Neobanks are popular substitutions for traditional banks. Businesses create neobanking solutions for retail and corporate clients. For both these groups, the software solution should be agile, simple, and comfortable to use.

This article is about how to start a neobank development on your own, what should you know before you launch the neobank and how much do you need to do this. Our company develops retail and corporate solutions of its own. So, if you want to see the product features of a modern successful core for a neobank service, read more on our digital retail banking software page.

Create your digital banking solution in weeks

Talk to Our TeamWhat is a neobank?

To check if we are on the same page, let’s define what neobank is. When you are building your neobank, it means your product has no physical branches. It offers access through a mobile app, and (or) online banking. Neobanks enable customers to manage their finances directly, order new products, and receive support 24/7 with just a few taps irrespective of where they are. Neobanks and challenger banks tend to offer lower fees than their competitors because they save on digital banking, overhead, and branch costs. So, when someone launches a neobanking start-up, it means optioning the aggressive scaling. The competitive edge is to funnel money into blitz marketing, offline and online user acquisition, and tempting price plans for newcomers.

Create your digital banking solution in weeks

Talk to Our TeamWays to set up a neobank

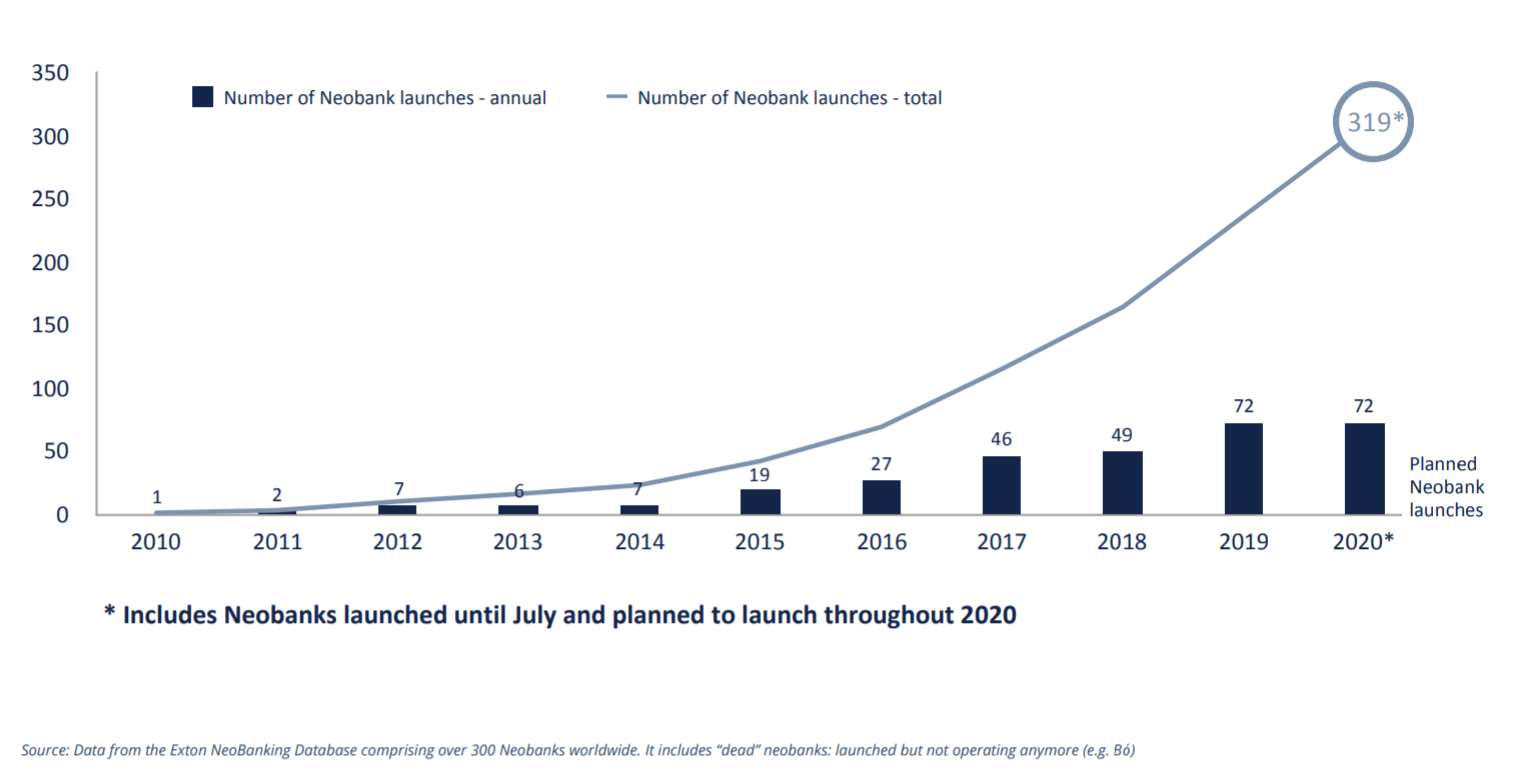

Source: Exton Consulting

As FinTech startups, neobanks need to offer an entirely new level of banking services to stand out and succeed. Every process and operation needs to be 100% digital and accessible on a smartphone or online without delay. Getting to that point requires a powerful digital neobanking system, a highly dedicated team, a strong vision, and modern tech components, such as artificial intelligence, risk assessment tools, and fraud detection to protect customer data. Below are three main ways how to build a neobank.

Create your digital banking solution in weeks

Talk to Our TeamBuilding an independent neobank

Independent neobanks that start from scratch need to get a virtual banking license to conduct business. After that, the neobank can operate without physical branches and offices. In most cases, independent solutions are centered on specific services rather than full-scale banking products. They bet on excellent customer service and a user-oriented experience to win customers through personalized experiences and attractive returns.

Revolut, for example, has made it incredibly easy to join – anyone can open an account in less than 60 seconds with free secondary accounts that hold money in one of 30 currencies. You can then use a Revolut card to spend any of your currencies, making it a whole lot easier to travel and spend abroad. Revolut will automatically convert your primary currency at the interbank FX rate without fees to make up the difference when you tap your card, saving money on every transaction.

Overview of live neobanks worldwide

Source: Exton Consulting

Building your own neobank from scratch or launching on a prebuilt solution?

Starting the neobank is about money. Backing our calculations on the number of clients our SDK.finance team has been in touch with, you need $5 million and more to set up a neobank, design the frontend and create a marketing funnel. If you have a great idea of how to cut the costs on clients’ acquisition and remarketing, you still face 2-3 years of software product development. Someone may grasp your idea, launch a neobank and go to the market far quicker than you. However, that is not the biggest issue.

When you decide to build your neobank from scratch, you hire a development team and fund them for the next three years. For a simple calculation, go to your regional IT vacancies aggregator, pick up the average salary per month for the developer and multiply it by 12. Then, multiply this amount by 20 or 30 for the number of developers working daily on your solution. So, you commit yourself to 3 years of production without a dollar of revenue, cause how will you provide P2P, get a banking license or comply with KYC requirements when you have no platform to onboard your clients?

We believe there is a shortcut for those willing to create a neobank. You can buy a software for your neobank for business or for clients. Many software development companies work on the best solutions opened for integrations with top-class vendors in KYC, CRM, and AI/ML niches. You can benefit from the product designed like the best neobanks of the market and muscle it up with your monetization idea, while it is still hot.

Neobanking software is more flexible, allowing banks to add and expand functions faster than traditional systems. Digital banks rely on the advanced process automation, web-based services, and APIs to provide banks and customers with a high level of cost-effectiveness, security, and flexibility. Neobanking startups now work on digital banking solutions that track customers’ journeys, generate real-time data streams, and accelerate critical analysis for better decision-making.

Open a subsidiary of a traditional bank

New technologies, customer preferences, and device changes constantly put pressure on traditional bank. Incumbents understand that they need to keep up with the times to retain their customers. However, rapid change is usually impossible due to the growing gap between the current level of technology and their large-scale enterprise systems. One solution is to create a spin-off neobank where the parent bank assumes the regulatory requirements. On the one hand, the parent company undertakes new risks, but on the other, the subsidiary can provide a broader range of banking and lending products, such as car loans, mortgages, etc. So, you start a neobank development for the existing audience of your company.

One of the best examples of a subsidiary neobank development is the Hello Bank! by BNP Paribas. With 3 million customers in several European countries, its broad user base has access to easy savings, preferential loans, and appealing cashback for purchases in various stores. In addition to traditional services, the bank also provides brokerage and insurance tools.

Build a neobank as a subsidiary of a tech company

The latest participants in the financial market are the new influential banks developed by the tech giants such as Google, Apple, Amazon, and Baidu. Besides enormous client bases, these companies excel in the digital world and have virtually unlimited resources. They can easily lower their prices and capture new markets, making it difficult for ordinary banks to deal with with tech-savvy competitors because they cannot match the reductions in prices of financial services. However, there is a chance. While these tech giants create neobanks from scratch, you can bring up a simple but highly profitable idea and mussel it up with a prebuilt banking core you integrate into your challenger bank.

One of the most popular neobanks in China, MYBank by Alibaba, caters to 35 million users and SMEs. The bank focuses on small personal loans and business credits. In less than three minutes, anyone can apply for a loan on a smartphone and wait less than one second to receive approval with zero human intervention.

What to consider before opening a digital bank?

It is hard to overstate the importance of technology for a digital bank. Starting neobank development from scratch requires significant investments and involves a great deal of uncertainty but provides unmatched control and flexibility over the platform. Partnering with an experienced technology provider offers a ready-made basis for establishing financial products and services without the need for large capital investments.

Neobanking software vendor SDK.finance provides a ready-to-go technological solution to start a neobank in the shortest amount of time. It takes about 2 years to develop software from scratch. SDK.finance solution reduces the time to market to several months.

SDK.finance platform is available for purchase as software with the source code license, which gives you independence from the vendor

Learn more about SDK.finance software solution for neobanks.

Why are UK consumers turning to neobanks?

Source: RFi Research

The financial industry is highly regulated to protect consumers as well as businesses. The regulatory environment needs to be researched and thoroughly evaluated for every country of operation as the ability to ensure deposits, for example, can be a decisive factor for consumers.

Aside from envisioning the neobank that will keep customers engaged and satisfied, it’s important to consider unique features and offerings because there’s a race to get a sufficient number of people to join. For a neobank to be profitable, it needs to build a large enough customer base, which means persuading a large number of customers to switch accounts from other financial institutions. This is notoriously difficult as it takes a time most neobanks don’t have in abundance.

Create your digital banking solution in weeks

Talk to Our TeamNeobank business challenges

Blurred differentiators

Neobanks have tried to differentiate themselves by offering very distinctive features not widely available among their high-street competitors. Neobanks were one of the first to provide app-based functions such as card freezing and spending classification. These and many other functions are now becoming widespread throughout the industry. More and more traditional banks provide good online banking services on top of their physical presence, diminishing the differentiators and making the market more crowded.

Racing against time

Neobanks clearly believe in a path to long-term profitability. Achieving this goal requires them to maintain agility and speed of innovation while actively pursuing new customers in an already crowded market with traditional banks rolling out their own neobanks. One solution is to sacrifice profitability to build a large customer base with competitive pricing, little to no ATM fees, and above-average savings interest. Although incumbents may lack the agility of new banks, they far surpass them in terms of the level of resources that can be invested in these initiatives.

Source: Insiderintelligence.com

Regulatory purgatory

Regulatory changes are undermining the unique value offerings of neobanks. Although highly beneficial for the industry as a whole, some regulatory initiatives diminish the first-mover advantages by forcing the competition to catch up. For example, Starling Bank’s API enabled external money management services to securely connect to the bank before the Open Banking initiative launched in 2018. On the other end of the spectrum, bureaucratic banking license processes geared towards traditional banking are still hindering progress with long paper trails and blanket requirements that do not apply to neobanking.

How to prevent a neobank failure

To reach profitability, neobanks need to find a way to stay ahead by continuing to innovate. They need to relentlessly identify, build, and introduce new features that customers want. The technical infrastructure needs to continue to provide a platform that truly supports scalability and innovation and stay away from the legacy technology challenges that have encumbered the progress of traditional banks.

Neobanks have immense potential, and the rising mobile and Internet penetration rates have created a suitable infrastructure for their booming development process. The increase in the use and trust of artificial intelligence and blockchain will drive the growth of new banks and may lead to a fundamental change in the banking industry. However, pressure from competition and the mature banking industry is a serious challenge that should be dealt with cautiously.

Business model and monetization strategies for neobanks

One of the key aspects of starting a neobank is developing a sustainable and profitable business model. Neobanks typically rely on various revenue streams to generate income and sustain their operations. Here are some common business models and monetization strategies employed by neobanks:

Subscription fees

Neobanks may charge customers a monthly or annual subscription fee for access to their banking services. This can include basic banking features such as account management, payments, and transfers, as well as premium features like higher transaction limits, enhanced security, and personalized customer support. Neobanks need to carefully consider the pricing and value proposition to ensure that customers see the subscription fee as justified.

Transaction fees

Neobanks may charge customers transaction fees for certain types of transactions, such as international money transfers, expedited payments, or additional services beyond the basic banking features. Transaction fees can be based on a percentage of the transaction amount or a flat fee. Neobanks need to carefully consider the transaction fees to strike the right balance between generating revenue and maintaining customer affordability.

Watch SDK.finance Platform demo video to explore how to maximize your revenue with our FinTech solution. This video showcases real-life scenarios demonstrating the power of the Vendor Management section for CROs within the SDK.finance backoffice:

Interchange fees

Neobanks can earn interchange fees from card transactions when customers use their neobank-issued debit or credit cards for purchases. Interchange fees are typically a percentage of the transaction amount and are paid by the merchant’s bank to the neobank for processing the transaction. Neobanks need to establish partnerships with card networks and payment processors to earn interchange fees.

Lending

Neobanks can generate revenue by offering lending products such as personal loans, small business loans, or credit lines to their customers. Neobanks can leverage their customer data and digital infrastructure to assess credit risk and offer personalized loan products. Interest rates and fees charged on loans can be a significant source of revenue for neobanks.

Partnerships

Neobanks can enter into partnerships with other financial service providers or third-party companies to offer additional products and services to their customers. This can include partnerships with payment processors, insurance companies, investment platforms, or other fintechs. Neobanks can earn referral fees, commissions, or revenue-sharing arrangements from these partnerships.

Cross-selling and upselling

Neobanks can leverage their customer base and data to cross-sell and upsell additional products and services. For example, digital banking can offer savings accounts, investment products, or insurance products to their customers based on their financial needs and preferences. Cross-selling and upselling can be an effective way to increase customer engagement and generate additional revenue.

White-label solutions

Neobanks can offer their banking infrastructure and technology as white-label solutions to other businesses or financial institutions. This can include providing banking-as-a-service (BaaS) or platform-as-a-service (PaaS) solutions, where other companies can build their own branded neobank using the neobank’s technology stack. White-label solutions can generate revenue through licensing or usage fees.

Data monetization

Neobanks can monetize the customer data they collect by offering anonymized and aggregated data to third-party companies for market research, customer insights, or targeted advertising. Data monetization can be a significant source of revenue for neobanks, but it requires careful consideration of data privacy and security regulations. It’s important for neobanks to carefully evaluate and choose the right business model and monetization strategies that align with their target market, customer base, and growth plans.

Neobanks should also consider the competitive landscape, regulatory environment, and customer expectations to develop a sustainable and profitable business model.

Neobank development: from idea to strategy

Developing neobank software is a challenging task, as the system must ensure the safety of their customers’ financial data, which involves implementing robust security measures and complying with regulatory requirements. Also neobanks need to integrate with a variety of third-party providers to offer additional services, such as international money transfers and foreign exchange, which adds another layer of complexity to the development process.

You can start building your own payment software from scratch, but must be ready that process requires a lot of your resources and can take 1 or 2 years. It is also crucial to find a proficient development team capable of managing a complex fintech project, along with a sufficient amount of time to build the project from the beginning.

If you value cost and time efficiency, using a pre-developed neobanking solution may be a more affordable decision for you. It allows you to label and customize the finished software according to your product requirements and significantly speed up the release.

How to build a digital bank on top of SDK.finance platform?

Start with setting up the infrastructure and services

To create a foundation for the future neobank, it’s essential to configure the environments, including development, pre-production, and production to provide seamless and efficient development process. Furthermore, it is necessary to establish services that can help with deployment, monitoring, and maintenance activities.

Configure development, pre-production and production environments

SDK.finance FinTech system consists of three servers: a developer’s instance for software development and testing, a production instance for live operation with real end-users and transactions, and a pre-production or Sandbox instance with the same specifications as the production server, primarily used for debugging third-party component integrations.

Requirements of the instance for production and test environments:

CPU – 1

RAM – 2 GB

SSD – 40 GB

OS: Ubuntu 20.04 LTS

Software: NGINX 1.14.0

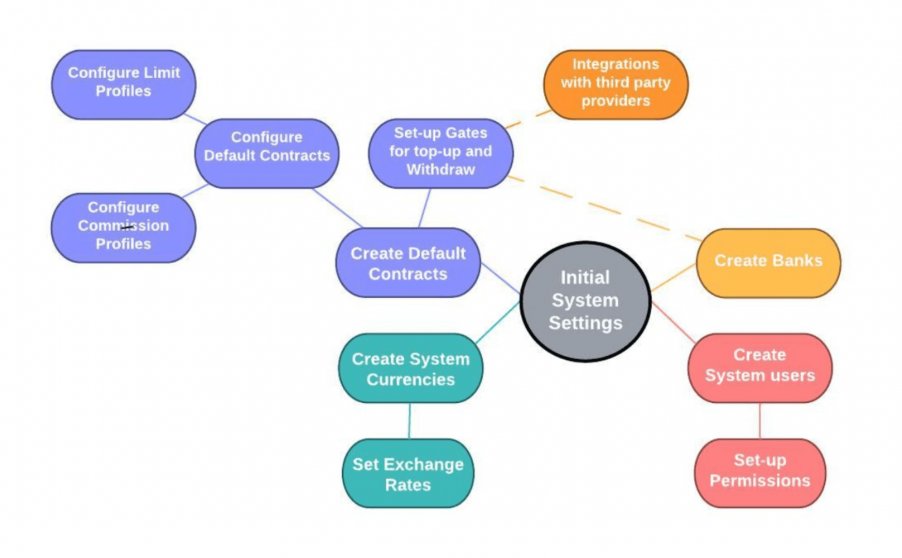

System configuration

To optimize the performance and security of a neobanking platform, several important tasks must be performed, such as setting up roles, configuring commissions, creating wallets and currencies, setting up contracts, setting exchange rates, and granting permissions. Proper execution of these tasks can ensure the smooth and efficient functioning of the payment system.

To initiate the setup of SDK.finance payment software, the first step involves authentication as an administrator via the API. After successful authentication, the API returns a token along with other user parameters in the response, which is crucial for accessing other APIs. If necessary, you can choose other parameters as per your requirements.

System management

System management allows you to set specific standards and rules for user behavior and determine the key services and features that customers, including individuals and merchants, have access to.

There are several use cases within the system management:

The contract management includes the creation of individual contracts, the insertion of commission rules, the editing of system settings and the activation of provider commissions.

Payment gateway management includes configuring exchange rates and managing currencies.

Reports and analytics provide the ability to create transaction-based reports that can be downloaded for further analysis of customer data.

See our knowledge base for more information on system management.

Payments and transactions

This step includes money transfers, bill payments, recurring payment setup, currency exchange, bill payment, and merchant payment services.

Bill payments

The system offers users the ability to make payments for utility bills, cell phone top-ups and other services using their neobank account.

This functionality can be used through integration with any relevant payment provider.

SDK APIs can be used to decouple billing from customers’ virtual accounts. To enable certain payments, the process should be added to the contract.

Launch your digital bank in weeks, not years

Talk to Our TeamRecurring payments

Recurring in-system payments can be implemented using subscription features. Subscriptions allow individuals or businesses to make recurring payments for a service or product. SDK.finance provides pre-implemented subscription expiration functions with various settings, such as payment period, number of payments, and subscription end date.

Subscriptions can have different statuses:

active

- stopped

- processed

- canceled

The expiration type of a subscription determines how it ends, either on a certain date, after a certain number of payments, or with no limit on the duration.

Read our knowledge base to learn more about payments and transactions.

Invoicing

Neobank systems built on SDK.finance enable users to create, send and manage invoices electronically, streamlining the process and making it more efficient.

Merchants can effortlessly create and monitor invoices, streamline payment reminders, and process customer payments. This simplifies financial operations, minimizes errors and administrative tasks, and increases customer satisfaction through a smooth and seamless payment process.

Our current set of use cases related to invoicing includes:

- issue of invoice

- view/search and filter the list of issued invoices

- invoice templates

- payment of invoices

Check out our knowledge base to dive into the invoicing for neobank development.

Create your digital banking solution in weeks

Talk to Our Team