The global remittance market was estimated to be worth $701 billion in 2020 and is expected to reach $1,227 billion by 2030, representing a CAGR of 5.7% between 2021 and 2030. Moreover, rising number of cross-border transactions and increasing usage of mobile payment options are expected to drive the market growth over the forecast period. From 1998 to 2018, the global average rate for remittances was 7.14%, reaching more than 700,000 transactions in 2020, according to Finder research. Based on Statista source, the value of remittances will increase to $750 billion in 2023. Source: Finder In addition, the rising penetration of mobile devices in recent years has encouraged the adoption of digital technologies in remittance services and cross-border payments worldwide. Customers around the world are also turning to digital remittance services as they help reduce remittance time and costs. In addition, money transfer services provide a high level of privacy and protection for consumers’ money. Source: Statista Market Insights The international money transfer market has grown significantly at a CAGR of 10.4% since 2000, with $530 billion being transferred each year. Digital remittance transactions are estimated to exceed $390 billion in 2022, and the adoption of platforms integrated with blockchain technology is expected to drive growth. On processed international transfers and remittances as of 2022, either incoming or outgoing(in billion U.S. dollars) Source: Statista Market Insights With such huge amounts of money moving across borders, money transfer services are beneficial for both customers and businesses. By adopting digital technologies for cross-border money transactions, remittance companies are increasing their revenues as the financial industry continues to grow. So, a money transfer is a broader term that includes money remittance, as well as other types of financial transactions, such as sending money from one bank account to another or transferring ownership of assets from one person to another. Many companies start the remittance business without background research or expertise in this industry. In fact, it is crucial to be well versed in the money transfer and payment industry, as there are a number of restrictions and regulations in this field. Therefore, we discover the most important points you should know before starting a remittance business. Launch your payment project in record time The money transfer market is an ecosystem made up of various players that are responsible for different functions. As a new money transfer provider, you need to clarify the responsibilities of these participants and understand their role in the payments ecosystem. The key players in the money transfer system are listed below: In most countries, a license is required to operate a money transfer business. Therefore, it is important to research the licensing process before launching a remittance business. To enter the money transfer industry, you need to contact regulatory agencies and apply for a license for your type of business. By obtaining the necessary permits and licenses, you can avoid potential legal issues and operate a transparent money service business. There are some differences in obtaining a money remittance business license depending on the region in which you will be operating. The operation of a money transfer business requires compliance with federal, state, and local regulations governing this service. In the United States money transmitter is a part of a larger group of Money Service Businesses. To ensure that your company is not involved in money laundering, you must file a FinCEN Form 107 with the U.S. Treasury Department’s Financial Crimes Enforcement Network (FinCEN). It takes 180 days to establish the business under the Bank Secrecy Act, which controls money transfer services. New York State, for example, provides a complete checklist for obtaining a money transfer license. This licensing can be expensive and time-consuming. According to Faisal Khan’s research, it can cost around $1 million and take about two years to obtain a state license. If you want to become a money transfer operator in the UK and offer services such as sending and receiving money in and out of the country, you need to get the Payment Institution license. Depending on the amount of revenue your business generates, there are two types of Payments Institution (PI) licenses: Small Payments Institution (SPI) or Authorized Payment Institution (API). If your average monthly revenue is less than 3 million euros, you need to register as an SPI; if it is more than 3 million euros per month, you have to work as an API. The fees for the licenses are £500 for SPI and £1500 or £5000 for API, depending on the services offered. You will also need to sign the FCA Connect Platform for processing all license applications and related matters, and provide the Firm Reference Number (FRN) and Individual Reference Number (IRN). To start a money transfer business in Europe and beyond, you need an EMI (E-Money Institution) license. To obtain this license, you must meet the following requirements: an operational presence in Europe (an office and local staff); financial and non-financial resources to manage and operate the EMI; and capital of EUR 350,000 available in a bank account in the country where the EMI applies for the license. A money transfer license in the UAE is mandatory if you want to become a money transfer company in the country. With this license, businesses can offer currency exchange and money transfer services. The Central Bank UAE, ADGM (Abu Dhabi Global Market) and DIFC (Dubai International Financial Center) are three different licensing authorities, and each of them has its own rules. For instance, ADGM requires that you submit your application in accordance with the Financial Services Regulatory Authority (FSRA) guidelines, and you must meet with FSRA representatives or hold a conference call. In general, you need to have a business structure, financial resources, and internal control systems such as audit, AML compliance program, and KYC. Each of these institutions will audit your company according to the requirements: monitoring systems, availability of resources and others. It is prohibited to conduct money transfer business in the Kingdom of Saudi Arabia without a valid license issued by SAMA. In order to obtain a license from SAMA, the company’s paid-up capital must be at least two million (2,000,000) riyals. The founder of the money transfer company must also be older than 25 years and must not have violated any financial or banking laws in the UAE or outside the country. The complete list of requirements is available here. Ready backend, APIs, and integrations To speed up your time to market and save time and resources on development, you can find a software partner with experienced team. This company can help you start a money transfer business by providing the payment system software for you to build your product upon. To choose the right software solution, analyze its functional capabilities, especially in terms of AML and KYC requirements. SDK.finance is a fintech software vendor offering money transfer software that can help you launch a money transfer business or develop a remittance app. Below is a table of key features for a remittance app and their availability through the SDK.finance platform. Watch the SDK.finance Platform’s demo video to explore how you can simplify transaction management and ensure financial compliance with our powerful FinTech Platform: Numerous banks around the world are focusing on integrating technology into their remittance online platforms to enable faster and more seamless transfer. In addition, banks are increasingly turning to digital innovation to gain a competitive edge over other rivals. The increasing shift towards digitalization in the cross-border money transfer industry is also expected to drive the growth of the segment over the next decade. To start a remittance business you need to have a license and a reliable payment system, but software development is a complex process that requires a huge amount of resources. You can find the right money transfer software partner to accelerate the development of the payment product and meet your customers financial needs. The international money transfer industry overview

Global money transfer inflows (US$ million) over time

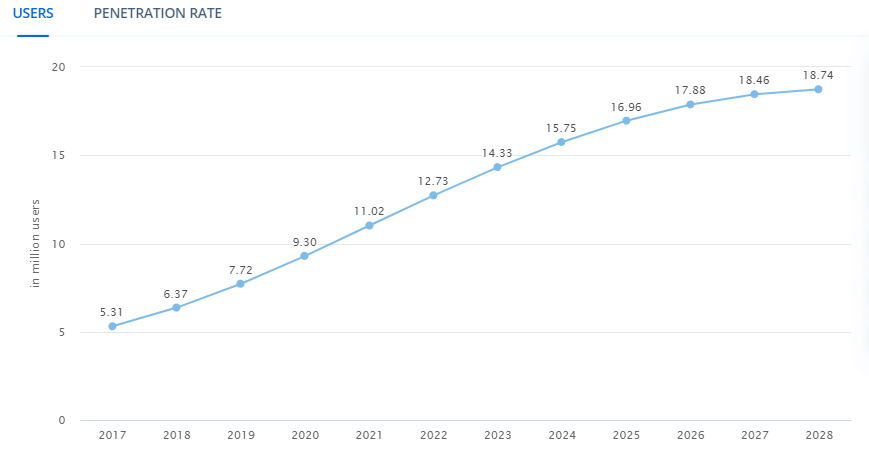

Money transfer number of users in millions

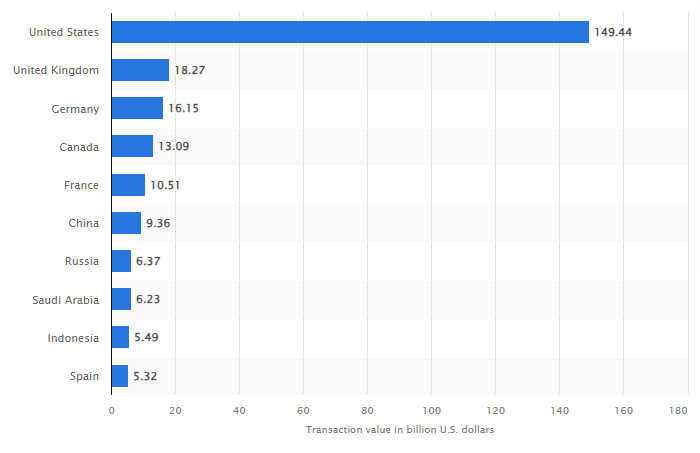

Leading countries in the world with the highest transaction value

Licensing and the main participants in remittance business

Money transfer and remittance: definitions and differences

What is money transfer?

The term money transfer refers to any electronic transfer of funds from one bank account to another.

What is money remittance?

Actually, money remittance is simply an amount of money transferred or sent from one party in one country to another party overseas. These money transfers can be made by customers to family and friends abroad, settle a supplier in another country, or for international business money transfers.

Participants of the money transfer process

Money transfer player

The role in remittance system

Sender, remitter

The individual who sends the remittance

Beneficiary

The person who receives the remittance money.

Sender’s bank

The bank used by the sender to transfer the amount of money. It can be a physical bank, an online bank, a mobile bank or an e-wallet.

Beneficiary’s bank

The beneficiary can access the funds through their bank account. The beneficiary’s bank is used to receive the sender`s money.

Money Transfer Operator (MTOs)

Money Transfer Operators, or MTOs are the authorized entities that facilitate the money transfer process.

Payment processor

The payment processor is used by an MTO to conduct transactions when payment instruments such as ACH, debit/credit cards, or other platforms like PayPal are used.

Payment network

MTOs can route the remittance transfer through different payment networks, including a third-party network to settle transactions in regions where the MTO is not directly integrated.

Transmitter platform

Transmitter platform is the correspondent banking or online remittance software used by the MTO to handle all of its money transfer activities. One such remittance software is the Money Transfer Application, which not only includes everything an MTO needs for its operations, but also has simple accounting and tracking functions.

ID Verification (KYC)

A third-party service may be used to authenticate and verify the IDs submitted by the submitting MTO as part of the onboarding process.

Types of licenses for remittance business

Money transmitter license in the USA

Money transfer license in the UK

Money service business in Europe

Money transfer services in UAE

Money service business in Kingdom of Saudi Arabia

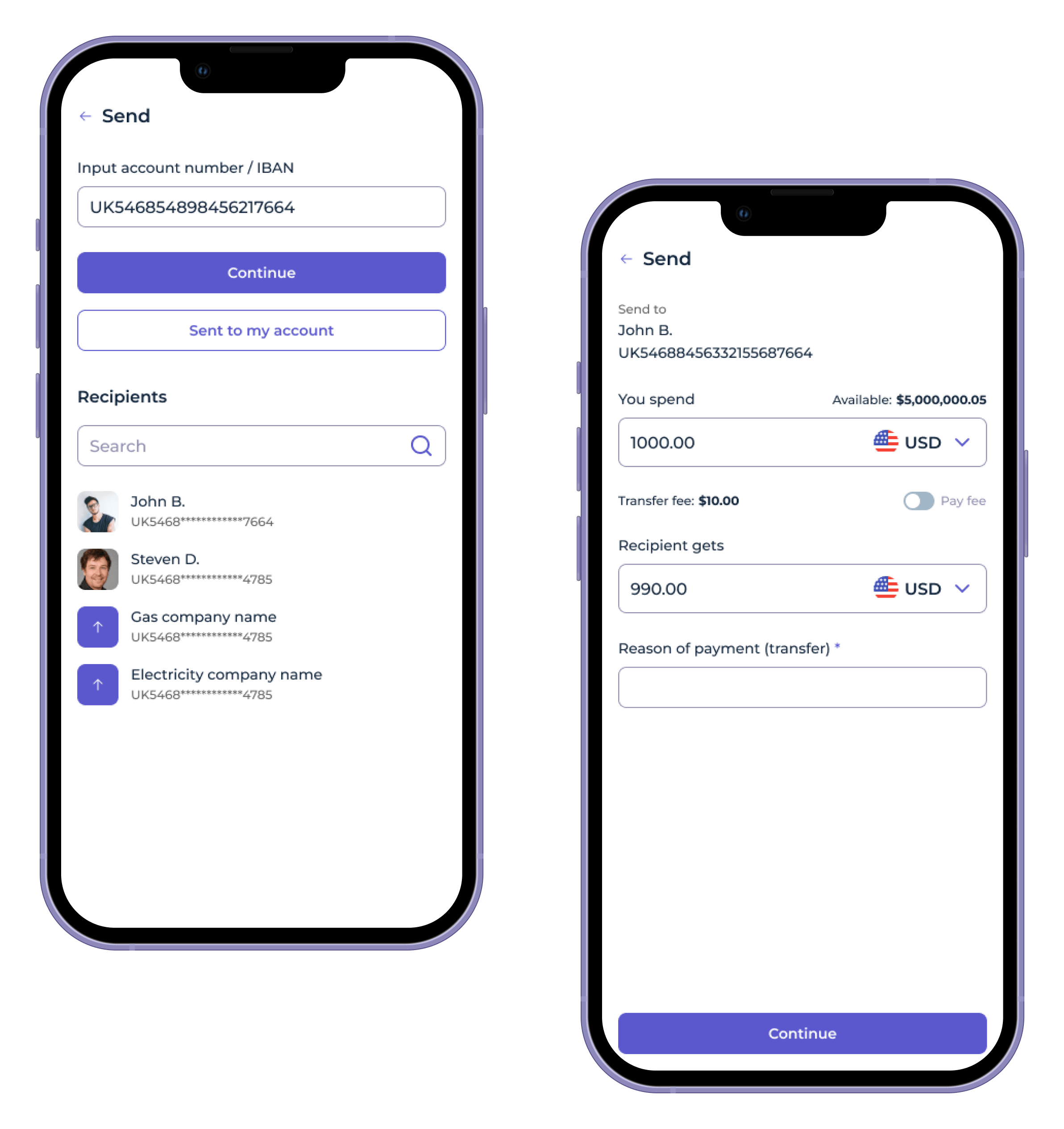

Developing the payment software

Money transfer service feature

SDK.finance fintech platform

Two-factor authorization (2FA)

Available

Online ID check (KYC)

APIs for manual approval and for integration with third-party KYC services

E-wallets

Yes, multiple wallets in different currencies can be created

Bill payments

Available through integrations with the vendors via API

Expense tracking

Yes, spending by categories, transactions on the map

Transaction notifications

Email and SMS notifications APIs

P2P transfers

Available out of the box

International remittance

APIs for integration available

Currency exchange

Available between a user’s accounts

Multilingual interface

APIs for integration available

Support

APIs for integration available

Integrations

The product is integration-ready with 400+ APIs, but no out-of-the-box integrations available

Conclusion

Fast-track your money transfer system launch

Launch your digital wallet app in record time