People often mix up “payment gateway” and “payment processor,” but they actually handle very different parts of a transaction. If you think of payments like a relay race, the gateway starts the run while the processor finishes it.

In this piece, experts from leading digital payment software provider SDK.finance will break down these concepts, explaining how the two fit into both online (card-not-present) and POS (card-present) acquiring. We’ll cover what each does, how they interact with banks and card networks, how they make money, and what kind of risks and licences are involved. There’s even a comparison table at the end if you’re the type who likes to see it all laid out neatly.

Definitions and Roles

A payment gateway is basically the digital front door of a transaction. It's the bit of tech that securely captures a customer's card info-think of that checkout form you fill out when buying something online-and passes it along for processing.

It encrypts the card data, runs some basic fraud checks (and sometimes 3-D Secure), and sends the authorisation request off to whoever’s handling the heavy lifting. Once the result comes back-approved or declined-the gateway shows it to the customer and the merchant. Its main job? Keep things secure, fast, and fraud-resistant.

To simplify: the gateway is the front end you see; the processor is the back-end machine that moves the money.

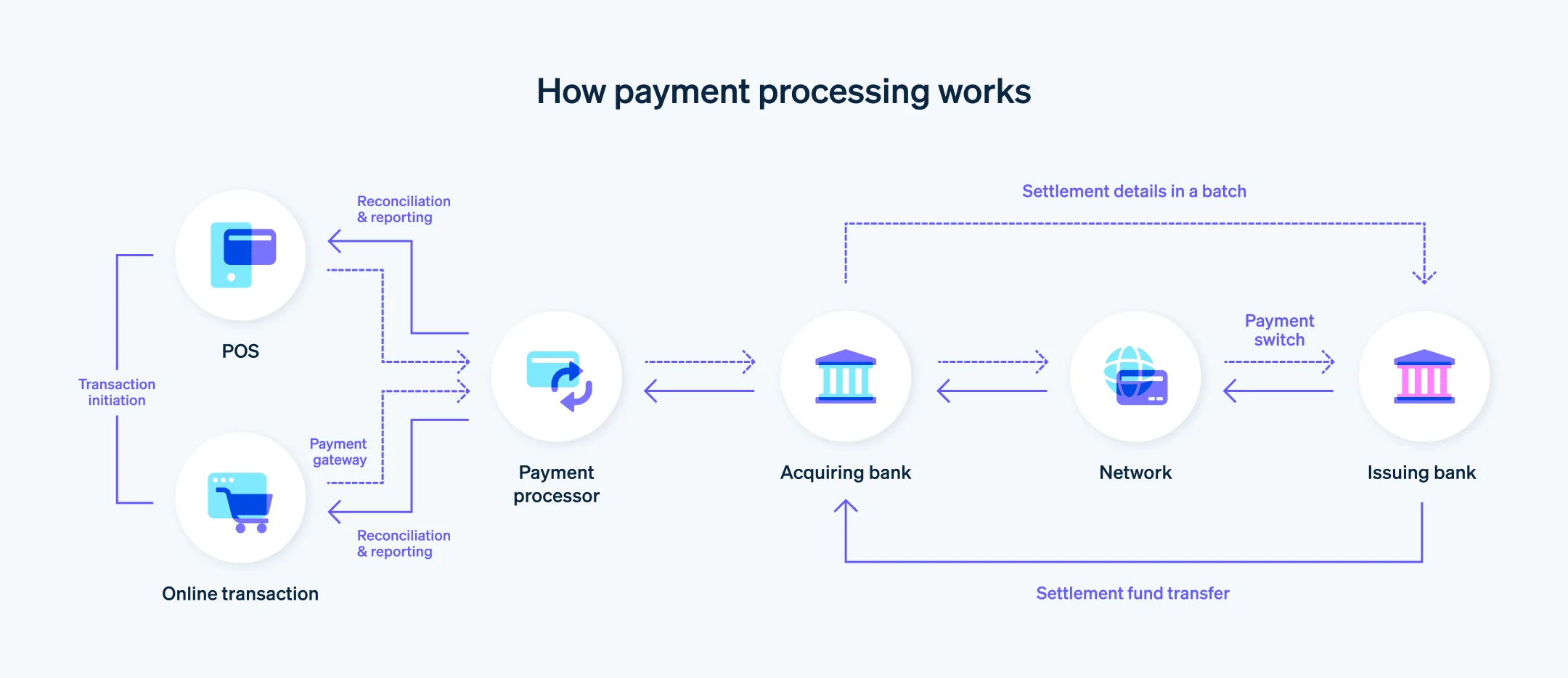

Online Acquiring (Card-Not-Present)

When you buy something online or in an app, both parts-the gateway and the processor-are usually involved.

Here’s the flow in plain English:

- You (the customer) type your card details on the checkout page.

- The gateway encrypts that info, does fraud checks or 3-D Secure if needed, and forwards an authorisation request to the processor.

- The processor then sends it through the card network to your bank (the issuer). The bank approves or declines it and sends the response back.

- The gateway tells the merchant (and you) what happened. If it’s approved, your bank reserves the amount.

- Later, the processor kicks off clearing and settlement-money leaves your account, flows through the card network, reaches the acquirer, and finally lands in the merchant’s bank account. The gateway’s done its part by then.

POS Acquiring (Card-Present)

At a physical store, things look a bit different. The POS terminal-whether it’s a card reader, a self-checkout, or a smartphone with a tap-to-pay app-takes over the role of the gateway.

Here’s the gist:

- The terminal reads your card (magstripe, chip, or NFC).

- It sends the authorisation request straight to the processor or acquirer.

- The processor does its routing magic, gets the decision back, and sends it to the terminal.

- You get a receipt, and everyone’s happy.

Clearing and settlement happen later, just like in online payments. In most POS setups, you don’t need a separate gateway, since the terminal already does that job. Large chains might still use a “gateway-like” system to connect multiple acquirers for reliability or cost optimization.

Responsibilities and Interactions

The gateway connects merchants and customers. It handles the checkout UI, encryption, tokenisation, and some fraud prevention. It doesn’t touch the actual funds-it just passes secure data to one or more processors.

The processor connects to the banking world. It communicates with card networks and issuers, manages clearing and settlement, and keeps up with strict compliance and reporting rules.

Pro insight from SDK.finance: In practice, a payment gateway and a payment processor can exist within a single solution only if a provider owns the entire payment infrastructure. However, in many cases, these functions are handled by different vendors– one focusing on secure data transmission, the other on authorisation and settlement.

Sometimes a single company handles both parts. These “full-stack PSPs” (like Stripe or Adyen) make life easier by giving merchants one contract, one integration, and one support team.

Business Models and Licensing

How they make money:

- Gateways typically charge a fixed fee per transaction or a monthly subscription. Extras like advanced fraud tools or reporting dashboards can cost more. They don’t earn from interchange or network fees.

- Processors/Acquirers earn from the merchant discount rate (MDR), which is a small percentage of each transaction. That covers interchange (what goes to the issuing bank), card scheme fees, and the processor’s own margin. They might also charge for chargeback handling, merchant onboarding, or terminal rentals.

Licensing and Regulation:

- Gateways are mostly tech companies. They don’t need a banking license unless they actually hold or move funds. Still, they must comply with PCI DSS and data protection laws. If a gateway starts acting as a payment facilitator (boarding merchants and managing settlements), it usually falls under regulated PSP or EMI rules.

- Processors are financial institutions, plain and simple. They’re either licensed acquirers themselves or work under one. They have to meet regulatory requirements like AML/CTF checks, PCI DSS, capital adequacy, and operational resilience standards.

Risks and Liabilities

Gateways deal mainly with technical and reputational risks-system downtime, data breaches, or weak fraud filters. While they’re not financially responsible for chargebacks, a security failure can seriously damage trust and lead to penalties or lost clients.

Processors, meanwhile, carry the real financial risk. They handle merchant funds, so they face chargeback exposure, scheme fines, compliance audits, and settlement or liquidity challenges. They’re also the ones on the hook for ensuring funds move correctly and legally.

Examples

- Payment Gateways: Authorize.Net, CyberSource, Braintree, Stripe (gateway layer), Adyen (gateway module), Uniteller, Payture, CloudPayments.

- Processors/Acquirers: Fiserv, Worldpay, Global Payments, Adyen (as acquirer), Stripe (processing layer), major bank acquirers like Barclays, plus PayPal and Square as PSPs.

What is the difference between payment gateway and payment processor?

The main difference between a payment gateway and a payment processor lies in what stage of the transaction they handle and how they interact with other parties in the payment flow.

Payment gateway: the front door of the transaction

A payment gateway acts as the digital interface that securely transmits payment data from the customer to the processor.

It’s typically used for online transactions (card-not-present) or POS terminals that need to encrypt and send payment data.

Payment processor: the middleman that moves the money

A payment processor is the engine that communicates with card networks (Visa, Mastercard, etc.) and banks to authorise and settle transactions.

It’s responsible for the movement of funds between the customer’s issuing bank and the merchant’s acquiring bank.

Side-by-Side Snapshot

| Parameter | Payment Gateway | Payment Processor |

|---|---|---|

| Role | Collects card data securely and forwards it for authorisation; returns result to merchant. | Routes authorisations via card networks, handles clearing and settlement to the merchant. |

| Key Functions | Checkout UI, encryption, tokenisation, 3-D Secure, basic fraud screening. | Network connectivity, authorisation routing, clearing, settlement, reporting, compliance. |

| Online Acquiring | Always needed to capture card data securely. | Always needed to execute the transaction flow. |

| POS Acquiring | Usually built into the terminal; sometimes used for routing across multiple acquirers. | Mandatory for all POS transactions. |

| Counterparties | Merchant and customer. | Acquirer, card networks, and issuers. |

| Licensing | Tech provider; PCI DSS required. Not regulated unless handling funds. | Financially regulated; must hold acquiring licenses and comply with AML/CTF rules. |

| Liability | Responsible for secure data handling; not liable for fund movement. | Bears chargeback and settlement risk. |

| Revenue Model | Fixed or monthly fees, add-ons for fraud tools and reporting. | Percentage-based MDR plus extra fees. |

| Examples | Authorize.Net, Braintree, Stripe, Adyen (gateway). | Fiserv, Worldpay, Adyen (acquiring), Stripe (processing), PayPal. |

Conclusion

In short, payment gateways and processors work hand in hand. The gateway is about capturing data securely and making the checkout experience smooth; the processor takes care of the actual money movement, authorisation, and settlement.

For online payments, you’ll almost always need both. At a physical point of sale, the terminal often does the gateway’s job, but you still need the processor to move the funds.

From a business perspective, the gateway is a tech service focused on security and reliability, while the processor is a regulated financial service focused on compliance and fund movement. Knowing where one ends and the other begins helps merchants pick the right setup-whether that’s a standalone gateway and acquirer or an all-in-one PSP-and helps banks and fintechs design their own solutions smartly.