Starting a digital bank in 2026 is not just a technology challenge. It is a licensing, compliance, infrastructure, and operations challenge. Most teams that fail do so not because they could not build an app, but because they underestimated what regulated financial infrastructure actually requires. A real-time ledger, AML controls, card processing, fee management, multi-currency operations, and audit-grade reconciliation are not optional extras. They are the minimum. The path is clearer than it used to be. Proven licensing models exist at every level of ambition, from a sponsor-bank MVP to a fully licensed digital bank. Ready fintech platforms like SDK.finance reduce the infrastructure burden dramatically, especially when the team wants speed without giving up long-term technology control. This guide covers licensing options, realistic costs, technology architecture, step-by-step launch sequence, build versus buy decisions, and how SDK.finance fits as a platform foundation for a digital bank, neobank, or banking-adjacent fintech product. SDK.finance provides core banking infrastructure with ledger, payments, wallets, ready applications and flexible deployment options The terminology varies by market, but the meaningful distinction is regulatory and economic: who holds the license, who is responsible for safeguarded or insured funds, and what revenue model the product can legally support. The most important point is economic. Card-led consumer neobank models often need additional revenue layers – subscriptions, FX, SME services, lending where licensed, payment processing, or embedded finance – because interchange alone rarely supports a durable business. The licensing strategy should follow the maturity of the business, not the ambition of the brand. A full banking license gives the most control, but it is rarely the right first step for a fintech MVP. A sponsor-bank or BaaS model is usually the fastest route to market. An EMI or PI license is often the best middle path for payments, wallets, cards, FX, and multi-currency products. A full bank charter starts to make sense only when deposit-taking, lending, and balance-sheet economics become central to the business model. A full bank charter gives the widest product surface: It is also the most demanding path. In the US, a new bank normally needs approval from a chartering authority and deposit insurance from the FDIC; the Federal Reserve notes that starting a bank can take a year or more and usually involves more than one regulator. In the UK, the Bank of England/PRA new bank authorisation process provides a structured route, including mobilisation for firms that need to complete build-out under restrictions. This path is best for teams that need direct deposit-taking, lending from their own balance sheet, and maximum control over the financial relationship. It is rarely the fastest path for a fintech MVP. An EMI or PI license is often the most practical starting point for a payments-led digital banking product. It can support: It does not automatically allow deposit-taking or bank-style balance-sheet lending. In the EU, PSD2 sets different initial-capital thresholds for payment institutions depending on services, while e-money institutions are subject to a higher initial-capital requirement. The European Banking Authority provides the regulatory framework context for payment services and e-money. In the UK, the FCA regulates payment and e-money institutions, with increasingly strict safeguarding and reconciliation expectations. BaaS is a commercial and technical delivery model, not a license type. It lets a digital banking team launch on top of a partner bank or regulated provider while operating the customer-facing product layer. It can be fast and capital-efficient, but it creates dependency on the sponsor’s compliance requirements, pricing, technical capabilities, risk appetite, and strategic direction. The right sequence for many teams is: BaaS for product validation, EMI/PI once product-market fit is established, and a full bank charter only when deposits and lending become the core economic engine. A platform like SDK.finance does not replace licensing. It provides the software foundation beneath the licensed operation. Licensing determines what you are allowed to do; your platform determines how efficiently you can do it. A realistic 2026 launch budget starts from $100k-$250k for a SaaS or lean MVP path and can reach $1M-$5M+ for custom or fully regulated builds. A fully licensed bank can require substantially more once regulatory capital, legal work, risk teams, audits, and operations are included. As a market benchmark, SDK.finance analyses of enterprise core banking vendors estimate Temenos at about $518,000 per year on average and FIS in a broad $300,000-$1 million annual range, confirming that core banking software costs can quickly reach hundreds of thousands of dollars per year before implementation, migration, and customization are included. SaaS gives the fastest start with lower upfront cost and no infrastructure overhead. It is useful for testing transaction scenarios, validating assumptions, and launching with managed infrastructure. Source code costs more upfront but gives 100% vendor independence: your team owns the codebase, deploys in its own environment, integrates providers directly, and continues development on its own roadmap. SDK.finance offers both. For serious fintech teams building a differentiated long-term product – especially in markets with data-residency requirements, custom compliance obligations, or deep technical ownership needs – the source-code license is the strategically stronger choice. Successful digital banks do not start by being a better bank for everyone. They start with one use case where digital execution is materially better than incumbents: SME invoicing and payroll, cross-border payments for a specific corridor, salary-day money movement, embedded treasury for software platforms, or mobile-first wallets for underserved customers. Revenue can come from subscriptions, FX spread, payment processing, merchant fees, interchange, lending margins where licensed, or embedded finance platform fees. Plan unit economics before build begins. A mass-retail free-card model needs much higher volume than an SME or B2B infrastructure model. A practical staged approach is BaaS MVP for validation, EMI/PI once product-market fit is established, and a full bank charter only when deposits and lending become core to the economics. Start with the lightest regulated structure that supports the first product. Compliance needs to be part of the product architecture: KYC/KYB, AML/CTF, sanctions and PEP screening, transaction monitoring, suspicious-activity workflows, audit logs, data retention, complaint handling, and reporting. A digital bank needs a reliable ledger, account and wallet logic, transaction statuses, reversals, fees, limits, multi-currency support, reconciliation, and audit trails. SDK.finance provides these as a configurable fintech platform rather than a blank engineering project. The customer layer should cover onboarding, accounts, wallets, balances, transfers, card management, transaction history, notifications, and support. For related reading, see Mobile Banking App Development and Banking App Development: How to Create a Bank Application. Plan for development, pre-production, and production environments. SaaS reduces infrastructure burden. Source-code delivery gives full deployment control for teams with data-residency, security, or architecture requirements. Configuration includes currencies, providers, contracts, fees, limits, exchange rates, roles, permissions, and available operations. This is where a configurable platform saves time because business logic does not need to be hard-coded for every rule. User management covers individual and business users, document collection, verification statuses, risk levels, approvals, account restrictions, and compliance review flows. A digital bank usually depends on KYC providers, AML tools, sponsor banks, payment processors, card issuers, FX providers, open banking providers, analytics tools, and customer support systems. SDK.finance’s API-first architecture and provider model support this integration layer. Test failed payments, reversals, dispute flows, reconciliation under load, provider downtime, permission boundaries, AML alerts, support processes, and incident response. The happy path is not enough. Track activation rate, KYC pass/fail rate, payment success rate, card authorization rate, reconciliation breaks, fraud loss ratio, support tickets, complaint rate, revenue per active user, and retention by segment. Pros: full architectural control and proprietary IP across the stack. Cons: long build timeline, high cost, ledger and reconciliation risk, security burden, and a maintenance load that pulls engineering effort away from differentiation. Pros: fast time to market. Cons: vendor lock-in, limited customization, opaque codebase, dependency on vendor roadmap and pricing, and difficult exit if the vendor changes direction. This is the model SDK.finance was designed for. A ready fintech platform gives the compressed timeline of white-label software. Source-code delivery gives the customization freedom and vendor independence of a custom build. You are not choosing between speed and control – you get both. Most fintech teams spend the first 12-18 months doing work that has already been done before: designing ledger logic, building fee engines, writing back-office tooling, wiring role-based access, and connecting currencies and providers. This is not differentiated work. It is table stakes – and it consumes budget that could go toward customer experience, compliance quality, distribution, and partnerships. SDK.finance exists to solve that problem. What is SDK.finance? The core proposition is simple: you bring the license strategy, brand, regulated partners, and business model. SDK.finance provides the financial infrastructure that makes it work. For executive teams evaluating long-term technology strategy, the source-code option addresses one of the biggest risks of working with any third-party fintech platform: lock-in. With SDK.finance source-code delivery, your organization can own the codebase, deploy in its own infrastructure, integrate directly with providers, build custom modules, and evolve the platform on its own roadmap. This is the difference between renting infrastructure and owning it. SaaS is excellent for speed. Source code is stronger when the business needs technology independence, custom compliance logic, specific deployment requirements, or long-term product control. The ROI argument is straightforward. A custom build of the infrastructure SDK.finance provides – ledger, fees, limits, roles, currencies, back office, APIs, and mobile interfaces – can take years and cost millions to reach production quality. SDK.finance compresses that to a fraction of the time and cost, while keeping the product flexible enough for serious fintech ownership. That budget delta becomes available for the work that actually differentiates your product: distribution, compliance, customer experience, market entry, and partnerships. To see the customer-facing product layer, watch the SDK.finance mobile banking app demo: Recognized by leading FinTech and banking technology awards. SDK.finance has been recognized by major industry programs, including PayTech Awards 2026, Banking Tech Awards 2025, and other international FinTech and banking software awards. Regularly featured among top banking software providers. SDK.finance has been included in industry rankings and market reports such as the Everest Group Top 50 Core Banking Technology Providers 2026 and other core banking systems report. Proven in launched products and high-volume processing. SDK.finance software powers implemented financial products across the US, Canada, the EU, the UK, and MENA; one Saudi Arabian payment system built on SDK.finance processes around 75% of national payments, demonstrating scalability for high-volume, mission-critical transaction processing. SDK.finance provides core banking infrastructure with ledger, payments, wallets, ready applications and flexible deployment options Based on SDK.finance’s 15+ years of experience supporting the launch of digital banking and fintech products, the biggest failure pattern is treating speed as the strategy: teams go live quickly, but struggle to scale because ledger logic, reconciliation, compliance workflows, provider orchestration, and operational visibility were not designed for growth from day one. The stronger approach is to start with infrastructure that is ready not only for launch, but for the next stages of volume, complexity, and market expansion. If you are planning a digital bank, neobank, wallet, or payment product, SDK.finance can help you choose the right platform model and move from idea to launch with a scalable foundation. Book a demo to see how SDK.finance can support your digital banking launch.Quick Answer: How Do You Start a Bank?

Digital Bank vs. Neobank vs. Fintech App

Type

License holder

Deposit-taking

Lending

Launch speed

Best fit

Fully licensed digital bank

Own bank charter

Yes, subject to local deposit-protection rules

Yes

2-4 years

Long-term full-stack banking

EMI/PI neobank

Own EMI or PI license

No bank deposits; safeguarded e-money

No or limited

6-18 months

Wallets, cards, transfers, FX

Sponsor bank/BaaS neobank

Sponsor bank or licensed partner

Via partner structure

Via partner

6-12 weeks for MVP

Validation and fast market entry

Fintech app

No direct license; relies on partners

No

No

Weeks

PFM, payments UX, referral products

Main License Paths for Launching a Digital Bank

Strategy

Best when

Main trade-off

Start with sponsor bank/BaaS

You need to validate demand quickly and reduce regulatory capital requirements at MVP stage.

Fastest route, but creates partner dependency and less control.

Move to EMI/PI license

The product has traction and is focused on payments, wallets, cards, FX, or multi-currency accounts.

More control than BaaS, but still not a full deposit-taking bank.

Apply for full bank charter

Deposits, lending, net interest margin, and primary banking relationship are core to the business.

Maximum control, but highest capital, governance, and timeline burden.

Full banking license

EMI or Payment Institution license

Sponsor bank or Banking-as-a-Service partnership

White-label or configurable banking platform

How Much Does It Cost to Start a Digital Bank?

Model

Starting budget

Typical full budget

SaaS digital banking platform

$100k-$250k

$250k-$600k+

Sponsor bank/BaaS MVP

$150k-$300k

$300k-$700k+

EMI/PI neobank

$300k-$700k

$700k-$2M+

Ready platform with source-code license

$250k-$600k

$600k-$1.5M+

Custom build from scratch

$800k-$1.5M

$1.5M-$5M+

Fully licensed bank

$2M-$5M+ before scale

$5M-$20M+

SaaS vs. source-code license: the trade-off

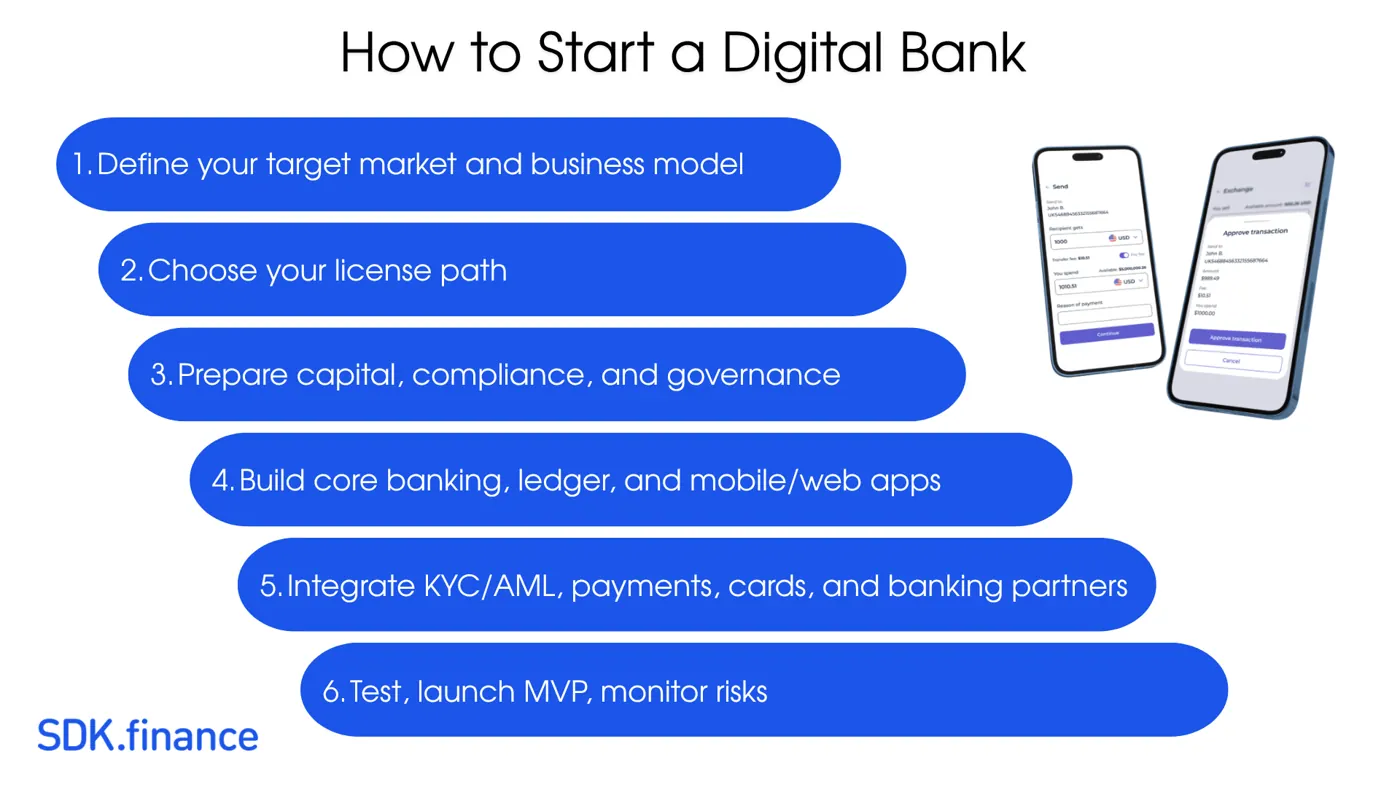

Step-by-Step Roadmap: How to Start a Digital Bank

Step 1. Choose a narrow market wedge

Step 2. Define business model and unit economics

Step 3. Select your regulatory path

Step 4. Build compliance and risk foundation

Step 5. Choose core banking and ledger architecture

Step 6. Design customer experience

Step 7. Set up infrastructure and environments

Step 8. Configure the system

Step 9. Set up user management and KYC

Step 10. Connect payments, cards, and third-party providers

Step 11. Test operations before launch

Step 12. Launch, monitor, and expand

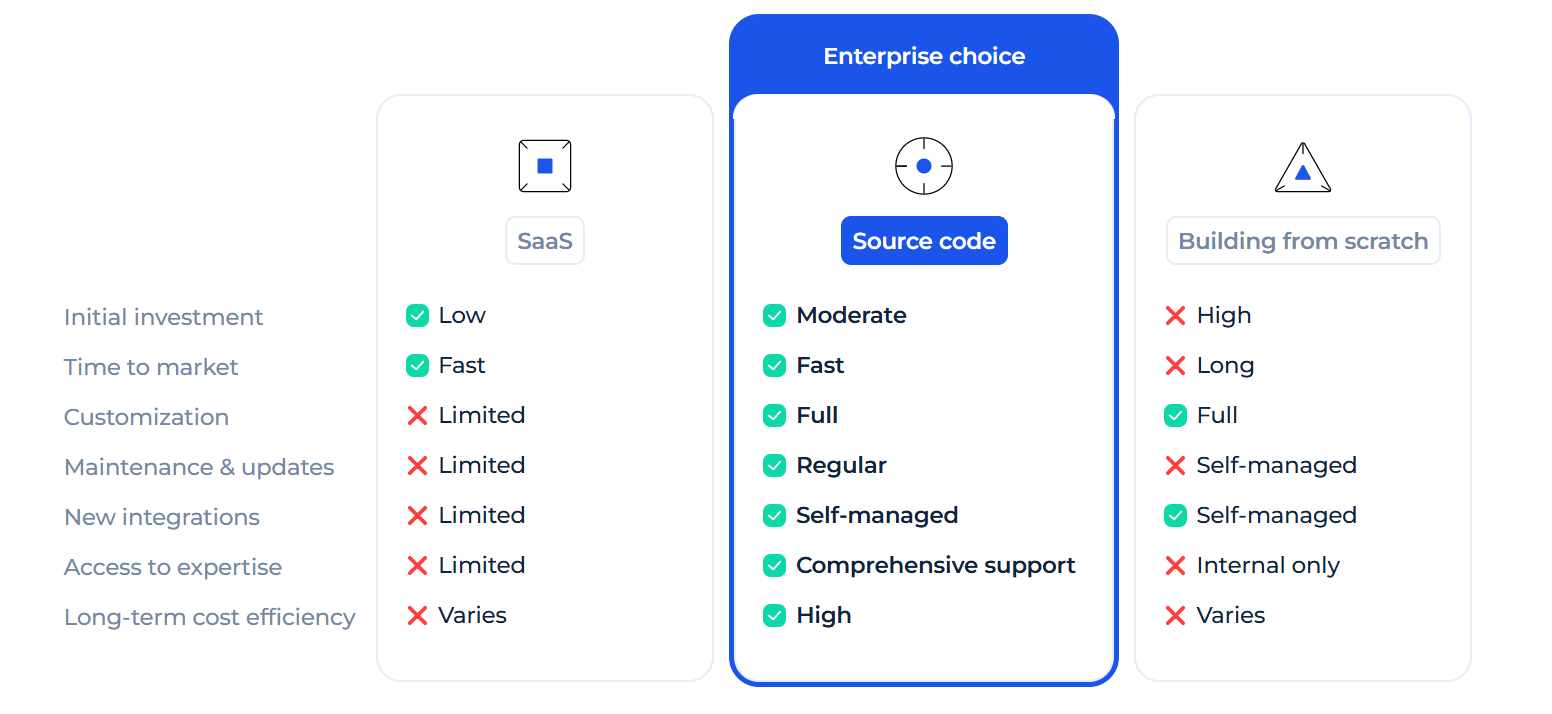

Build vs. Buy vs. Source Code

Build from scratch

Closed white-label platform

Configurable platform with source-code ownership

How SDK.finance Helps Start a Digital Bank Faster

SDK.finance is a ready-to-use fintech software platform built on 15+ years of financial infrastructure engineering, helping companies launch digital banks, neobanks, wallets, payment products, and embedded finance solutions faster with core infrastructure, APIs, back office, mobile/web interfaces, and SaaS or source-code delivery for full vendor independence.

What you get on day one

Source-code license for 100% vendor independence

The business case for using a platform

Proven FinTech and Banking Software Expertise

Common Mistakes When Starting a Digital Bank

Building a FinTech product, PSP/EMI platform, digital wallet, neobank or crypto-friendly banking solution?

For a deeper internal benchmark, see SDK.finance's full cost guideHow Much Does It Cost to Build a Bank in 2026

Building a FinTech product, PSP/EMI platform, digital wallet, neobank or crypto-friendly banking solution?