This future is already here, thanks to prepaid digital wallets. These revolutionary payment solutions are changing how we shop, travel, and socialize.

Prepaid digital wallets are revolutionizing finance, allowing users to load funds in advance for a wide range of transactions, whether in-store, online, or via mobile apps. This provides flexibility, security, and ease, making them an essential tool for the modern, cashless economy.

In this article, we’ll explore the rise of prepaid digital wallets, examine their growing influence across various industries, and highlight how businesses can benefit from launching these payment solutions.

Prepaid digital wallet market size

Globally, the prepaid digital wallet market is growing rapidly. Here are some key statistics and insights regarding its size and projected growth:

- The global market for prepaid cards is estimated at US$2.0 Trillion in 2023 and is projected to reach US$4.1 Trillion by 2030.

- It is expected to reach $7.5 trillion by 2027.

- Global digital wallet users are expected to reach 5.2 billion by 2026, representing over 60% of the global population.

These statistics highlight the rapid growth and increasing importance of prepaid digital wallets in the global payments landscape, driven by rising consumer adoption and the shift towards a cashless society.

What is a prepaid digital wallet?

A prepaid digital wallet is a type of electronic wallet that allows users to load funds in advance and use them for various transactions within a specific ecosystem or with participating merchants.

These prepaid solutions offer a controlled spending environment, making them popular for budgeting, gifting, and managing expenses without the need for a traditional bank account.

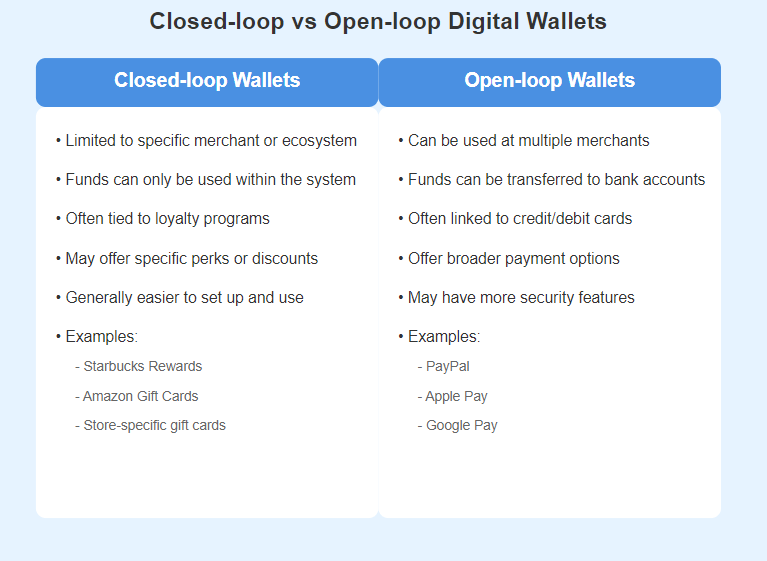

Prepaid wallets can be:

– closed-loop, where funds are restricted to a specific merchant or group of merchants,

– open-loop, where funds can be used across multiple platforms and locations, similar to debit or credit cards.

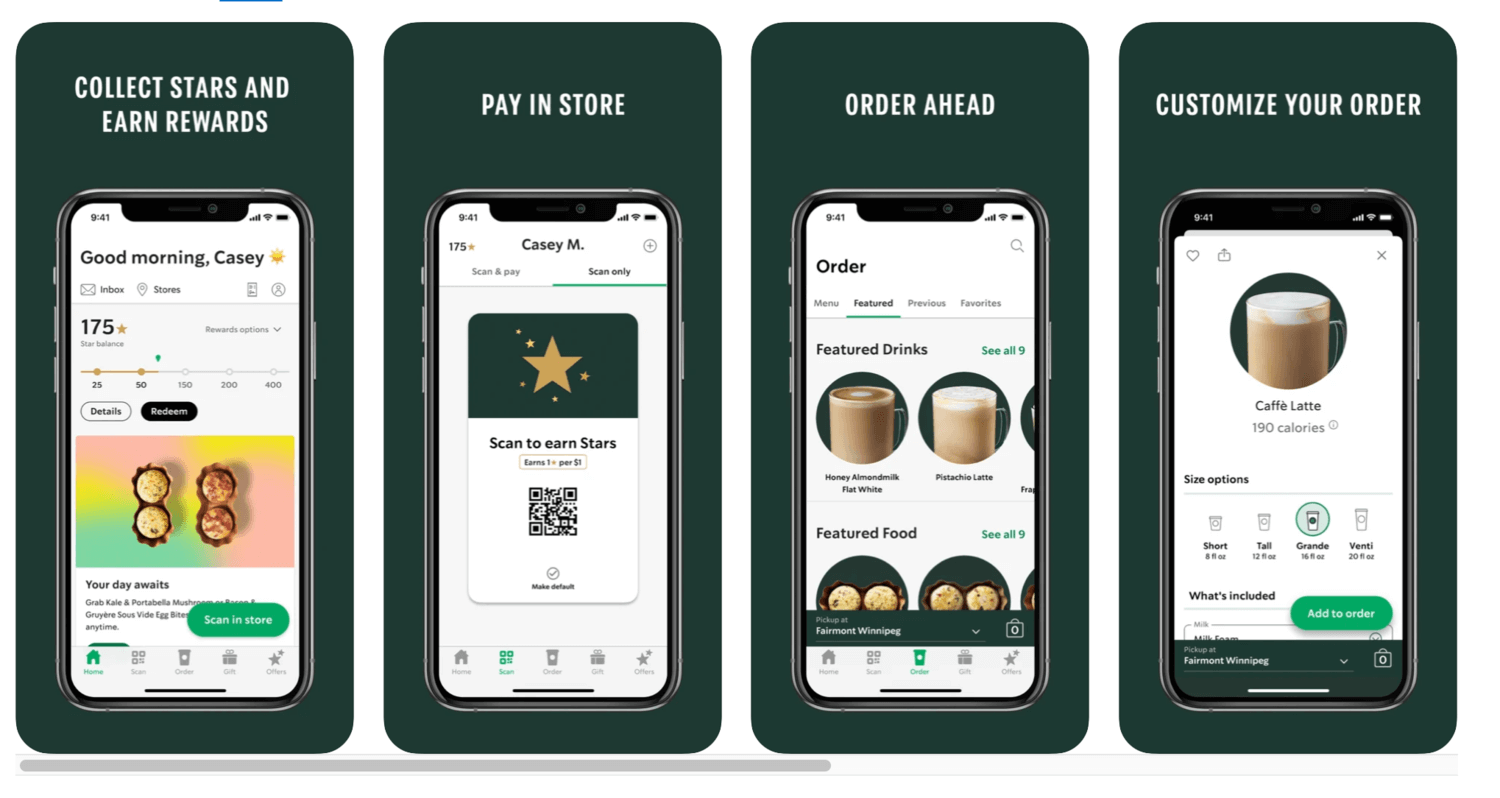

A classic example of a closed-loop prepaid solution, the Starbucks Card allows customers to load money onto the card and use it exclusively at Starbucks locations. It also integrates with the Starbucks app, offering rewards and special promotions.

What is the difference between digital and prepaid wallets?

Prepaid solutions, refer to a form of digital wallet enabling users to pre-load funds and use them for different transactions within a designated environment or with affiliated retailers.

Digital wallets vs. prepaid wallets comparison table:

| Feature | Digital wallets | Prepaid wallets |

| Funding source | Linked to bank accounts, credit/debit cards, or other financial accounts. | Funds must be loaded in advance, usually through cash, bank transfer, or another payment method. |

| Spending flexibility | Can be used for a wide range of transactions, including online purchases, in-store payments, peer-to-peer transfers, and more. | Typically limited to specific transactions within a closed-loop system (specific merchants) or open-loop system (wider acceptance, like a prepaid card). |

| Integrations | Often integrated with additional financial services, such as savings accounts, loans, and investment options. | Generally focused on transactions and payments, with fewer additional services. |

| Examples | Apple Pay, Google Wallet, PayPal, Samsung Pay. | Starbucks Card, Amazon Pay Gift Card, PayPal Prepaid Mastercard. |

| Reloadability | Automatically funded through linked accounts or cards. | Must be manually reloaded by the user, though some offer automatic top-up options. |

| Use cases | Broad use across various sectors, including retail, services, P2P transfers, and more. | Often used for budgeting, gifting, and controlled spending within specific environments. |

| Security | Iinclude encryption, biometric authentication, and tokenization for secure transactions. | Security features similar to digital wallets, but with the added security of limited spending based on pre-loaded funds. |

| User control | Control over multiple funding sources and can switch between them. | Control over the pre-loaded balance, with no access to external credit or debit sources. |

While digital and prepaid wallets both offer convenience for electronic transactions, digital wallets provide more financial flexibility and integration across multiple funding sources. On the other hand, prepaid wallets are focused on controlling spending within specific environments.

Get your prepaid digital wallet product launched months faster

Accelerate the development process with a ready-made SDK.finance Digital Wallet Software

Learn moreGrowing prepaid digital solution trend in various industries

The prepaid digital wallet market is experiencing significant growth across various industries, driven by the increasing adoption of digital payment solutions.

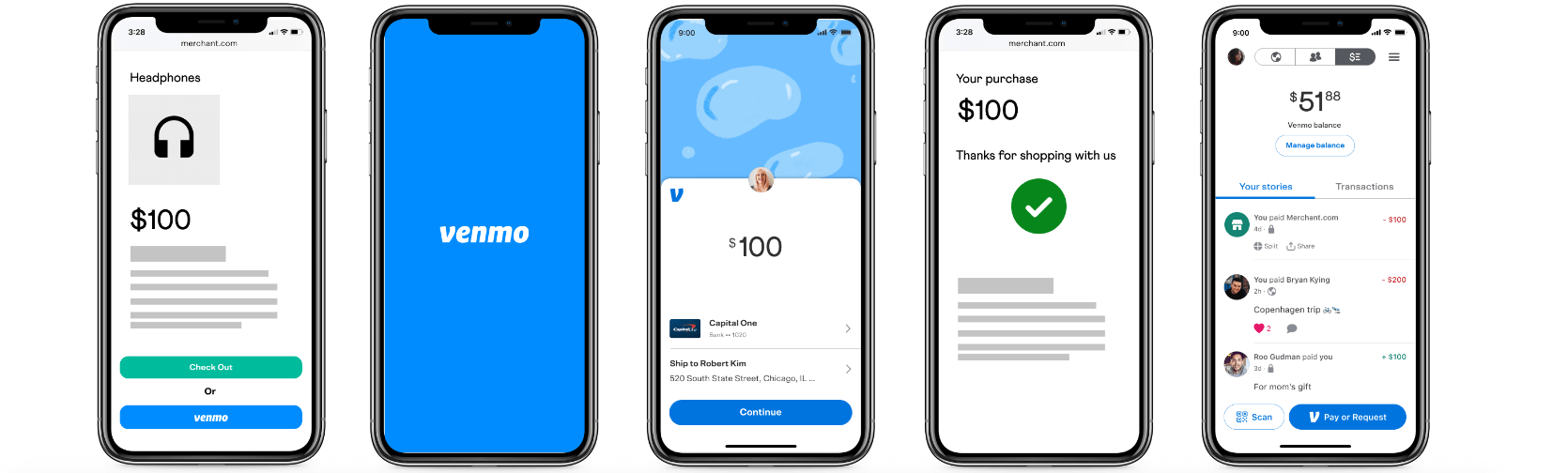

Retail: Apple Pay and Google Pay

Retailers are increasingly integrating digital wallets to enhance customer experience and streamline transactions.

For instance, many retailers now accept mobile payment options like Apple Pay and Google Pay, allowing customers to make purchases quickly and securely.

Source: Apple

Hospitality: Airbnb and Uber

The gig economy has transformed the hospitality industry by providing flexible staffing solutions. Businesses can hire gig workers for specific tasks, reducing the need for full-time employees and optimizing operational costs.

Digital platforms like Airbnb and Uber have integrated payment solutions that facilitate seamless transactions between service providers and customers.

Source: Medium

Finance: GCash and PayMaya

Prepaid digital wallets are becoming essential tools for financial inclusion, particularly for unbanked populations. They offer a way to access digital payments without needing a traditional bank account.

One notable example is the rise of prepaid digital wallets in the Philippines, where a significant portion of the population lacks access to traditional banking services. In 2021, around 51% of Filipino adults were unbanked, and to address this gap, prepaid digital wallets have emerged as a viable solution. Services like GCash and PayMaya have gained widespread adoption, with GCash alone boasting over 66 million registered users as of 2022.

Features of prepaid digital solutions

Prepaid digital solutions have become increasingly popular due to their convenience, flexibility, and security features. These solutions are designed to facilitate financial transactions without the need for traditional banking services.

Instant transfers

Users can enjoy instant transfers between accounts, making it easy to send money to friends or family or pay bills promptly. For instance, Cash App is a popular prepaid digital wallet that allows users to send and receive money instantly. The transfer is typically completed within seconds, making it ideal for splitting bills, paying for services, or sending gifts.

Bill payment options

Prepaid digital solutions often allow users to pay bills directly through the platform, eliminating the need for manual payments or visits to payment centers. An example of bill payment options in prepaid digital solutions is Venmo’s bill pay feature, which allows users to pay various bills directly through the app, such as utilities, rent, and credit card payments.

Rewards and cashback programs

Some prepaid digital solutions offer rewards programs or cashback incentives, providing additional benefits for users who make transactions through their services.

An example of a rewards and cashback program is the PayPal Cashback Mastercard. Users who make purchases with this prepaid digital solution earn 3% cash back on all transactions made with the card, which is automatically credited to their PayPal account.

Virtual and physical cards

Prepaid digital solutions often provide both virtual and physical cards. Virtual cards are ideal for online transactions, while physical cards can be used at point-of-sale terminals.

SDK.finance offers comprehensive card issuing services, leveraging Marqeta’s powerful platform for both virtual and physical cards. Using the API-first approach, SDK.finance delivers highly customizable card solutions, aligning with modern consumer expectations for flexibility, security, and control across various payment channels.

Launch your crypto-to-fiat app, in weeks

Build a robust crypto-to-fiat spending app on the SDK.finance Platform

Learn moreMobile wallet integration

Prepaid solutions integrate seamlessly with mobile wallets, allowing users to make payments directly from their smartphones or other mobile devices.

An example of mobile wallet integration is Apple Pay’s connection with prepaid cards. Users can add their prepaid cards, like the ones from PayPal or Green Dot, directly to their Apple Wallet. This allows them to make contactless payments using their iPhones or Apple Watches at supported point-of-sale terminals.

Benefits of prepaid digital solutions app for businesses

Prepaid digital solutions apps offer a range of advantages for both individuals and businesses. Here are some of the key benefits for financial institutions:

New revenue streams

Prepaid digital wallets can generate revenue through various fee structures, including per-transaction fees, monthly subscriptions, or tiered pricing based on usage. By the way, analyzing customer purchase history and preferences, wallets can recommend relevant products or services, driving additional sales.

Lower operating costs

Prepaid digital solutions can significantly reduce operational costs for businesses. A study by the Federal Reserve revealed that cash handling can account for a substantial 5-10% of transaction values. By switching to these digital solutions, businesses can streamline their operations and eliminate the expenses associated with cash management, check processing, and credit card fraud.

Faster transactions

Prepaid digital wallets enable instant payments and real-time fund transfers, accelerating transaction times. Unlike traditional methods like checks, which can take 2-3 business days to clear, digital payments are processed almost immediately.

Turn the first years of development into the first years of growing your revenue

Explore how our powerful API-driven neobank software can accelerate your launch

More detailsImproved customer experience

Customers can make contactless payments in-store or online using their mobile phones, which eliminates the need for physical cash or cards. According to a survey by Statista, 43% of global consumers used mobile payments at least once a week, indicating an increasing preference for digital payment options among customers.

Valuable data insights

By analyzing transaction patterns, businesses can anticipate future spending behavior and adjust inventory or promotional campaigns. According to McKinsey, businesses that use data-driven personalization can increase sales by 5-15% and boost marketing ROI by 10-20%. For instance, Uber uses spending data from its digital wallet to offer ride promotions based on customer activity.

Choosing between closed-loop and open-loop systems

When evaluating prepaid digital wallet systems, businesses must consider the pros and cons of different types of payment products: closed-loop and open-loop systems. For example, closed-loop systems, like those used by Starbucks or Walmart, offer enhanced control over transactions and greater customer engagement, but are limited to specific merchants or brands.

On the other hand, open-loop systems, such as those offered by Visa or Mastercard, provide broader usability across multiple merchants, offering more flexibility for users but often involve higher transaction fees and less control for businesses.

The difference between closed-loop and open-loop systems

Use cases vary by business type. For instance, closed-loop systems are ideal for brands that want to increase customer loyalty and keep transactions within their ecosystem, such as retail chains, hospitality, or entertainment venues.

Open-loop systems, on the other hand, work well for financial institutions or companies that need wide usability, like fintech startups offering payment solutions for diverse industries.

When considering scalability, businesses should assess their growth plans.

Closed-loop systems can be easily scaled for businesses with a loyal customer base, but may require significant customization to expand functionality. Open-loop systems offer immediate scalability but often require higher upfront investment and ongoing fees.

Using established solutions, like SDK.finance, allows businesses to leverage pre-built tools for scalability while maintaining customization capabilities. Platforms like SDK.finance enable companies to create tailored closed-loop wallet systems, offering seamless integration, secure transactions, and the flexibility to scale operations as the business grows. These platforms help businesses manage both customer engagement and transaction flows without the need for extensive in-house development.

Regulatory compliance for prepaid digital wallets

One of the most important aspects of developing a digital prepaid wallet is compliance. Companies that offer digital wallets must navigate a complex set of rules to protect consumers and ensure financial security.

KYC and AML requirements

First, to prevent fraud and money laundering, businesses must follow strict Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations. KYC involves verifying a user’s identity using documents like passports or driver’s licenses. AML laws require businesses to keep an eye on transactions for any suspicious activity. If they spot something fishy, they must report it to the authorities.

Data protection and privacy laws

Next, businesses must also comply with data protection and privacy laws, such as the General Data Protection Regulation (GDPR) in Europe or the California Consumer Privacy Act (CCPA) in the United States.

These regulations require businesses to handle customer data according to robust security measures, obtain consent for data collection, and provide transparency on how customer data is used.

PCI DSS compliance

Last but not least, prepaid digital wallets must also follow PCI DSS standards. These are security rules made to protect cardholders’ information when they pay. Businesses that handle card payments, whether with physical cards or digital wallets, need to follow these guidelines to stop data leaks and fraud.

Stay ahead in the remittance business with a ready-made FinTech Platform

With SDK.finance software you can implement your money transfer app vision faster

More infoCase studies: successful prepaid digital wallets

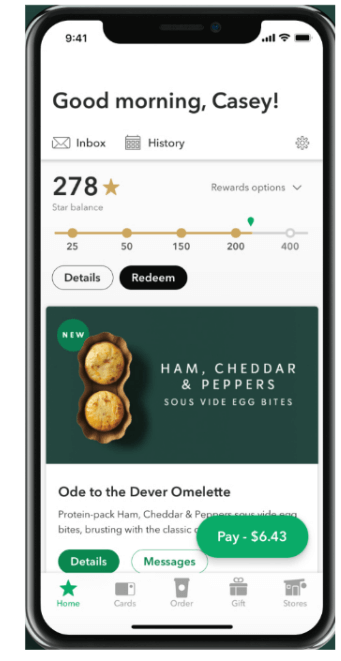

Retail: Starbucks rewards

The Starbucks Rewards Program is an excellent example of how a retail brand can use prepaid digital wallets to enhance customer engagement and loyalty. Customers can load funds into a prepaid wallet using the Starbucks mobile app, enabling them to make swift and smooth purchases either in-store or online. With each transaction, users earn Starbucks Stars, the program’s reward currency, which can be exchanged for free drinks, food items, or special offers.

Travel: Airline-specific wallets

In the travel industry, airline-specific wallets allow passengers to store funds, manage flight-related expenses, and even collect loyalty points or rewards all within one integrated platform.

For example, airlines like Delta Air Lines and Qatar Airways have developed their own digital wallets that enable customers to store funds, and manage payments for future flights, baggage fees, upgrades, and in-flight purchases. The wallet is tied directly to the customer’s account, making it easy to complete transactions without the hassle of entering payment details for every purchase.

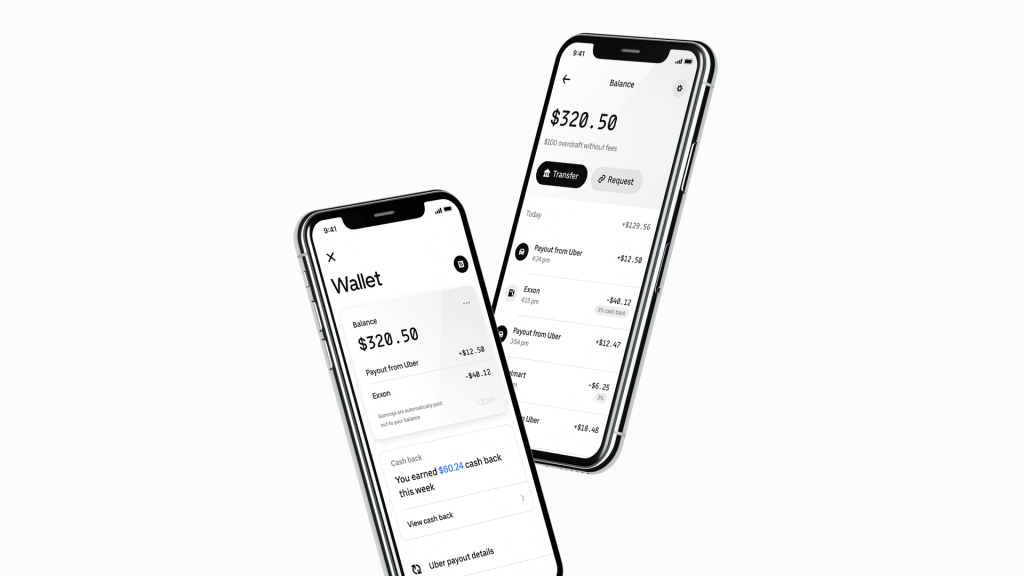

Gig economy: Uber driver wallet

Uber’s driver wallet has revolutionized the way drivers manage their earnings. The wallet allows drivers to easily track their income, expenses, and tax information. By providing a convenient and transparent financial solution, Uber has enhanced the driver experience and improved efficiency within the gig economy.

Expand your market with virtual and physical card issuing

Create virtual or physical cards faster via SDK.finance easy-to-use card issuance API

Read moreDeveloping the prepaid digital wallet solution

As businesses increasingly explore digital payment options, developing a prepaid digital wallet solution offers a strategic way to engage customers, streamline transactions, and unlock new revenue streams.

However, building such a system from scratch can be costly and time-consuming. To overcome these challenges, many companies turn to established solutions that provide the infrastructure needed to launch digital wallets quickly and efficiently.

For businesses looking for a ready-made solution, SDK.finance offers a flexible FinTech Platform for building prepaid digital wallets.

Key features of SDK.finance Platform:

User account management

- Registration and onboarding: We provide a simple and secure user registration process, including options for Know Your Customer (KYC) procedures.

- Multi-currency support: Our platform supports any urrencies to accommodate a global user base.

Payment and transaction processing

- P2P payments

- Merchant payments

- Bill payments and top-ups

- QR Code and contactless payments

- Transaction history

Security features

- Two-factor authentication (2FA)

- Fraud detection and prevention

- Data encryption

- Biometric authentication

Customer support tools

- In-app support

- Notifications and alerts

SDK.finance offers a highly scalable platform with a capacity of 2,700 transactions per second (TPS), capable of handling over 233 million daily transactions, ensuring seamless growth from 1,000 to 1 billion+ monthly transactions. This scalability guarantees consistent performance as your business expands, allowing you to focus on increasing transaction volumes without concern for system limitations.

The platform’s modular architecture allows businesses to customize their solution by selecting only the necessary features, such as payments, rewards, or advanced financial services. With over 400 API endpoints, SDK.finance ensures seamless integration with third-party systems, making it easy to expand and adapt your prepaid digital wallet as your business needs evolve.