Nowadays, launching card programs has become more streamlined and efficient than previously, however there may still be challenges and complications to consider. That’s why it is crucial to account for potential obstacles such as regulatory requirements, and technical issues.

In this article, we explore the key steps on how to launch a card issuing program and explore a solution to accelerate this process.

The basics of card issuing

Before launching your card issuing program, it’s crucial to have an understanding of the whole process for making informed decisions and implementing a successful card program.

What is card issuing?

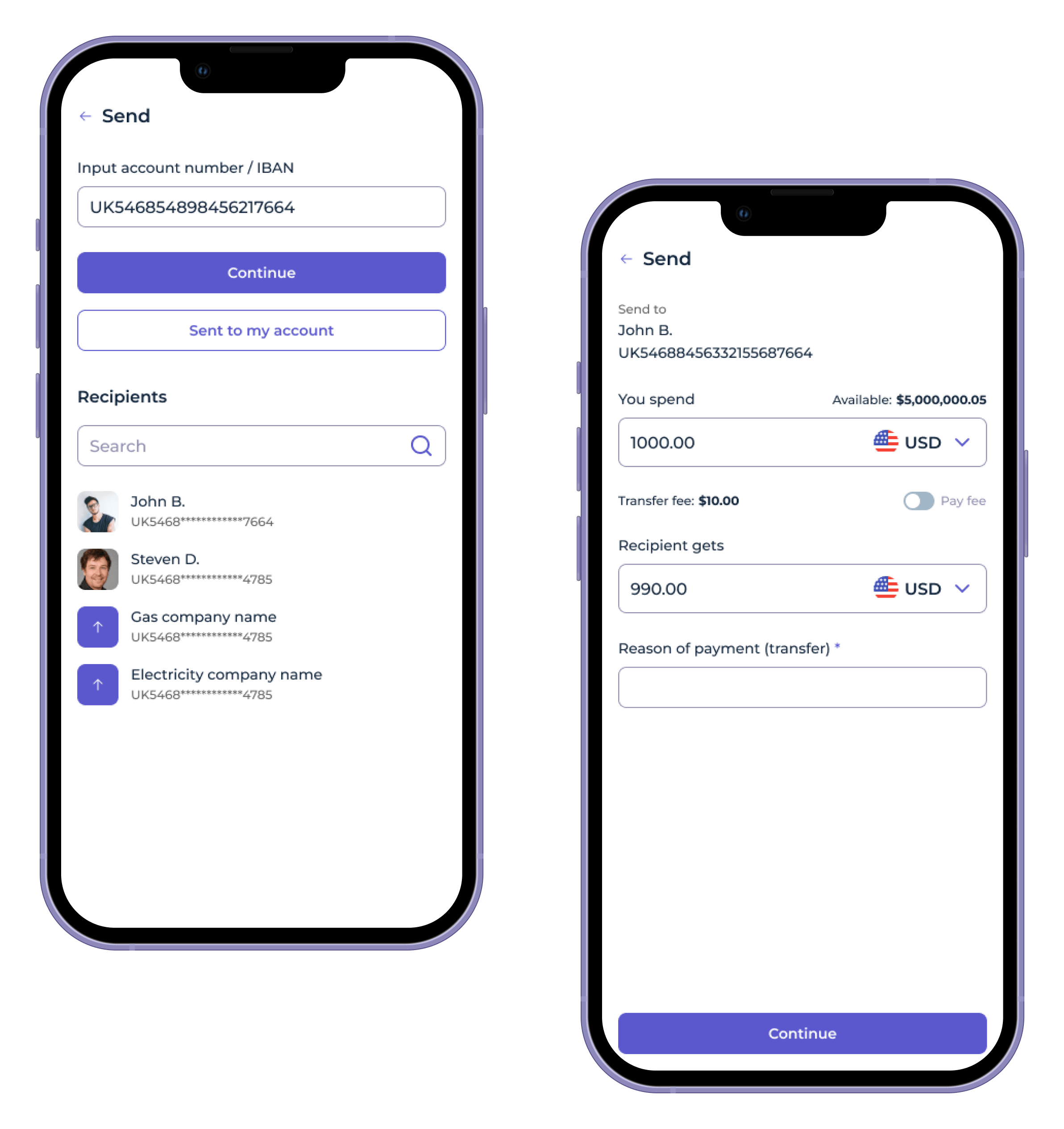

Card issuing is the process of creating and distributing payment cards, such as credit or debit cards, to end-users. This involves a series of steps to ensure the cards are securely produced, personalized, and activated for use. Card issuing allows individuals or businesses to access financial services, make electronic transactions, and conduct various monetary activities.

How does the card issuing system work?

Source: EY

Below we explain key steps of how to become a payment card issuer.

How to launch a card issuing program?

Initial planning and feasibility

This step is paramount for a successful card program launch and involves the definition of program objectives, where the specific goals, compliance considerations, and financial sustainability are crystallized.

You must also conduct market research to identify and segment the target audience, ensuring that the card program meets your customers’ needs. User experience, risk assessments, and alignment with regulatory requirements define the planning process.

That’s why this phase serves as a background for a card-issuing program that meets compliance standards and the demands of your target market.

Compliance and regulatory requirements

It is impossible to explore the journey of card program launch without an understanding of card issuing regulations. The FinTech sector, whether it involves credit, debit, or prepaid cards, is subject to various compliance and regulatory requirements to ensure security for cardholders.

The specific requirements can vary by country, and financial institutions must adhere to the regulations set forth by relevant regulatory bodies. Below we highlight the common regulatory aspects you need to know before becoming a debit card issuer.

PCI DSS

PCI DSS (Payment Card Industry Data Security Standard) is a set of security standards designed to ensure that all companies that accept, process, store, or transmit credit card information maintain a secure environment. Card issuers need to comply with these standards to protect sensitive cardholder data.

For example, a leading card issuing provider Marqeta offers customizable widgets that allow secure card activities in customer applications. Additionally, it provides a JavaScript library to display sensitive card data while minimizing data security compliance requirements.

SEPA cards framework

The SEPA Cards Framework (SCF) sets the guidelines that payment service providers, card systems, and other market participants must follow for card payments and cash withdrawals within the Single Euro Payments Area. The aim is to ensure that these transactions are processed as quickly, safely, and efficiently as they would be in the home country.

How to become a card issuer with SDK.finance?

SDK.finance provides a comprehensive solution for businesses looking to enhance their financial offerings.

Our Platform offers a specialized service for technical integration with Marqeta, including essential features for physical and virtual card issuance and management. It allows our clients to become a card issuer without having to go through the lengthy process of integrating with banks or card-issuing platforms.

SDK.finance clients can access the features available based on their unique requirements and agreements with Marqeta, whether through the source code license version of the SDK.finance Platform, or the PaaS one.

Therefore, our system acts as a facilitator, ensuring a swift and efficient integration process and enabling clients to take advantage of Marqeta’s full array of card-issuing capabilities.

How to start using Marqeta integration for SDK.finance clients?

Embarking on the journey of integrating Marqeta with SDK.finance for clients involves a structured and step-by-step approach.

- To get started with Marqeta, clients need to sign an agreement with a card-issuing provider, outlining the specific features and services they want to use. The flexibility of these features depends on the client’s needs and the agreements they make with Marqeta, whether related to the source code or cloud clients.

- The client receives essential credentials from Marqeta, granting access to both the Test and Production Environments. These credentials play a crucial role in establishing connectivity with the service provider.

- Once armed with the necessary access, clients proceed to configure provider connectivity settings within the SDK platform, ensuring seamless integration.

- This step is critical in ensuring a smooth integration between Marqeta and SDK.finance for clients. It involves configuring the gate product (this is the way we refer to it in our documentation ) within the SDK.finance platform, completing the setup process, and laying the foundation for a seamless integration. In this context, the “product” refers to the display of product cards within the SDK.finance system. A specific plan is necessary to determine how a card will be issued for the client, guided by the card scheme, such as choosing Visa. This plan is collaboratively agreed upon and issued by Marqeta, improving the clarity and efficiency of the integration process.

- The last steps involve setting up the system configuration file and defining the commission profile, specifying the provider and total commission for the “Issue card” operation in the settings. To ensure that customers can access the card issuing service, it is crucial to establish a fee for this operation within their contracts. This fee configuration typically comprises two components: the provider fee and the system fee.

Card design and branding

When it comes to designing and branding cards, Marqeta is a standout in the market due to its wide range of options and flexibility in card issuance branding. By working together, Marqeta and SDK.finance enable clients to take advantage of comprehensive branding options, but the extent of this capability is dependent on the specifics outlined in the client’s agreement with Marqeta.

The configuration of the card product, including the type of cards issued, is a critical aspect determined by the terms established between the client and the Marqeta. From a technical standpoint, SDK.finance supports all card branding options available, ensuring that the full spectrum of branding possibilities can be seamlessly integrated.

The success and richness of the card branding experience depend on the collaborative understanding and agreement between the client and Marqeta, facilitated by the robust support provided by SDK.finance in the integration process.

Activation

Card activation within the SDK.finance system is an effortless and efficient process that guarantees a quick and hassle-free experience for users. The entire process, from the initial setup to card activation, is designed to be completed within just 1-2 minutes.

Watch this video to explore the seamless process of card activation by SDK.finance`s users

Below is a breakdown of the process

1) System setup

The first step involves setting up the SDK.finance system, where users can initiate the process of creating their payment cards. The user-friendly interface and intuitive design of the system make it easy for individuals to navigate through the setup process.

2) E-wallet creation

Upon entering their accounts, users have the option to create an in-system eWallet. This digital wallet serves as the funding source for their new card. Creating an eWallet in the system is straightforward and adds to the user-friendly experience.

3) Top-up process

At this stage, we need to top up the wallet to pay for issuing the card (to make a top-up—whether for cards or wallets—an integration of card processing is necessary).

To activate and fund a new card, customers can effortlessly top up their eWallet using their existing debit card. This step is seamlessly integrated into the process, allowing users to complete the transaction swiftly and securely.

4) Card issuance and customization

Once the eWallet is topped up, users can proceed to issue their new card. SDK.finance offers a range of design options for users to choose from, allowing them to personalize their cards to align with their preferences and branding. Users can also add a nickname to their card, adding a personal touch to the overall experience.

5) Activation

The final step involves activating the newly issued card. With just a simple click on the “Activate the Card” button, users can swiftly activate their cards for immediate use.

6) Funding

Through integration, customers can easily add funds to their card with the top-up feature, which is fully supported by the system.

As a result of this streamlined process, the card becomes ready for use within minutes. Users gain instant access to view their transactions, customize settings, and review card details. SDK.finance’s commitment to efficiency and user satisfaction is evident in this expedited card activation process, making it a standout feature for individuals who prefer a swift and straightforward experience in managing their payment cards.

Technologies integration

The process of technology integration involves the use of the SDK.finance Platform to initiate the issuance of a card (either physical or virtual) through a front-end application, which can be either web or mobile. The front-end application utilizes API calls to create a Business Process within the SDK.finance system based on certain conditions. This Business Process triggers an integration service, which then makes requests (via REST API) to the service provider’s system to issue a card.

On the provider’s side, a user account and a card are created, with a selected schema and program that is agreed upon between the client and provider. The card is then linked to the user’s profile.

Marqeta, as the service provider, handles all necessary communication with the card network or bank that owns the card and provides the issue, according to the agreement and card product settings.

Once the card is created, the provider returns the card ID to the SDK.finance system, which then links the card to the initial user’s profile.

This allows the user to see the issued card within the SDK.finance system and access card management functions (such as de/activating, un/blocking, un/freezing, and setting limits). The user can also use the card to top up accounts or make payments, provided that a card payments provider has been configured in the system.

Security measures

The security measures are intricately linked to the card programs offered by Marqeta.

The company offers two distinct options for its clients to manage their card programs. The first option, “Powered By,” allows clients to independently use the platform by providing specific configuration elements. This option offers flexibility, letting businesses shape their card program as per their requirements while Marqeta provides expertise in configuring crucial resources.

The second option, “Managed By,” positions Marqeta as the Program Manager, taking charge of handling the program on behalf of the client. This full-service experience goes beyond assistance, as Marqeta configures the majority of critical resources necessary for the production environment. This option offers a comprehensive and hassle-free solution, allowing clients to focus on their core business while entrusting Marqeta with the intricacies of card program management.

Marqeta is a top card issuing provider and it considers security as its top priority. The company follows the latest hardware and software security best practices to ensure the safety of its customers. Marqeta has PCI DSS level 1 and SSAE-18 compliance certifications, which shows that it meets the highest standards of security.

Additionally, the company uses bank-grade encryption for PII, PCI, PIN data-in-transit, and data-at-rest to protect sensitive information. When communicating with Marqeta platform services, TLS 1.2 or higher is required to ensure secure communication.

Conclusion

The journey on how to launch a card issuing program has been made easier, thanks to the innovative solutions provided by SDK.finance and its integration with Marqeta.

As technology continues to shape the landscape of card programs, these key steps serve as a roadmap for businesses seeking to embark on this transformative journey. With a ready-to-use integration service app by SDK.finance becoming a credit card issuer is more accessible and efficient.