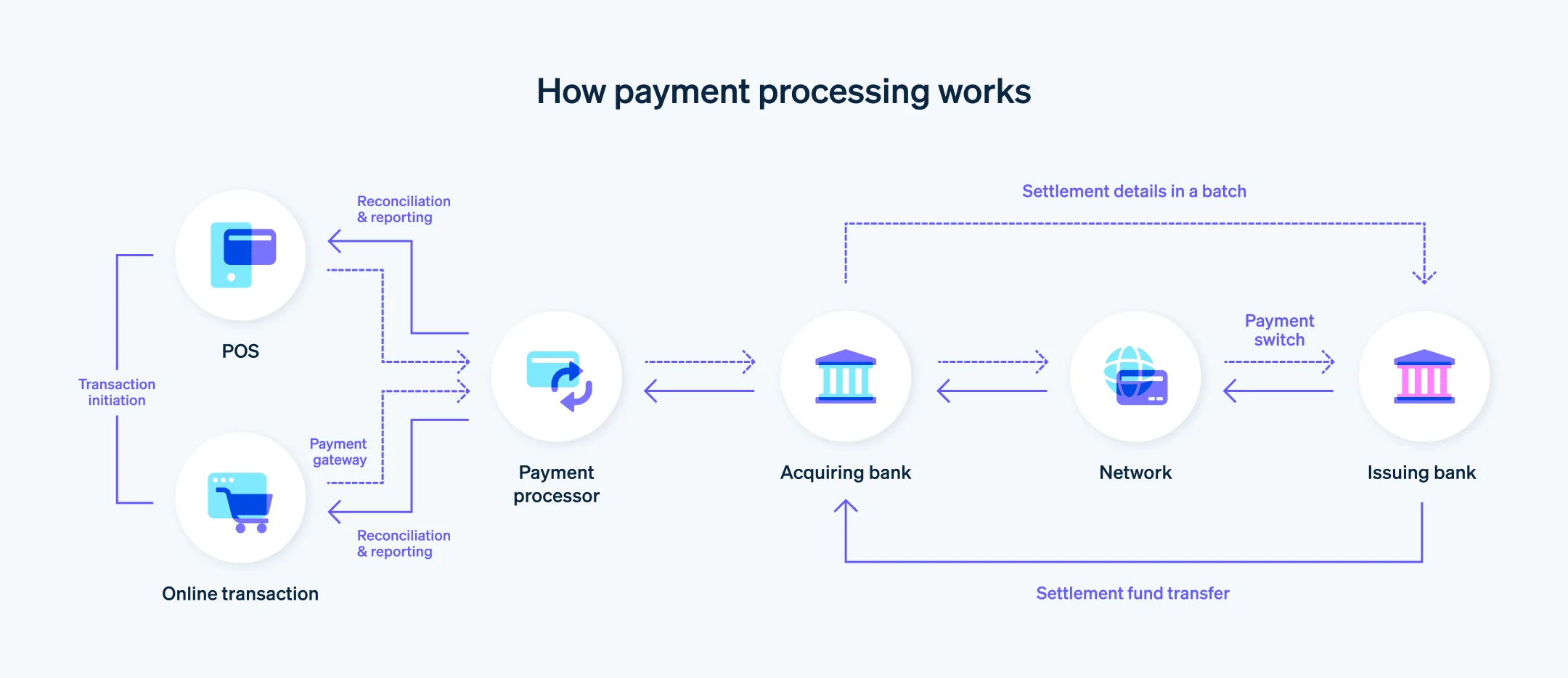

At its core, a payment system is an orchestration layer that moves money and data between customers, merchants, banks, and networks.

The architecture is made up of various system components – such as payment gateways, processors, PSPs, ledgers, and integration layers – that work together to enable secure and reliable transactions. It sits in the middle of a complex web of relationships and gives each party what they need to perform their part of the transaction flow. A well-designed payment system reliably handles, tracks, and secures financial transactions to ensure accuracy, compliance, and trustworthiness in monetary exchanges.

It consists of several roles:

- Payment gateway: securely collects and encrypts payment data.

- Payment processor: communicates with acquirers, issuers, and networks to authorise transactions.

- PSP (Payment Service Provider): offers merchants the full set of services required to accept online payments.

- Acquiring bank: represents the merchant and processes card transactions.

- Issuing bank: holds the customer’s account and approves or declines payments.

When a transaction occurs, these actors exchange messages in milliseconds, running fraud checks, validating funds, applying rules, and updating balances. The payment system orchestrates this entire process: receiving requests, applying business logic, sending messages to networks, updating the ledger, and eventually settling funds. This end-to-end process is known as the payment cycle, which includes pay-in and pay-out flows, transaction tracking, reconciliation, and security at each stage to ensure reliability and correctness.

Introduction to Online Payments

Online payments have become the backbone of modern commerce, empowering businesses to accept payments from customers around the world with unprecedented ease. At the heart of every successful online transaction is a payment processor, which acts as the critical link between a customer’s bank account and the business’s bank account.

The payment processing system is made up of several interconnected components:

- the payment gateway,

- payment service provider,

- acquiring bank.

The payment gateway serves as the secure entry point for payment information, encrypting sensitive data and transmitting it safely to the payment processor. The payment processor then communicates with the acquiring bank and other financial institutions to authorize and complete the transaction. By leveraging advanced payment processing capabilities, businesses can streamline online transactions, reduce friction at checkout, and offer a seamless payment experience to their customers.

Understanding how these elements work together is essential for any business looking to expand its reach, increase revenue, and stay competitive in the digital economy. With the right payment processing system in place, companies can confidently accept payments online, knowing that every transaction is handled efficiently and securely.

Why Companies Build Their Own Payment System Today

Most businesses start out using external PSPs, and in the early stages this approach works well. It’s fast to set up, affordable, and doesn’t require a large operational team. In the broader payment business landscape, this is a common entry point for companies and service providers operating within the payments ecosystem. Over time, though, as transaction volumes rise and companies expand into new regions, the limits of a third-party setup become increasingly visible. What once felt convenient starts slowing the organisation down, especially for high-volume or multi-market products.

- Control over the experience. Owning the payment layer lets companies shape the checkout flow, fine-tune routing rules, adjust business logic, and manage customer communication without waiting on a provider.

- Less dependence on external providers. PSP outages, pricing changes, feature delays, and geographic restrictions all become potential risks when the entire payment flow sits outside the company’s control.

- Better long-term economics. At scale, routing transactions internally or working directly with acquirers can meaningfully reduce processing costs.

- Room for custom featuresю Teams can introduce instant payouts, internal transfers, multi-currency accounts, card issuing, or crypto rails in line with their product vision rather than a PSP’s roadmap.

- Security and data ownership. Operating your own engine means full access to transactional data — essential for analytics, fraud modelling, and meeting regulatory expectations.

As products evolve, the most innovative use cases often demand capabilities that external PSPs cannot deliver or prioritise. Internal payment systems give companies the flexibility to build the features they need, exactly when they need them. Building a robust system is essential for scaling operations and meeting the compliance and security requirements expected in the financial technology sector.

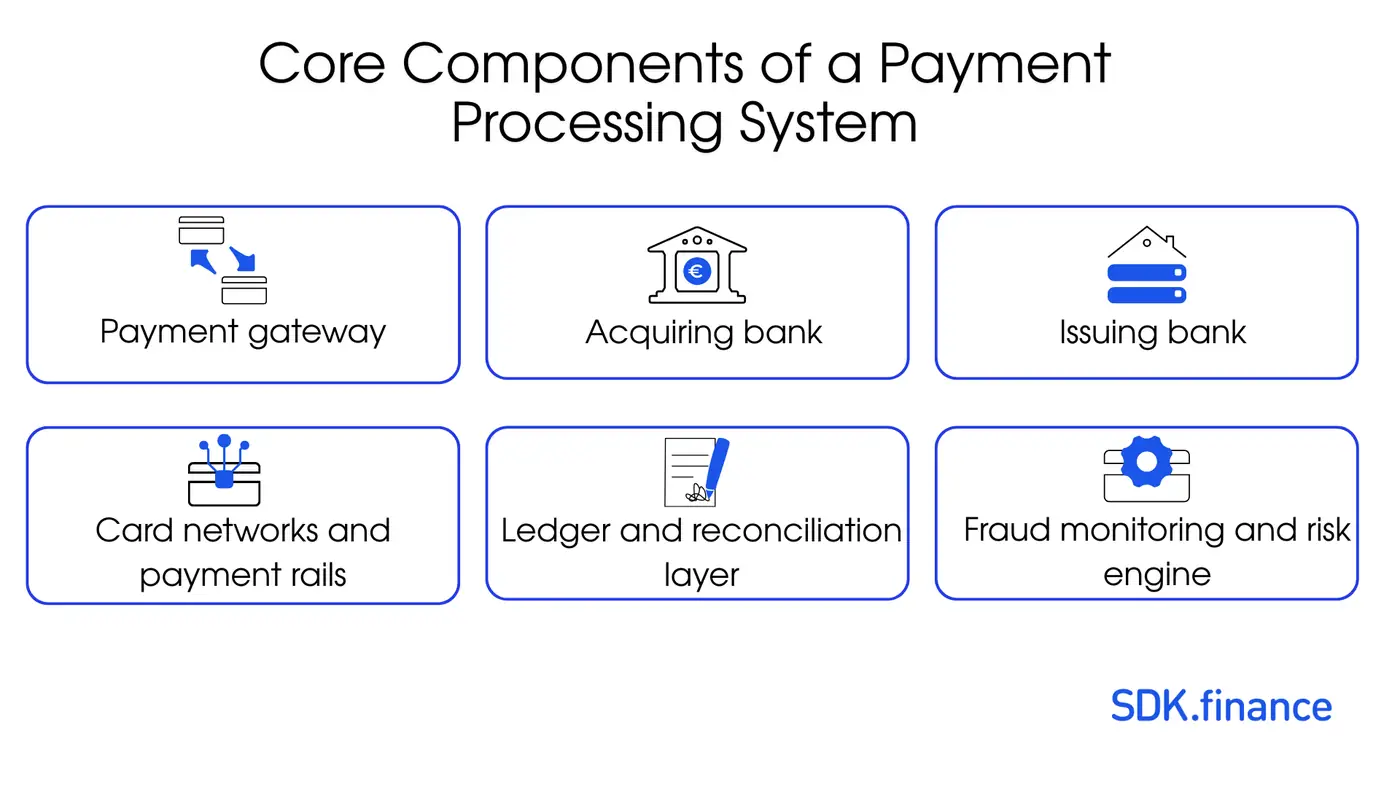

Core Components of a Modern Payment Processing System

A payment system may look like one product from the outside, but behind the scenes it’s a set of tightly connected parts—including various internal services such as accounting, analytics, and wallets—that have to work in sync to support the payment flow. Understanding these components, which collectively facilitate and manage payment transactions throughout the system, helps teams decide what is truly worth building in-house and what is smarter to source from proven payment processing platforms.

User and Merchant Onboarding

Onboarding is the first real point of trust. For consumers, it usually involves identity checks, document verification, sanctions screening, and basic risk scoring. Merchant onboarding goes further: reviewing company documents, ownership structure, expected volumes, and overall risk level. A good onboarding flow protects the system while keeping conversion rates healthy.

Payment Gateway

This is the touchpoint where customers enter their card or banking details, including sensitive credit card details and payment details. A strong gateway handles tokenisation, 3-D Secure, device checks, and localised checkout options. It also ensures that transaction details and transaction information are securely encrypted and transmitted to the payment processor, and manages retries and fallback routing so transactions don’t fail unnecessarily.

Payment Processor

The processor communicates with issuing and acquiring banks, converting requests into the formats networks understand. The payment processor sends transaction data to payment networks, such as Visa or Mastercard, to obtain authorization and facilitate settlement between the merchant and the customer’s bank. In the overall transaction workflow, a payment processor works by authenticating the customer, authorizing the transaction, and acting as a mediator between merchants and financial institutions to ensure secure and efficient payment processing. It manages authorisations, captures, refunds, and reversals. Most businesses rely on external processors, but they keep routing and orchestration logic under their own control.

Fraud & Risk Management

Fraud control is never just one tool. It’s a combination of rules, behavioural checks, sanctions screening, and sometimes machine-learning models. These systems detect suspicious patterns, block abusive behaviour, and protect merchants. Building this alone requires specialist knowledge, so many teams blend in-house logic with external fraud tools.

Ledger and Accounting Engine

The ledger is the system’s backbone. It records every movement of funds accurately – from holds and fees to FX and reversals. A reliable ledger must be immutable, multi-currency, and fully auditable. Implementing a double entry system is essential for ensuring transaction accuracy, end-to-end traceability, and regulatory compliance. The ledger service acts as a core component, maintaining transaction records and supporting the double-entry accounting principle. The ledger service appends new entries in an append-only manner, preserving data immutability and consistency for all financial transactions. The underlying data model typically includes a transaction table, which tracks all financial movements and provides a complete audit trail. Because mistakes here directly create financial and regulatory problems, many companies integrate a ready-made ledger rather than trying to build their own.

Settlement & Reconciliation

Authorising a transaction is only the start. Funds must eventually move, and internal records must match reports from banks and processors. Automated reconciliation ensures that all the transactions are accounted for by verifying consistency between internal logs and external settlement reports. Tracking transaction status throughout the payment cycle is crucial for identifying failures or delays and maintaining auditability. These reconciliation processes are essential for upholding financial integrity, as they help catch discrepancies early and remove hours of manual work.

Compliance: KYC/AML, PCI DSS

Payments are heavily regulated. Identity checks, monitoring, sanctions screening, and fraud controls need to be built into the system from day one. Handling card data introduces PCI DSS obligations, while wallets or stored balances trigger PI/EMI requirements.

Reporting, Analytics, Back Office Tools

Operational teams need visibility. Finance, risk, support, and compliance all require their own tools for reviewing transactions, resolving issues, and tracking performance. Access to detailed transaction history is crucial for finance and compliance teams to ensure accurate record-keeping, facilitate audits, and support regulatory reporting. Many teams underestimate how complex these internal systems can become – they often match the front-end in terms of effort and importance.

Planning Your Payment System: Key Decisions

Licensing vs Operating Under a Partner

One of the most consequential decisions in any payment system roadmap has surprisingly little to do with technology. It centres on whether the company should apply for its own financial licence or begin operations by relying on an already licensed institution. This choice determines how quickly you can launch, what services you can legally provide, and how much of the payment lifecycle you can control from day one.

In most jurisdictions, regulated payment activity falls under two key authorisation types:

- Payment Institution (PI) – permission to process and execute payments, manage merchant acquiring, and handle transfers.

- Electronic Money Institution (EMI) – includes PI permissions, plus issuing and holding electronic money, providing wallet balances, multi-currency accounts, stored value, and sometimes card issuing.

Obtaining either licence is not simply an administrative exercise. Regulators typically require companies to demonstrate:

- a transparent governance and ownership structure

- experienced, “fit and proper” leadership

- detailed AML and counter-fraud frameworks

- safeguarding arrangements for customer funds

- minimum capital requirements

- documented operational resilience planning

- audited financial statements

- robust cybersecurity and IT controls

- risk management policies and clear reporting procedures

These obligations come with financial impact. The true cost of securing a licence includes application fees, legal and compliance advisory, external audits, internal hires, capital deposits, and the infrastructure adjustments needed to satisfy regulatory expectations.

Below is an approximate view of what these licences cost across major regions.

Estimated Cost of Obtaining a Payment Licence (by Region)

Approximate ranges reflecting real-world totals – legal work, documentation, audits, capital requirements, and operational readiness.

| Region | Licence Type | Estimated Total Cost (USD) | Notes |

|---|---|---|---|

| European Union | EMI | 250,000 – 1,000,000+ | Includes 350k EUR capital, legal, audits, staffing, policies. |

| PI | 80,000 – 300,000+ | Lower thresholds but still requires full AML/IT documentation. | |

| United Kingdom | EMI (FCA) | 300,000 – 1,200,000+ | FCA places strong focus on resilience and wind-down planning. |

| PI (FCA) | 120,000 – 400,000+ | Depends on business model complexity and risk profile. | |

| United States | Money Transmitter Licences | 1,000,000 – 5,000,000+ total | Licensing is state-by-state; each state has its own fees and bonding requirements. |

| MENA (UAE, Bahrain) | Payment/Fintech Licences | 150,000 – 500,000+ | Varies by licence category and central bank requirements. |

| Asia (Singapore) | PSA Licence | 300,000 – 1,000,000+ | Includes cybersecurity audits, IT assessments, and compliance setup. |

These figures are not official tariffs, but they represent the realistic investment required to assemble the legal, operational, and technical framework regulators expect from a licensed payment institution.

Because of the high entry barrier, many companies choose a phased approach instead of applying for a licence immediately. Common pathways include:

- Sponsored PSP model – the regulated partner executes payment operations while you manage the product.

- Authorised Agent (EU/UK) – you operate under the umbrella of an EMI/PI licence and appear in official registers.

- Technical Service Provider – your company provides the technology layer, while the licensed entity handles all regulated functions.

This approach allows businesses to go live significantly faster, validate demand, build revenue, and later decide whether obtaining a full licence makes strategic and financial sense.

Choosing Supported Payment Methods

From cards to instant payments to crypto, as well as bank transfers and credit card payments, each option shapes your technical and compliance obligations.

For international transactions, supporting currency exchange is essential to enable seamless multi-currency operations and ensure reliable global payment flows.

Supported Geographies and Currencies

A system intended for Europe must be architected differently from one serving the US or MENA, especially when you need a high-performance transaction processing system that can handle diverse schemes and volumes.

Security Requirements (PCI DSS, Tokenisation)

Security controls determine how card data is stored, transmitted, and insulated from breaches.

Integration Stack (APIs, Gateways, Banks)

Modern systems are essentially integration networks; the quality of APIs determines how easily the product evolves.

How to Build Your Own Payment System

Creating a payment system is far more demanding than building a typical digital product and often exposes teams to the hidden cost of fintech software development. Payments sit at the intersection of finance, regulation, and cybersecurity, which means the system must be resilient, auditable, and capable of adapting to legal and compliance changes that rarely stand still.

When designing a payment system, it is crucial to define both the pay in flow (handling incoming payments from the customer’s account to the business’s account or merchant account) and the pay out flow (managing outgoing payments from the business’s bank account to sellers or merchants). These flows ensure secure, reliable, and efficient movement of funds throughout the payment lifecycle.

Each payment event encapsulates the details of a transaction and triggers downstream processes such as ledger updates, wallet adjustments, and reconciliation. A single payment event can represent an individual transaction, serving as a key unit for processing, idempotency checks, and tracking within the system.

A core component in this architecture is the payment executor, which is responsible for executing individual payment orders through external Payment Service Providers (PSPs). The payment executor calls interact with third-party PSPs to process payment requests, manage execution status, and handle failures to ensure reliable deposit and withdrawal operations. The payment executor stores transaction data, including payment orders and statuses, in a persistent storage system to guarantee accurate processing and fault tolerance.

The wallet service manages user and merchant balances, with the wallet server stores maintaining account balances and transaction history to ensure secure and consistent financial record-keeping. Payment service stores are critical for securely storing and managing payment data, supporting reconciliation, compliance, and data integrity.

Tracking seller’s balance information is essential for accurate payouts and reconciliation, as it reflects the funds available for disbursement and affects transaction consistency. Throughout the payment flows, funds move between the customer’s account, business’s account, business’s bank account, and merchant account, ensuring seamless and secure transactions for all parties involved.

Below is a compressed, practical view of the stages most teams follow when bringing a payment system to life, especially if the goal is to start a payment processing company.

Solutions for Building a Payment System

When planning technical implementation, companies eventually choose between two paths, including using dedicated payment processing software to become a PSP.

One is to build the entire platform internally. The other is to start with a white-label PSP platform and customise it.

Both are valid. The choice depends on resources, timelines, and long-term strategy.

Custom In-House Development

Suitable for companies with unique technical requirements and large engineering teams. Brings full control but demands time, compliance investment, and deep technical expertise.

White-Label Solutions for PSP

A white-label PSP platform provides a pre-built financial core, dramatically reducing the technical and operational burden, especially when it’s part of an enterprise fintech platform for banking and payment solutions. These solutions typically include onboarding modules, a ledger, routing engines, settlement and reconciliation workflows, back-office tools, PCI DSS – aligned infrastructure, and connectors to acquirers and gateways. For many companies, this approach accelerates time to market while still offering room for customisation.

Build vs Buy: Should You Develop a Payment System from Scratch?

| Factor | Build In-House | White-Label |

|---|---|---|

| Time to Market | 12-36 months | 3-6 months |

| Upfront Cost | High | Lower |

| Compliance | Fully internal | Largely vendor-supported |

| Engineering Complexity | Very high | Moderate |

| Best For | Specialist platforms | Fast-growing businesses |

SDK.finance White-Label Solution for PSPs

For many companies, the biggest obstacle in entering the payments market isn’t the idea itself – it’s the time, cost, and expertise needed to build the core infrastructure. White-label PSP platforms like SDK.finance address this by giving teams an operational foundation that already handles the most demanding parts of payment processing.

These systems usually come with the building blocks that otherwise take months or years to engineer. For example:

- ready-made onboarding and KYB flows

- routing, settlement, and reconciliation modules that already follow industry logic

- PCI DSS–aligned security architecture, including tokenisation and controlled data zones

- merchant portals and internal dashboards for finance, compliance, and support teams

- connectors to acquirers, gateways, and external service providers

- pre-built mobile or web interfaces for customer-facing use cases

- shorter certification and approval timelines, since core components are already tested

The advantage is not only speed but also risk reduction. Instead of building the financial engine from the ground up, companies can focus on shaping the user experience, refining commercial models, and expanding into new markets. The white-label core quietly handles the heavy lifting – the parts of payments that must work flawlessly from day one.

SDK.finance is often selected by teams that want to enter the payments market quickly, without giving up stability, flexibility, or control. Instead of piecing together multiple vendors or trying to develop core components from scratch, companies get access to an all-in-one backend shaped specifically for the demands of modern, high-volume payments.

At the centre of the platform is a robust ledger built for intensive financial operations. Around it is a set of ready-made modules covering the essential building blocks of a PSP, including:

- Merchant onboarding and KYB

- Payment routing and orchestration

- Settlement and reconciliation

- Flexible fee and commission management

- Chargeback and dispute handling

- KYC/AML compliance tools

- Multi-currency wallets and account management

- IBAN and virtual IBAN accounts

- Card issuing

- Reporting and analytics

- User and role management (RBAC)

- API gateway and audit logs

- Asset and token management

- Crypto on-ramp and off-ramp flows

The platform includes 570+ REST APIs, a comprehensive back office for finance, compliance, support, and risk teams, and a white-label mobile app that can be adapted to your brand and product design.

For companies that want a dependable, comprehensive starting point – and prefer not to spend years rebuilding the same financial infrastructure – SDK.finance offers a practical, proven path to market.

Conclusion

Building a payment system is no longer reserved for banks or the largest fintechs. With the right design, licensing approach, and technology stack, businesses can internalise payments and gain significant strategic advantages. White-label cores such as SDK.finance shorten the journey, reduce risk, and provide a powerful foundation for innovation.

The same principles apply when you create a digital-only banking app or launch a neobank using SDK.finance.