FinTech products that operate across borders, serve multiple merchant types, or support wallets in more than one currency face a structural challenge that a basic balance table cannot solve:

How do you keep separate, accurate, and auditable balance states for USD, EUR, GBP, and other currencies within a single operational system - without collapsing them into one abstract number?

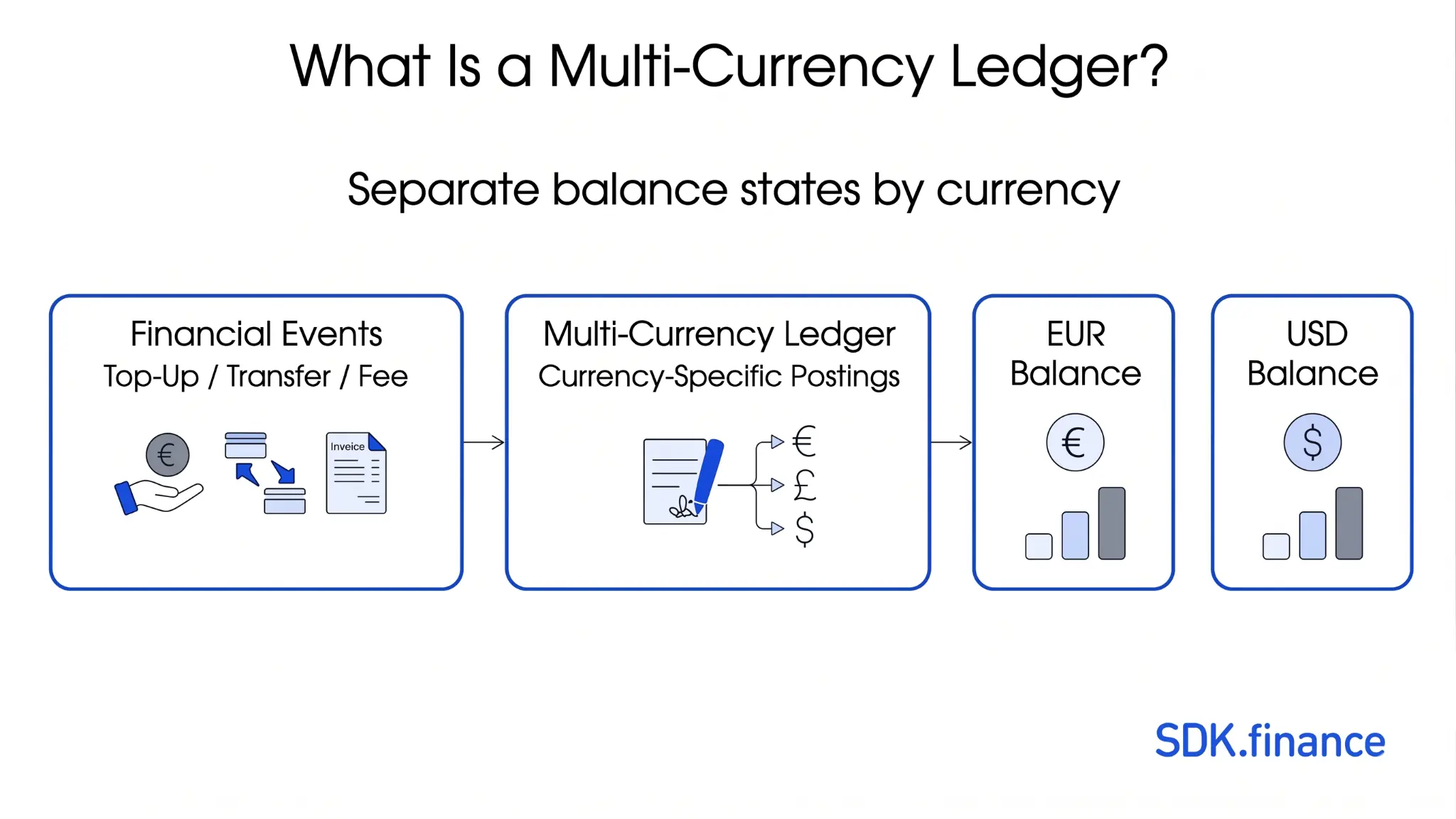

That is the problem a multi-currency ledger is built to address. It is the operational layer that records every money movement event with its currency context, maintains distinct balance states per currency, and produces the reconciliation-ready history that finance and engineering teams need to operate at scale. Understanding what it is – and what it is not – matters for anyone designing or evaluating ledger infrastructure for a modern fintech product.

This article explains what a multi-currency ledger is, how it works mechanically, why FinTech products need it, how it differs from adjacent systems like wallet ledgers and general ledgers, and what to look for when building or evaluating one.

The Short Answer

- It keeps distinct balances per currency – USD, EUR, GBP, and others are tracked independently, not collapsed into one running total

- Every posting carries currency context, so transfers, fees, and payouts are recorded with the specific currency of each movement

- It supports internal transfers, fee accounting, payout tracking, and settlement visibility across currencies in a single coherent system

- It preserves an immutable, reconciliation-ready history of how balances changed over time, including pending, posted, and settled states by currency

What Is a Multi-Currency Ledger?

This is an important distinction. A multi-currency ledger is not a single balance displayed in multiple currencies. It is not a conversion layer that translates a USD balance into EUR for display purposes.

Each currency has its own balance state, its own ledger treatment, and its own posting history. If a user holds USD and EUR simultaneously, those are two balance objects with independent lifecycles – not one balance with a display flag.

The mechanics are built on double-entry bookkeeping: every transaction is represented by balanced postings across at least two accounts, with each posting carrying its currency denomination. This means a cross-currency movement – say, a EUR deposit that funds a USD payout – is modeled as explicit, currency-specific postings plus any associated FX fee entries, rather than one opaque net update. The result is a system where balances are always derivable from the event log, not just stored as a column value.

Why FinTech Products Need a Multi-Currency Ledger

Most fintech products reach a point where a single-currency ledger or a simple balance table stops being sufficient. The moment a product accepts payments in one currency, holds balances in another, and pays out in a third, the gaps become operationally painful.

At that point, separate balance tracking by currency is no longer a nice-to-have. It becomes part of the operational infrastructure needed to keep wallet balances, merchant balances, fees, and settlement states coherent.

- Payment service providers need to track merchant balances across multiple settlement currencies, apply fees in the correct denomination, and reconcile incoming funds against outgoing payouts without losing the currency context of each movement.

- Cross-border wallet products need to maintain distinct available balances per currency for each user, record top-ups and transfers accurately regardless of which rail delivered them, and produce transaction histories that correctly represent the currency of each event.

- Neobanks with foreign-currency accounts need per-currency balance states that can support real-time authorization, hold placement, and settlement, with reconciliation against card networks and partner banks that settle in different currencies.

- Payout products – whether serving freelancers, gig workers, or marketplace sellers – need to separate the payout currency from the holding currency, track what has been paid out versus what is pending, and match internal records against provider settlement files.

- Marketplaces need to track funds on behalf of multiple parties simultaneously, including platform fees, seller balances, and buyer activity, often across currencies and payment rails. Without a multi-currency ledger, this quickly becomes a fragmented, error-prone process.

In each of these cases, the operational need is the same: explicit balance tracking by currency, with a posted event history that can be reconciled against external systems.

How a Multi-Currency Ledger Works

Separate Balances by Currency

USD, EUR, GBP, and other currencies cannot be treated as one abstract balance. Each currency represents a distinct liability or asset state in your system, and the behavior of funds in each currency may differ – in settlement timing, in the rails used for payout, in the regulatory treatment of held funds, and in the FX exposure if conversion has not yet occurred.

A well-designed multi-currency ledger maintains these as separate balance objects, each queryable independently. A typical implementation will also split balance state further by availability: distinguishing between what is pending, what is available, and what has been settled externally. This gives product and operations teams an accurate picture of liquidity per currency at any point in time, rather than a single aggregate that obscures in-flight state.

Ledger Postings for Transfers, Fees, and Payouts

The double-entry structure of a ledger posting does not change when multiple currencies are involved – but each posting must carry its currency denomination, and the balancing rule applies within each currency, not across them.

A transfer from a EUR wallet to another EUR wallet is a balanced pair of postings in EUR. A cross-currency movement – a USD receipt that funds a EUR payout – is modeled as a set of currency-specific postings: one reducing the USD balance, one increasing the EUR balance, and a separate entry for any FX fee, recorded against a dedicated fee account. This explicit treatment prevents the common failure mode of older single-currency designs, where lack of cross-ledger atomicity allows one side of a transaction to succeed while the other fails, creating balance inconsistencies that require manual intervention.

Fees and commissions should be modeled as first-class postings, not as implicit adjustments. An application fee, an FX markup, or a payout fee should each appear as a distinct ledger entry against the appropriate account, in the appropriate currency. This keeps the event log clean and makes fee reconciliation tractable.

Transaction History and Reconciliation by Currency

The practical value of a ledger over a balance table is its history. A balance table tells you the current state. A ledger tells you how you got there – and that history must be queryable by currency to be useful.

When a finance team needs to reconcile a EUR settlement file against internal balance movements, they need a filtered view of EUR postings, not a search through a mixed-currency event log. When an operations team is investigating a discrepancy in a payout run, they need the payout state per currency, linked to the individual transactions that composed it.

Reconciliation-ready history means every ledger entry carries enough metadata to stitch it back to the external event it represents: the provider reference, the payment ID, the settlement batch, the account the funds moved through. This is what allows internal ledger state to be matched against bank files, processor settlement reports, and partner rail data without resorting to manual matching.

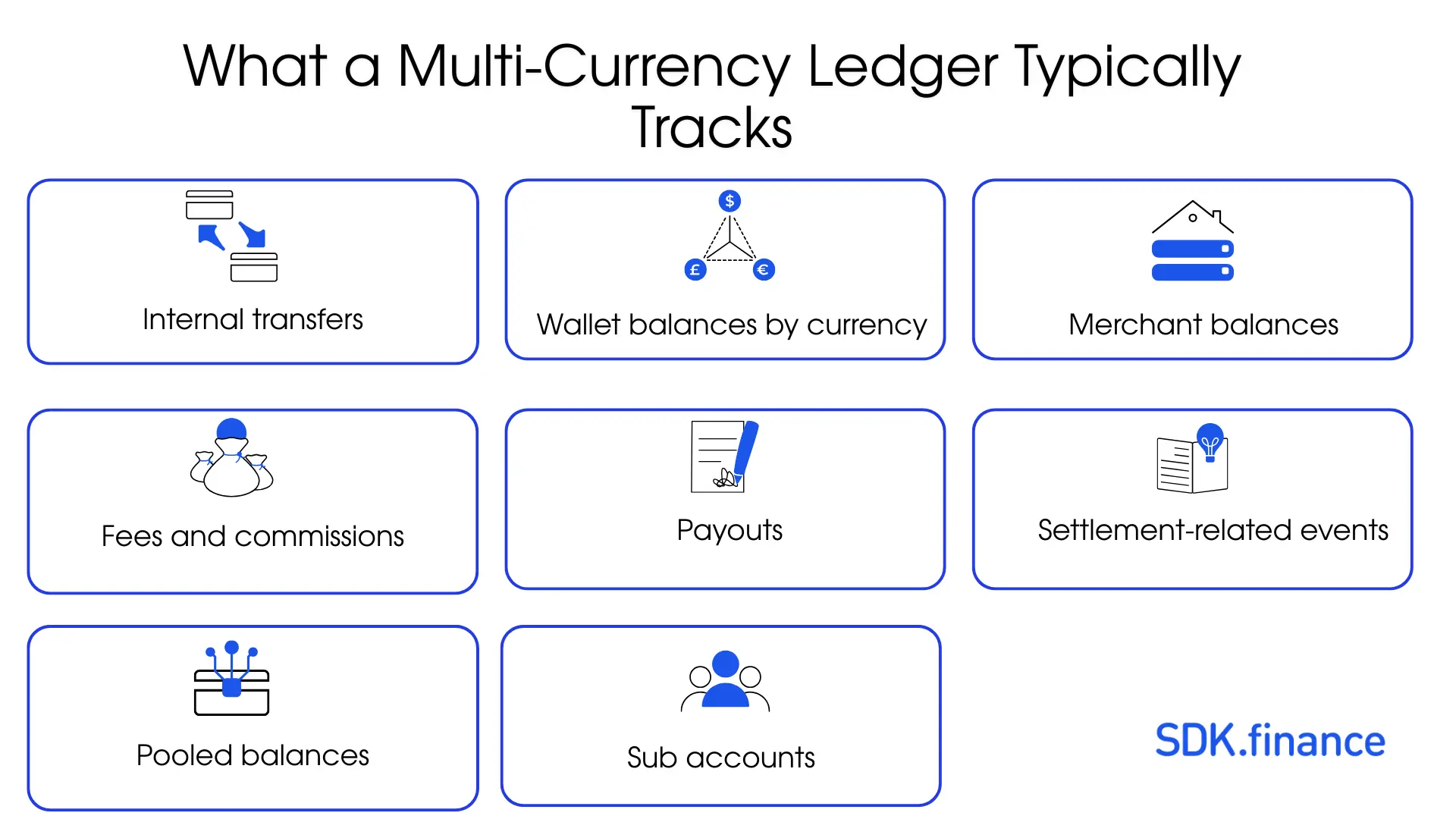

What a Multi-Currency Ledger Typically Tracks

The scope of a multi-currency ledger covers all balance-impacting events across the currencies your product handles. In practice, this typically includes:

- Wallet balances by currency. User-facing stored-value balances, each maintained as a separate balance state per currency with full posting history.

- Merchant balances. Funds held on behalf of merchants or sellers, segmented by currency and by lifecycle state – processing, available for payout, reserved.

- Internal transfers. Movements between accounts within the same system, modeled as balanced postings rather than net balance updates, to preserve traceability.

- Fees and commissions. Platform fees, processing fees, FX fees, and payout fees, each recorded as explicit entries against dedicated accounts in the relevant currency.

- Payouts. Movements from internal balances to external accounts, tracked by currency, with payout state (initiated, processing, settled, failed) recorded against the relevant balance.

- Settlement-related events. Inbound settlement from card networks, processors, or banking partners, matched against internal posted entries to confirm that external funds have moved as expected.

- Pooled balances. Where funds are held in a pooled or FBO account, the ledger provides the sub-ledger layer that tracks each user’s or entity’s entitlement within the pool, by currency.

- Sub-accounts. Hierarchical account structures that separate balances by user, product, program, or lifecycle state – enabling segmentation without requiring separate physical accounts.

Multi-Currency Ledger vs Wallet Ledger

These concepts are related but not the same.

A wallet ledger is the ledgering model behind stored-value or FBO-wallet products. It focuses on user balances, funding events, peer-to-peer transfers, and payouts – the operational layer that a wallet product depends on to track what each user holds and how that holding changes over time.

A multi-currency ledger is a capability layer, not a use-case layer. It describes how a ledger handles currency-separated balance tracking, whether the product is a wallet, a PSP platform, a payout service, or a marketplace. A wallet ledger may be multi-currency if the product supports balances in more than one currency, but the two concepts are not interchangeable: a wallet ledger can be single-currency, and a multi-currency ledger can serve products that are not wallets.

The practical distinction matters when designing infrastructure. If your product is a wallet, you are designing a wallet ledger – and the question of whether it needs multi-currency support is a feature decision. If you are designing or evaluating the underlying ledger infrastructure, multi-currency capability is an architectural question about how currency is represented in balance and posting logic.

Multi-Currency Ledger vs General Ledger

A general ledger organizes financial events to represent the financial position of the business for accounting and reporting purposes. It lives in an ERP or accounting system and is optimized for producing balance sheets, income statements, and formal financial records.

A multi-currency ledger is an operational balance layer. It is optimized for real-time product behavior – authorizing transactions, updating balances, recording postings, and supporting reconciliation against external systems. It is not a replacement for a general ledger, nor does it serve the same function.

The relationship between the two is downstream: the operational ledger records product-level money movement in real time, and that data feeds into accounting systems where it is reorganized for financial reporting. As discussed further in Product Ledger vs General Ledger, the two layers have different audiences, different optimization targets, and different update frequencies. Conflating them produces either an operational system that is too slow, or an accounting system that is too noisy.

Common Multi-Currency Use Cases

PSPs and Merchant Balances

Payment service providers accept funds across currencies, distribute to merchants in various denominations, and settle across different rails. The multi-currency ledger is what keeps merchant balances coherent when incoming settlement, outgoing payouts, and platform fees each touch different currencies.

Real-time reconciliation across ACH, card networks, wire, and faster-payment rails requires one authoritative ledger state rather than separate, rail-specific ledger entries. Without that structure, balance ownership, fee treatment, and payout visibility become harder to trace across currencies.

Cross-Border Wallets

Products that allow users to hold, send, and receive money in multiple currencies need per-currency balance states at every step – top-up, hold, transfer, conversion, and payout. The presentment currency, the settlement currency, and the payout currency may all differ for a single user action. The ledger must preserve each of these distinctions rather than flatten them, or the product loses the ability to explain to users (and regulators) exactly what happened to their funds.

Neobanks with Foreign-Currency Accounts

Neobanks that offer foreign-currency accounts or multi-currency spending cards need a ledger capable of maintaining distinct balances per currency, tracking card authorization and settlement amounts (which may differ due to FX), and reconciling against card network settlement files that express amounts in a settlement currency that may not match the user’s held currency.

Marketplaces and Payout Products

Marketplace platforms must track funds on behalf of sellers, buyers, and the platform itself – often simultaneously, often in more than one currency. Payout products serving freelancers or gig workers face similar complexity: the worker earns in one currency, the platform holds in another, and the payout settles in a third. In both cases, the ledger must support multi-party balance tracking, configurable account structures, and currency-level payout visibility.

Products with Sub-Wallets and Pooled Balances

Products that use FBO or pooled account structures hold commingled funds at a banking partner while tracking individual user entitlements internally. The multi-currency ledger provides the sub-ledger layer that makes this work: per-user, per-currency balance entries that collectively reconcile against the total pooled balance at the custodian bank. Without robust sub-ledger tracking in this model, segregation breaks down and reconciliation becomes a manual exercise.

Design Challenges in Multi-Currency Ledger Systems

- Balance consistency across currencies. When a cross-currency movement is split across multiple ledgers or handled non-atomically, one side can succeed while the other fails. This creates inconsistent balances and typically requires engineer and finance intervention to resolve. The solution is atomicity at the transaction level – a cross-currency movement should either fully post in both currencies or not post at all.

- Internal transfers. Modeling transfers as balanced postings rather than net balance updates is architecturally straightforward but requires discipline. Ad hoc implementations tend to drift toward direct balance mutations, which are harder to audit, harder to reverse, and harder to reconcile.

- Payout-state visibility. A payout is not a single event. It passes through initiated, processing, in-transit, settled, and potentially failed or returned states. Each state transition should produce a ledger event, so the system can answer questions like “what is the pending payout balance in EUR right now” without querying external provider APIs.

- Fee logic by currency. Fees assessed in a different currency than the underlying transaction introduce conversion logic. If this logic is not modeled explicitly in the ledger – with dedicated fee accounts and currency-specific posting rules – it becomes invisible to reconciliation and difficult to audit.

- Reconciliation complexity. Matching internal ledger records against external settlement files requires that every posting carry enough metadata to identify the external event it corresponds to. In multi-currency systems, this metadata must also include currency, so that EUR settlement files are matched against EUR postings specifically, rather than against a mixed-currency set of entries.

- Account hierarchy design. A useful multi-currency ledger needs a structured chart of accounts – not a flat list of user IDs. Hierarchical account structures allow segmentation by currency, by lifecycle state, by user type, and by product line, making balance queries and reconciliation practical at scale.

- Scaling without breaking correctness. High-volume systems must make explicit tradeoffs between throughput and consistency. Strong consistency is appropriate for accounts that gate authorization decisions; eventual consistency may be acceptable for reporting aggregates. These choices need to be designed in from the start, not retrofitted when volume increases.

What Makes a Good Multi-Currency Ledger

- Real-time balance visibility. Balance state should update immediately when postings are confirmed, so product logic and operations teams are working from current data, not lagged aggregates.

- Structured posting logic. Every balance-impacting event should be represented as a double-entry posting, with currency, amount, timestamp, and the relevant account identifiers. Direct balance mutations are an anti-pattern.

- Clear account hierarchy. Accounts should be organized hierarchically, with meaningful paths that reflect the business structure – separating user accounts from fee accounts, liability accounts from asset accounts, and pending balances from settled balances.

- Reconciliation-ready records. Every posting should carry the metadata needed to link it to an external event: provider reference, payment ID, settlement batch, external account. This is what makes automated reconciliation possible.

- Support for internal transfers. Transfers between accounts within the system should be first-class ledger operations – not workarounds or balance updates applied outside the posting model.

- Support for multiple account types. Wallet accounts, merchant accounts, fee accounts, reserve accounts, and settlement accounts have different behaviors and visibility requirements. A good ledger supports all of them within the same posting framework, rather than requiring separate systems for each.

How SDK.finance Supports Multi-Currency Ledger Use Cases

SDK.finance’s real-time ledger software and wallet ledger software are designed for fintech products that need:

- multi-currency balance tracking,

- double-entry posting logic,

- and reconciliation-ready records across wallet, PSP, and payment operations.

The platform is designed to maintain separate balance states by currency, so wallet, merchant, and operational accounts can be tracked independently without collapsing multi-currency activity into one aggregated balance.

The platform supports multi-currency wallet balances, sub-account structures, internal transfers, fee accounting, and payout tracking – the operational capabilities that make a multi-currency ledger usable in production rather than a theoretical architecture. For teams building PSP platforms, cross-border wallets, neobank products, or marketplace payment infrastructure, SDK.finance provides the ledger layer that sits underneath product flows and connects to external payment rails.

Conclusion

A multi-currency ledger is the operational balance infrastructure that makes it possible for fintech products to track funds accurately when more than one currency is involved. Its defining feature is not multi-currency display – it is separate balance states per currency, maintained through structured double-entry postings, with a history that can be reconciled against external payment systems.

For PSPs managing merchant balances across settlement currencies, for wallets that allow users to hold EUR and USD simultaneously, for neobanks with foreign-currency accounts, and for marketplaces tracking multi-party funds across rails, the multi-currency ledger is the layer that keeps balance state coherent, fees traceable, payouts visible, and reconciliation tractable.

Modern fintech products do not operate in one currency in one jurisdiction. The ledger infrastructure that supports them should not, either.