Financial super apps are changing the way we manage money by bringing together a wide range of financial and lifestyle services in one easy-to-use platform. These all-in-one apps are becoming popular worldwide, offering a new approach to banking and how people handle their finances by automating processes like transaction handling and data compilation, alleviating the burdens of traditional banking functions.

The rise of super apps is fueled by the growing need for convenience, personalized experiences, and smooth digital interactions. By combining services like payments, transfers, investments, and insurance, these platforms are positioning themselves as the central hub for all things financial.

This article explores the key features that define next-generation finance through the lens of banking super app examples, showcasing how platforms like SDK.finance are driving this transformation.

What is a banking super app?

A banking super app is a mobile application that combines various financial services into a single, convenient platform. It’s designed to streamline your financial life by offering multiple features in one app. By automating traditional banking functions, these apps allow banks to focus on fostering deeper relationships with their customers and enhancing customer engagement. Rather than requiring multiple apps for various tasks such as payments, shopping, transportation, or messaging, a super app enables users to accomplish all of these tasks—and more—within a single app.

This offers users a highly convenient and seamless experience, allowing them to access a variety of services without needing to switch between different platforms. Super apps are especially popular in regions like Asia but are gaining global traction as they change the way people engage with digital services.

Historical Context and Development of Super Apps

The concept of super apps was initially coined by Mike Lazaridis in 2010. However, it wasn’t until the rise of fintech and mobile technology that super apps began to gain significant traction. In Asia, particularly in China and Southeast Asia, super apps have become incredibly popular, with companies like WeChat and Alipay leading the way.

These apps have evolved from simple messaging or payment platforms to comprehensive ecosystems that offer a wide range of financial and lifestyle services. For instance, WeChat started as a messaging app but quickly expanded to include payments, e-commerce, and even government services. Similarly, Alipay began as a payment solution for Alibaba’s e-commerce platforms and has since grown to offer investments, insurance, and various lifestyle services.

The success of these super apps in Asia has demonstrated the potential of integrating multiple services into a single platform, setting a precedent for similar developments in other regions.

The evolution of banking super apps

The fintech super apps have changed a lot. They used to do only one thing, like peer-to-peer payments. But now they do a lot more. Fintech super apps have evolved from simple payment platforms to include traditional banking functions like transaction handling and data compilation. They offer many different services all in one place.

Chinese super apps like WeChat and Alipay have been important in making this trend popular around the world. They show how these all-in-one apps can be important in the market by combining messaging, payments, shopping, and other services.

The fast growth of fintech super apps is driven by several key factors:

Technologies

Advanced technologies like cloud computing, AI, and mobile technology have made it possible to develop advanced super app platforms. These technologies ensure easy user experiences, provide smart data insights, and offer new and innovative services.

Additionally, these technologies support the automation of traditional banking functions, allowing banks to focus on enhancing customer relationships and loyalty.

User convenience

Users are looking for more convenient ways to manage their finances and daily activities. Super apps make life simpler and save time by offering a wide range of services in one place.

RegTech

Regulatory changes, such as open banking and fintech-friendly regulations, have made it easier to share data and increased competition, paving the way for super apps and accelerating their growth.

These changes impact traditional banking functions by enabling easier data sharing and increased competition.

Global leaders: Banking super app examples

Super apps are changing traditional banking by offering all-in-one platforms that not only provide financial services but also integrate various other functions, creating comprehensive ecosystems within a single application. These companies are pioneering the fintech landscape and are transforming the way people manage their finances.

Western markets

PayPal

PayPal

PayPal started as an online payment processor for eBay transactions. It has expanded to offer a wide range of financial services, including person-to-person payments, credit services, and cryptocurrency trading.

PayPal also incorporates traditional banking functions like transaction handling and data compilation into its platform.

Key features:

- Simplified checkout: PayPal’s One-Touch checkout makes online shopping easier by letting users make purchases with a single click, making it more convenient and reducing abandoned carts.

- Loans for small businesses: PayPal offers working capital loans to small businesses based on their sales history on the platform to help them grow and run their operations.

- Venmo incorporated: PayPal has included Venmo, a popular social payments platform, so that users can easily send and receive money while adding social features like shared payments and comments.

- Cryptocurrency services: Users can now buy, sell, and hold cryptocurrencies directly within the PayPal app, catering to the growing interest in digital assets.

PayPal uses its large number of users, built up over many years as a trusted online payment provider, to introduce and expand new financial services. This has made PayPal an important player in the rapidly growing fintech super app industry.

Revolut

Revolut

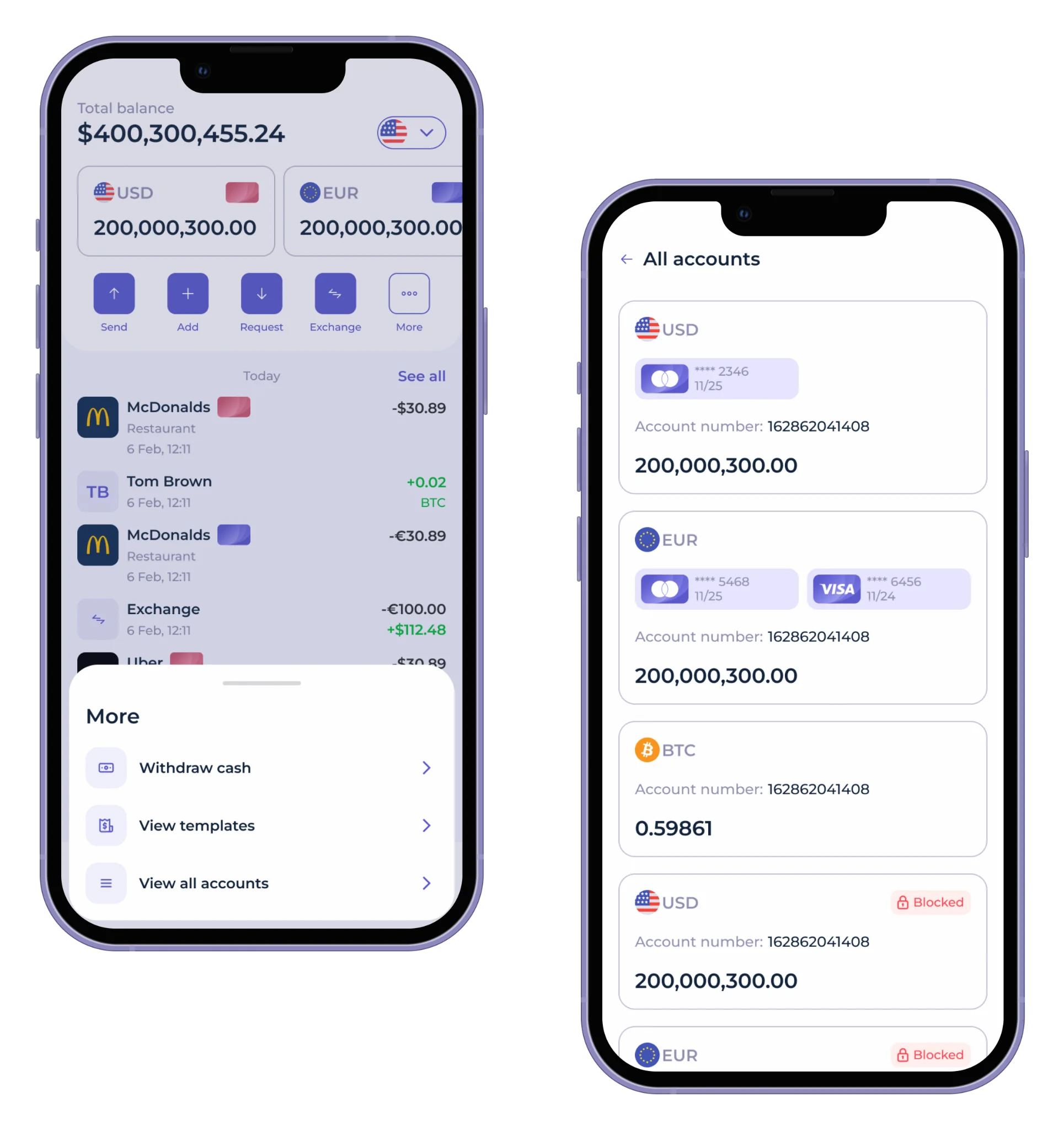

Revolut started as a travel card with great foreign exchange rates. Now it’s a full-service banking platform offering many financial services like traditional banks.

Here are the key features:

- Multi-currency accounts: Revolut lets users hold and manage multiple currencies with local bank details in different countries, making it popular for travelers and expatriates.

- Commission-free stock trading: Users can invest in global markets with minimal barriers because Revolut offers commission-free stock trading, making investing more accessible.

- Budgeting tools: Real-time expense categorization and budgeting tools help users manage their finances better.

- Crypto and commodities: Revolut also offers crypto trading and commodities investing, providing a comprehensive range of investment options.

- Innovation: Revolut is known for quickly introducing new features and expanding into new markets, which has helped it build a diverse and engaged user base globally.

Asian markets

Alipay

Alipay

Alipay started as a way to pay for things on Alibaba’s websites. Now it’s a super app that offers lots of financial and lifestyle services. Here are the key things about Alipay:

- Payments: With Alipay, you can pay for things online, in stores, bills, and public services.

- Investments: You can invest in money market funds and other things through the app.

- Insurance: Alipay offers various insurance, like health, life, and property insurance in the app.

- Lifestyle: Alipay also offers things like food delivery, ride-hailing, and travel booking.

Alipay has changed the way people pay for things in China. It has made digital payments common and changed how people behave in the country.

WeChat Pay

WeChat Pay

Originally, WeChat started as a messaging app. It then added a payment feature, which expanded into a wide range of financial services. This made WeChat an important part of everyday life in China. WeChat’s mini-programs let third-party services work within the app.

They offer a variety of things like e-commerce, gaming, and government services, all without leaving the app. WeChat Pay’s strategy is to create a closed ecosystem where users can do almost all their daily activities, from socializing to handling financial transactions, without leaving the app.

Emerging market innovation of FinTech super apps

Nubank

Nubank

Nubank started by offering a credit card with no fees, which was a new idea in a market where traditional banks charge high fees. They have since expanded into full digital banking services, meeting a wide range of financial needs.

Key features:

- Digital bank accounts: Nubank offers digital accounts with no fees, free transfers, and easy mobile access. This is appealing to younger, tech-savvy people.

- International transfers: They provide international transfer services, making it useful for users involved in global transactions.

- Personal loans and insurance: Nubank offers personal loans and has recently started offering life insurance. This expands its products to cover more aspects of personal finance.

Nubank is at the forefront of financial inclusion in Latin America. It challenges traditional banks by offering low-cost financial services to millions of people, particularly those who are underserved by traditional banking.

M-Pesa

M-Pesa

M-Pesa revolutionized financial access in Kenya and across Africa by providing a mobile-based platform for P2P transfers, bill payments, and more, in regions where traditional banking infrastructure is limited.

Initially focused on simple money transfers, M-Pesa has grown to offer a broader range of financial services, including savings accounts, microloans, and international remittances.

M-Pesa showcases the power of mobile-first financial super apps to leapfrog traditional banking in developing markets, providing essential financial services to millions who previously had little or no access to formal banking.

Key features driving financial super app adoption

Super apps are becoming popular worldwide because they offer a seamless user experience and valuable features. These features make them more appealing to users and set them apart from traditional financial and lifestyle apps. In this section, we’ll explore the main elements driving the widespread adoption of super apps.

Seamless user experience across services

Banking super apps provide a seamless user experience across various services. Users can access all features of the app without managing multiple logins or accounts, thanks to a single sign-on system. The consistent user interface and design across different services within the app make it easier for users to navigate and utilize the app’s offerings.

Personalized offerings through data integration

Banking super apps leverage data integration to provide personalized experiences. By analyzing user data such as spending patterns and preferences, these apps offer AI-driven financial advice tailored to individual needs. This could include suggestions for budgeting, investing, or saving based on the user’s unique financial behavior.

In-app marketplaces and third-party integrations

Financial super apps include in-app marketplaces and the ability to integrate with third-party services. Similar to WeChat’s mini-programs, super apps often host an ecosystem of third-party applications within their platform, allowing users to access a wide range of services without leaving the app. These in-app marketplaces enable users to shop, book services, or access government services directly through the super app.

SDK.finance’s Platform is designed to support these extensive integrations, providing the APIs and modular architecture needed to incorporate third-party services seamlessly. This capability allows super apps to expand their offerings rapidly, providing users with a comprehensive solution that meets various needs in one place.

Challenges and considerations

The growth of financial super apps brings many benefits, but also some challenges.

Payment regulations

The diverse financial regulations in different countries make it hard for super apps to expand globally while following the rules. For example, a banking super app operating in multiple regions has to meet different licensing requirements, anti-money laundering (AML) laws, and consumer protection regulations. This slows down expansion and raises operational costs. Data protection laws, like the General Data Protection Regulation (GDPR) in Europe, set strict guidelines for how companies can collect, store, and use personal data. Following these rules is important, but it also takes a lot of resources and might limit how super apps can use user data to offer personalized services.

Data privacy and security concerns

Another concern is the privacy and security of user data. When a lot of sensitive information is in one place, it’s important to protect it. Users worry about how their data gets used, and losing their trust could harm a company’s reputation and user confidence. Also, payment apps need strong cybersecurity measures to guard against things like data breaches, identity theft, and fraud. This includes keeping a close eye on things, encrypting data, using secure logins, and actively preventing fraud.

Build a financial super app on top of SDK.finance platform

SDK.finance offers a powerful FinTech Platform that supports the creation of super app experiences, allowing both traditional banks and fintech startups to focus on customer engagement and service innovation without getting bogged down by technological complexities.

SDK.finance’s software solutions enable a wide range of features within a super app:

- Accounts in any currency

- Currency exchange

- Popular payments

- P2P money transfers

- Visa/MasterCard issuing

SDK.finance’s modular platform allows for easy customization and integration of third-party services, ensuring that each super app can be tailored to the specific needs of its user base. Whether it’s enabling secure, real-time transactions or offering AI-driven financial planning tools, SDK.finance provides the technological foundation that makes these capabilities possible.

Watch the SDK.finance Platform demo video to explore key features you get out of the box with our solution:

By leveraging SDK.finance’s expertise, financial institutions can accelerate their digital transformation journeys, offering super app experiences that not only meet but exceed the demands of modern users.

SDK.finance in Action: A Super App Case Study

One of the most illustrative examples of SDK.finance’s contribution to the super app landscape comes from a large-scale implementation in the Maghreb region. A company building a comprehensive super app for taxi services, food and grocery delivery, and digital payments turned to SDK.finance to accelerate its infrastructure development.

Instead of building everything from the ground up, the company licensed the SDK.finance source code to lay the foundation of its fintech backend. This approach allowed the team to fast-track the creation of essential banking and wallet features, including transaction management, multi-service user onboarding, and secure digital payments — all from a single, unified platform.

By relying on SDK.finance’s modular architecture and 470+ ready-to-use APIs, the super app’s developers were able to:

-

Launch faster by skipping years of backend development.

-

Retain full control over the codebase, enabling long-term customisation and scalability.

-

Integrate a multi-service payment infrastructure that supports high transaction volumes and diverse use cases.

-

Maintain strict data control and compliance standards thanks to the self-hosted, ledger-based backend.

This case highlights how SDK.finance can serve as a powerful enabler for companies aiming to build regional or vertical super apps. Whether it’s ride-hailing, deliveries, or digital payments, the SDK.finance Platform provides the tools to tie everything together securely and efficiently.

Conclusion

As we enter a new era in financial technology, banking super apps are not just a passing trend – they represent the future of finance. By combining a wide array of services into one platform, they are setting new standards for convenience, personalization, and digital engagement.

Whether you are a traditional bank seeking to innovate or a fintech startup aiming to disrupt, the emergence of super apps – driven by technology leaders like SDK.finance – signifies a crucial moment in the ongoing evolution of finance.