While traditional payment rails like SWIFT and ACH have been the backbone of transactions for decades, they often fall short in today’s digital-first, on-demand economy.

A2A payment methods have emerged as 2024’s leading digital payments trend, challenging the dominance of international giants like Visa and Mastercard. From instant transfers to razor-thin fees, A2A payments are rewriting the rules.

So, how do they stack up against the old-school methods? Let’s break down the battle between A2A and traditional rails.

Traditional payment rails in different regions

From ACH in the U.S. to SEPA in Europe and the UK’s Faster Payments, traditional payment rails reflect the unique needs and constraints of its region.

While these systems have supported reliable transactions for years, they also reveal a range of regional differences in speed, costs, and cross-border capabilities—highlighting the strengths and challenges of each.

United States ACH payments

In the United States, the Automated Clearing House (ACH) serves as the foundation for various types of transactions, including payroll deposits, tax payments, peer-to-peer (P2P) transfers, and e-commerce transactions. ACH processes these transactions in batches, which provides stability but limits speed and flexibility.

Most ACH transfers take 1 to 3 business days to complete, making the network less suitable for the immediate demands of today’s on-demand economy. Although some banks do offer faster ACH options, they can be expensive, and tracking capabilities are often limited. Additionally, the average ACH transaction limit typically hovers around $25,000 per transaction, which may not be adequate for larger B2B payments.

Account-to-account (A2A) payments could address the issues of speed, cost, and transparency in the U.S. financial landscape by enabling real-time, low-cost transactions without the need for intermediaries. As the FedNow service is rolled out, A2A solutions could enhance accessibility and potentially challenge ACH’s dominance as the primary payment rail.

Europe: SEPA’s reach and A2A’s Appeal

Europe has one of the most integrated cross-border payment systems in the world: the Single Euro Payments Area (SEPA). SEPA standardizes euro-denominated transactions across 36 countries, making payments nearly as simple and cost-effective as domestic transfers. For even faster transactions, SEPA Instant offers near-instantaneous transfers within the SEPA network. This system is ideal for cross-border transactions in Europe, as it eliminates fees and supports same-day or next-day settlements for standard transfers.

However, SEPA Instant’s reach is limited to participants within the SEPA network, and there are caps on certain transactions, which can make it less effective for some B2B transfers.

There is potential for account-to-account (A2A) payments to build on SEPA’s success by extending fast, secure, and low-cost payments beyond the SEPA zone. With Europe’s Open Banking regulations promoting direct account-to-account payments, A2A payments could become a seamless and preferred option for both international and domestic transactions.

United Kingdom’s faster payments service

The UK’s Faster Payments Service (FPS) is an efficient system that enables nearly instant transfers within the country. FPS processes domestic payments in under 15 seconds and is accessible through most banks, although some may impose transfer limits or charge additional fees.

For high-value transactions, the Clearing House Automated Payment System (CHAPS) offers same-day settlement, but at a higher cost. This makes CHAPS more suitable for large corporate transactions rather than everyday consumer payments.

In contrast, Bacs (Bankers’ Automated Clearing Services) is primarily used for payroll and direct debits, taking 2-3 business days to process. This delay does not meet the immediacy required for many modern payment scenarios.

Although FPS is quick for domestic transactions, it does not support international payments. Account-to-account (A2A) payments could enhance the ability to make direct, real-time transfers beyond the UK, which would benefit both businesses and individuals with cross-border needs.

Middle East and North Africa (MENA)

In the MENA region, payment systems vary significantly from country to country, featuring a mixture of domestic solutions and a dependence on international services for cross-border transactions.

In Saudi Arabia, SADAD is a well-integrated system designed for bill payments within the Kingdom. However, it has limited interoperability with other regional systems, making cross-border transfers challenging.

Bahrain’s Fawri+ is a more advanced payment system that supports near-instant domestic transfers. Nevertheless, its capabilities for cross-border transactions are limited, which can hinder businesses and consumers in need of international payment solutions.

There is potential for Account-to-Account (A2A) payments to streamline cross-border transactions in MENA, particularly by reducing reliance on SWIFT for international transfers. As governments in the region demonstrate a growing interest in developing faster and more efficient payment rails, A2A payments emerge as a compelling alternative.

Asia-Pacific (APAC)

The APAC region displays significant variation in payment infrastructure. For example, Japan has a highly reliable but outdated system, whereas Australia has adopted modern payment technologies.

Japan’s Zengin System facilitates same-day transfers on business days; however, its batch processing methods mean it lacks the real-time immediacy needed for today’s digital transactions. In contrast, Australia’s New Payments Platform (NPP) offers 24/7 real-time payments across banks, allowing both consumers and businesses to make fast, low-cost transfers effortlessly.

The potential for A2A payments includes Japan and other APAC countries with legacy systems could greatly benefit from Account-to-Account (A2A) payments, which would enhance immediacy and transparency in interbank transactions. Meanwhile, in markets like Australia, A2A payments could support seamless international transactions, building on the capabilities that the NPP already provides domestically.

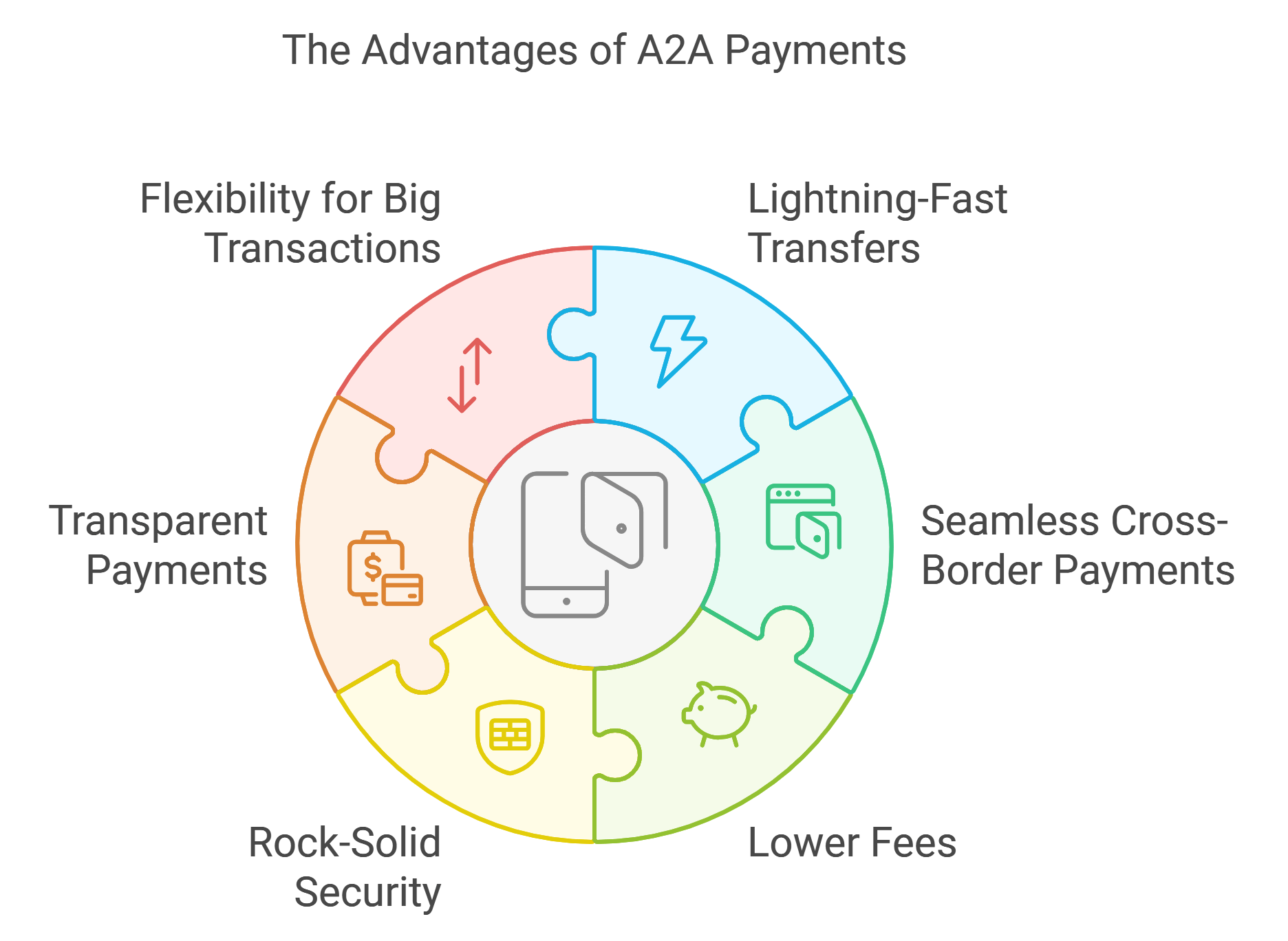

Advantages of A2A payments over traditional payment flows

As businesses and consumers gravitate toward smarter payment solutions, A2A payments have emerged as a game-changer, leaving traditional rails in the dust. Here’s a closer look at how A2A payments deliver unique advantages:

Lightning-fast transfers

Traditional transfers can take 1–3 business days, while A2A payments whisk funds from one account to another in a flash. This speed is a game changer for e-commerce, gig economy platforms, and P2P payments, where every second counts.

Lower fees

Traditional payment systems involve multiple intermediaries, leading to increased costs per transaction. With A2A payments, funds move directly from one account to another, reducing or eliminating fees associated with intermediaries.

In the Nordic countries, platforms like Vipps, Swish, and MobilePay showcase how cost-effective A2A payments can be compared to credit card options.

Seamless cross-border payments

Traditional cross-border payment systems, such as SWIFT, can be expensive and may take several days to settle, especially when multiple intermediaries are involved. In contrast, A2A payments facilitate seamless cross-border transactions, particularly in regions with open banking regulations.

Take Klarna, for instance, which enables quick cross-border transfers across Europe without needing intermediary banks—ideal for businesses catering to international customers.

Rock-solid security

With the rise of open banking standards, account-to-account (A2A) payments utilize multi-factor authentication and advanced data protection protocols, making them safer than many traditional payment methods.

For example, services like Plaid in the U.S. use encrypted bank APIs to authenticate users directly with their banks, thereby reducing the risk of card-not-present fraud, which is more common with credit card transactions.

Transparent payments

Traditional payment systems often leave users confused, particularly with cross-border transfers that navigate through multiple banks. Account-to-account (A2A) payments, on the other hand, provide real-time notifications, allowing both businesses and customers to stay informed about their transactions.

For example, the European A2A platform Tink offers detailed tracking that enhances transparency and improves the overall payment experience, contributing to better financial management.

Flexibility for big transactions

Need to move big money? Traditional systems often come with restrictive transaction limits—like the $25,000 cap on ACH payments in the U.S. A2A payments offer greater flexibility, making them the go-to choice for high-value business-to-business (B2B) transactions.

In Australia, the New Payments Platform (NPP) empowers instant, high-value transactions, streamlining business payments without the usual constraints.

With SDK.finance Platform scalability, that processes up to 2700 transactions per second (TPS), you can handle over 233 million daily transactions even on a basic configuration. This robust system accommodates transaction volumes from 1,000 up to 1 billion monthly transactions with ease, ensuring no performance hiccups. SDK.finance’s flexibility means your business can handle high-value transactions smoothly, adapting to your expanding needs without compromise.

Future of A2A payments

Global A2A (Account-to-Account) payments are set to skyrocket, with transaction volumes soaring from 60 billion in 2024 to a staggering 186 billion by 2029—a 209% surge!

A2A payments have gained a competitive edge over other methods, offering instant settlements and lower transaction fees than cards—making them increasingly appealing to merchants. This shift toward A2A is reflected in the rising transaction volumes across Europe’s top platforms.

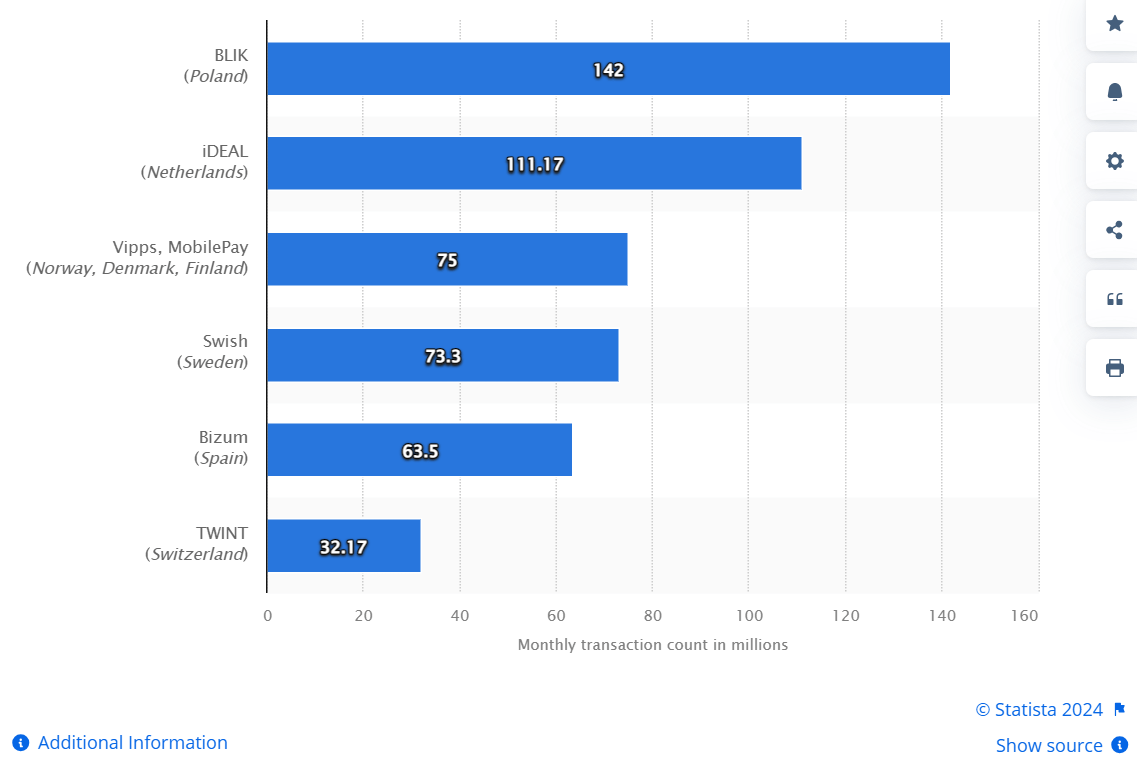

Top brands for monthly A2A transactions in Europe, 2023

Source: Statista

According to Statista, A2A payments are rapidly gaining traction across Europe. Leading the way are Poland’s BLIK with 142 million monthly transactions, the Netherlands’ iDEAL with 111 million, and Vipps and MobilePay (used in Norway, Denmark, and Finland) with 75 million transactions monthly.

Impact of VRPs on A2A payments

Open Banking developments have paved the way for the rapid rise of A2A solutions. A notable innovation in this space is Variable Recurring Payments (VRPs), which allow customers to link authorized payment providers directly to their bank accounts. This connection enables seamless, agreed-upon recurring payments within specified limits.

As a result, businesses and banks are increasingly interested in VRPs, as they offer greater flexibility and transparency compared to traditional direct debit methods, enhancing the overall payment experience for both parties.