The coronavirus pandemic brought an end to a decade-long window of opportunity for banks. Most industry incumbents did not use the bull market and rich returns to prepare their businesses for a looming downturn. In many cases, banks did not adapt their business models and adopt technology that would allow them to sustain what is shaping up to be a considerable period of zero-interest rates.

As margins and revenues continue to shrink, banks will need to find ways to preserve capital and rebuild profits. Credit losses and a muted economic recovery will be a profound challenge for banks and banking systems. Depending on the recovery pace, $1.5 trillion to $4.7 trillion in cumulative revenue could be lost between 2020 and 2024.

McKinsey expects global banking ROEs not to return to pre-crisis levels for at least five years.

Source: McKinsey Global Banking Annual Review 2020

As a core banking software provider, we devote a lot of time and resources to researching how global changes impact our clients and the industry. At SDK.finance, we believe that understanding how disruptive trends affect the world is key to developing modern banking platforms and future-proofing our products.

Here are the three key takeaways we got from reading the new report.

Strengthen the technological foundation

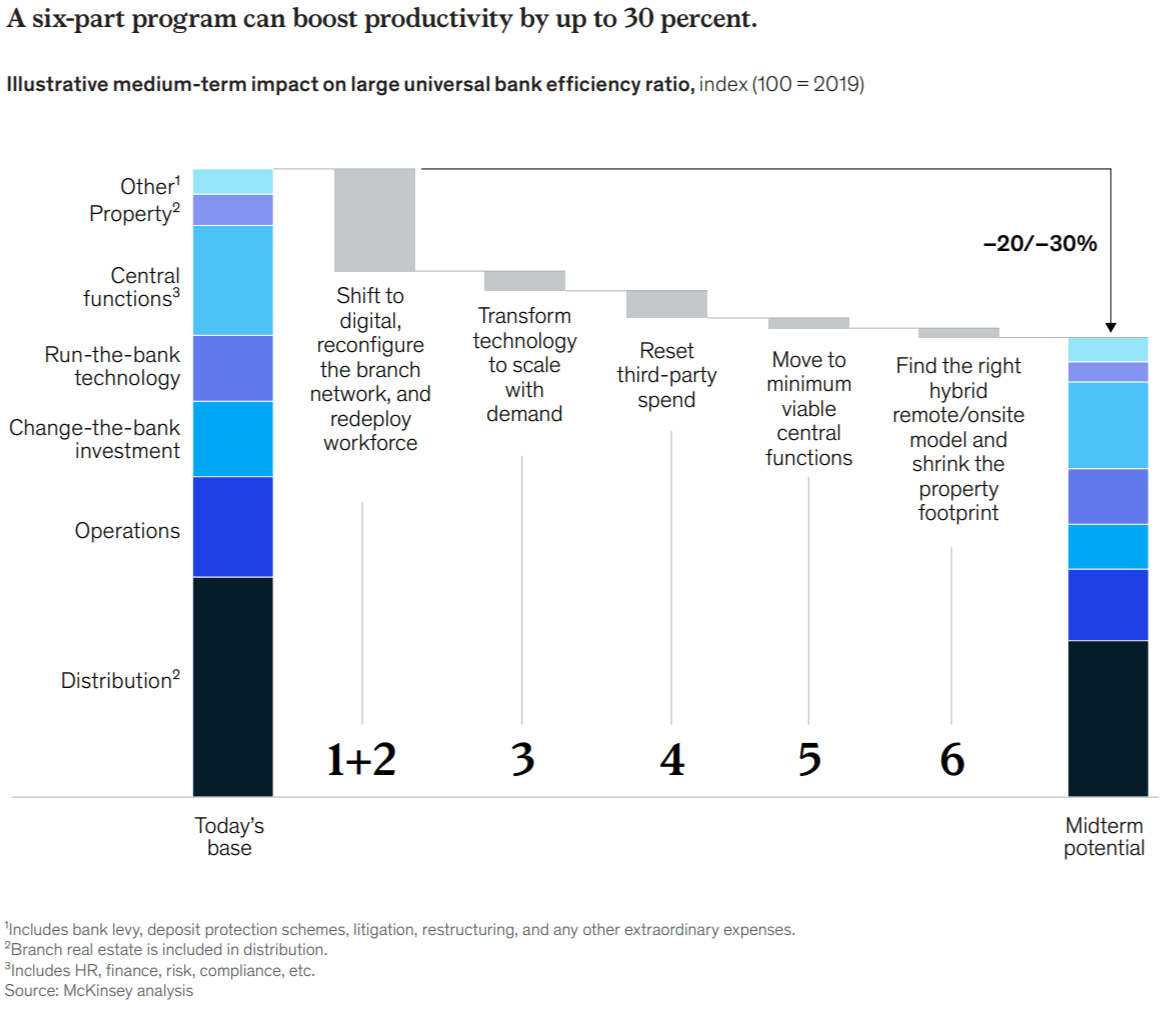

During the 2008 crisis, banks that reacted quickly and decisively were much better off than those that ignored or delayed important decisions. Banks that capitalize on this lesson can overcome the current downturn and come out stronger on the other side. McKinsey outlines three levers that banks can pull: increase revenues, manage costs, and better manage their equity capital. Resolute and timely action can improve efficiency by 20%-30% if banks dedicate themselves to continuous improvement instead of one-and-done programs.

Market-ready digital retail bank solution

Learn more

Source: 2020 Mckinsey’s Global Banking Annual Review

The demand for cash has fallen by 20-40% in most markets over the past year. Decreasing the use of cash and checks, core transactions for branches, is why banks need to accelerate the shift to digital banking platforms. As customer preferences shift towards digital channels and contactless payments, banks that invest in maintaining legacy infrastructure will see their costs balloon and responsiveness decrease.

To this day, less than 10% of an average bank’s technology expenses increase value-added business functionality. As the pandemic transforms customer journeys and demand for digital banking soars, banks need to radically reform the traditional IT function by shifting to platform-oriented architecture. Modern core banking platforms work across borders and products, providing access to real-time data flow and critical analytics.

Reinvent the business model

The expectation of a prolonged period of near-zero interest rates for years to come is forcing banks to reevaluate their business models. With a history of strong reliance on interest income and models built on risk intermediation, banks are now threatened by financial services intermediating services for fees, such as payment networks. 2020 is the first time the market cap of the largest three payments companies worldwide surpassed that of the three largest banks.

FinTechs and technology platforms capturing incumbents’ market share is another critical challenge for banks. Instead of relying on interest income to succeed in financial services, these tech challengers often thrive on origination fees or debit interchange, leaving interest rate risk and income to their partner banks. FinTechs drive engagement using seamless customer experiences, innovative products, and attractive rates on platforms that gather and monetize customer data.

Adopt the challenger playbook

As the threat of disintermediation by FinTech technology in a low-rate world becomes more real, banks cannot afford to forego new digital ideas. Leading banks are already taking on the best performing strategies of their digital challengers. In the past decade, banks that created internal digital bank spin-offs optimized revenue and reduced operating costs by up to 70%.

This approach allows banks to test concepts at lower risk before moving parts of the legacy business to the new system. Notable examples include Goldman Sachs’ Marcus, Bó by RBS, and State Bank of India’s YONO that acquired more than 26 million customers and broke even within 18 months.

Unconstrained by legacy technology constraints, banks can dramatically lower cost to serve and acquire customers by expanding digital-only services. Modern banking core platforms also open up the capability to partner and embed services in other ecosystems, capitalizing on the competition’s seamless digital experiences.

Banks have kept the financial system operating well in the first phases of the downturn. Now they need to concentrate on opportunities and productivity improvements available to restore and sustain livelihoods worldwide.

SDK.finance enables banks and financial institutions to build next-generation financial products with its core banking platform.

Contact the SDK.finance team directly to learn more about what type of banking software will be perfect for your business needs.