As digitalization continues to redefine the finance sector as we know it, customers are demanding a swift shift to digital banking services. While traditional banks and Fintechs are upgrading their systems to meet these demands from their customers, neobanks are creating digital bridges to connect numerous businesses and users to digital financial services, especially in areas not sufficiently covered by conventional banking activities.

But then the following questions come to mind: what is neobank? What are the features of neobanks? What are the pros and cons of using the services of neobanks? Stick along as we provide answers to all basic questions relating to neobanks.

What is neobank?

Neobank is a species of online FinTech institution that offers basic banking services by implementing cutting-edge technology. Unlike traditional banking institutions, neobanks offer banking services strictly online, via mobile apps, or online banking. While they possess no physically identifiable branches, they afford the customer avenues to open an account seamlessly, control their finances in real-time, and make online purchases from anywhere.

Neobank vs traditional bank

Image source: SDK.finance neobank solution mobile interfaces

Neobanks and traditional banks are two different types of financial institutions, each offering distinct features and approaches to banking services. Neobanks, also known as digital banks or challenger banks, are fully digital, technology-driven financial institutions that operate primarily through mobile apps or online platforms.

Traditional banks are established financial institutions with a physical presence, including brick-and-mortar branches. They have been operating for many years and offer a wide range of banking services. It’s important to note that some traditional banks have also embraced digital transformation and offer online and mobile banking services. Likewise, neobanks may partner with traditional banks to leverage their established infrastructure and regulatory compliance.

Digital bank vs neobank: is there a point of divergence?

Neobanks should not be confused with digital banks. Though similar in some ways, both are different forms of financial institutions. While digital banks are usually an offshoot of traditional banks with physical branch networks and offer a wider range of banking services, neobanks are strictly online fintech institutions with no physical branch networks.

Neobanks are sometimes called challenger banks because they compete with incumbent banks and provide services to areas not sufficiently covered by the conventional banking system, without any stress, and at zero fees.

Key neobank features

- They are cost effective

- Offer personalized financial services through A-I-powered technology

- Do not have any physical branch network

- It also operates a 24/7 financial service system

Create your digital banking solution in weeks

Talk to Our TeamHow does a neobank work?

The neobanks’ modus operandi is very simple, and the same goes for the requirements needed to start one. Neobanks attempt to distinguish themselves from regular banks on a basic level, making themselves more appealing to technologically driven consumers (especially Gen Z and millennials) who are increasingly becoming dissatisfied with the bureaucratic nature of traditional banks.

Source: Nielsen

One of the foundations of neobanks is the absence of a physical branch network, and as such, they perform their operations strictly within the online space, thereby lowering customer expenditure. Neobanks employs AI-powered technology to collate customer data to provide personalized banking services to users.

The vast amount of data they acquire from their consumers is used to understand their users better, identify problems, and develop requisite solutions. Because their systems are also significantly computerized, collecting and analyzing data and understanding how their clients interact in the financial ecosystem becomes much easier.

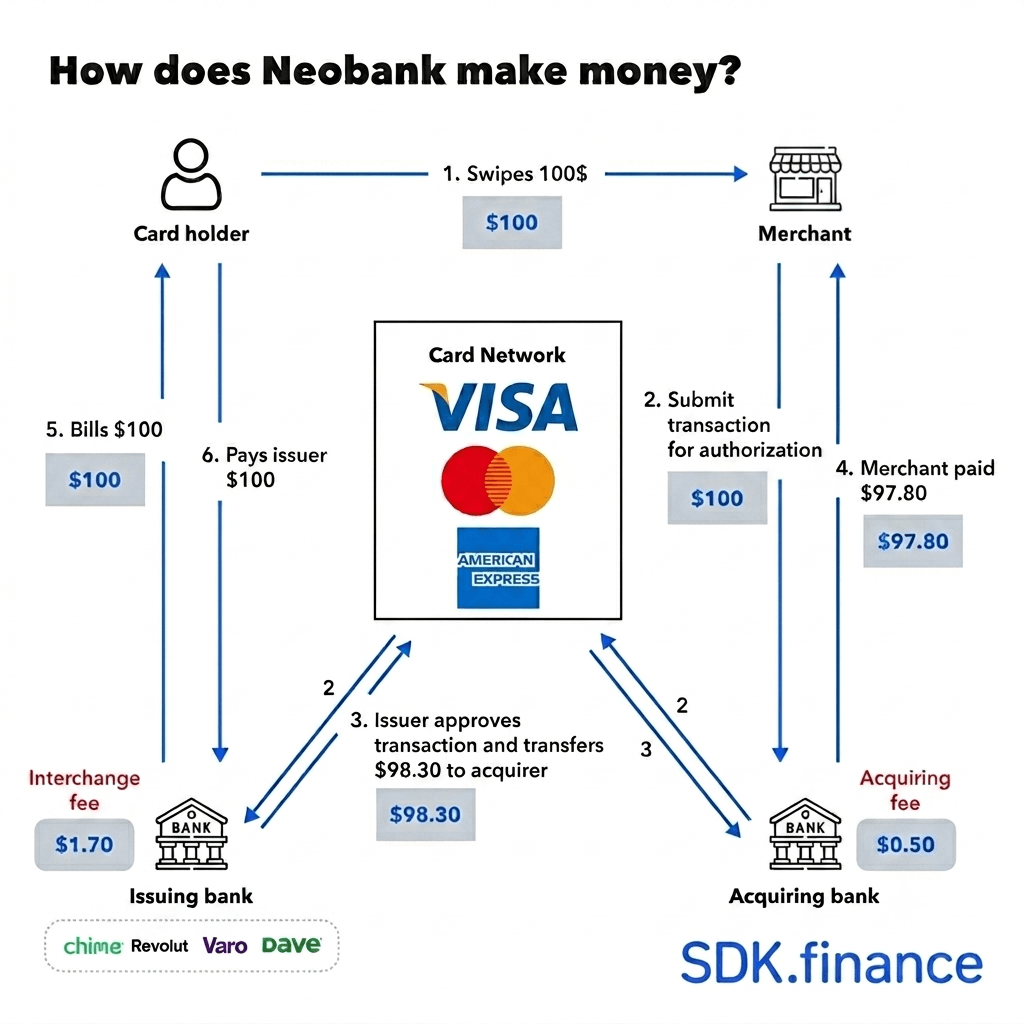

How do neobanks make money?

So, how do neobanks make money?

According to the stats by Research And Markets, the global neobanking market is projected to hit $333.4 billion by 2026, at an annual growth rate of 47.1%. The projected growth is impressive, given that they are quite new, have no identifiable physical structure, and haven’t built a substantial confidence level. The big question then is, how do they stay profitable?

Neobanks operate a business model different from conventional banks. A large percentage of their profit is generated from interchange fees paid by businesses whenever customers purchase with a neobank’s debit card.

For instance, Chime, a popular neobank platform in the US, has a user base of around 12 million and issues an actual debit card to registered users. Whenever users make a purchase using the Visa debit card, a fee of 1.5% is charged by Visa. Visa, in turn, pays a fraction of the charges to Chime neobank.

Another important aspect of how do neobanks make money is that they also profit from interchange fees whenever users make a purchase using a neobank credit card. A bit of context is the Nubank business model. Nubank is a neobank based in Brazil that boasts more than 40 million users. They offer credit card services and charge a fee for every transaction performed by their user. They also profit from the interest charge on users’ over-drawn credit balances.

Furthermore, neobanks benefit from interest charges on deposits and account opening. They also profit from the interest earned on ATM fees.

Now we are quite familiar with the concept of neobanks, their features, mode of operation, and revenue generation. Let’s look at some neobank pros and cons.

Neobank business model

Neobanks, much like traditional banks, cater to specific niches and even entire nations. The crucial question arises: What business model ensures organizations remain competitive in this dynamic landscape?

There are 5 neobank business model types:

Ecosystem-led model

The ecosystem-led model emphasizes connectivity and collaboration among different financial applications by leveraging API technology. This approach enables seamless communication and integration.

Interchange-led model

Interchange-led model neobanks charge transaction fees for each monetary transaction. For example, Chime in the USA and Neon in Brazil earn a portion of Visa fees during transactions made with their Chime Visa.

Credit-led model

The credit-led model relies on credit card services as a foundation for growth and profitability. It generates revenue through transaction fees and profits from carried balances and associated interest rates. Nubank in Brazil is an example of a neobank that adopts this model.

Asset-led business model

The asset-led business model allows neobanks to offer savings accounts and deposits, such as high-yield savings and certificates of deposits (CDs). Marcus, by Goldman Sachs on Wall Street, exemplifies this model by focusing on niche products and emphasizing specialization over a diverse range of services.

Product extension-focused approach

In contrast to the ecosystem-led model, the product extension-focused approach eliminates barriers to financial services. Robinhood provides a notable example, introducing Robinhood Gold, a product extension offering in-depth market analysis through a subscription-based model. This strategy enhances Robinhood’s competitive position by expanding its product offerings.

To remain competitive in the dynamic neobanking sector, it is essential to understand and strategically adopt these diverse business models.

Advantages of neobanking

Lower operational costs

Neobanks operate at a cheaper cost because of their lack of physical branch networks and fewer personnel. Typically, the capital savings associated with their no-branch business model are passed down to their consumers in the form of cheaper rates and no monthly fee payments.

Effortless banking methods

Neobanks have changed banking by moving away from the old model of visiting a bank branch and queuing for hours before transacting, to a system of digitally tailored self-service ideas. With neobanks, all you need is a mobile app that enables you to conduct simple financial activities from anywhere.

Speed

Neobanks also boast of speed in their method of service rendering. With a neobank, you could open an account, make a deposit, transfer money, and make online purchases faster than you could locate a traditional bank branch.

Use of technology

Neobanks use AI-powered technology to provide upgraded services to users. They also use AI-powered technology to understand customers’ interaction with their service and thus provide quality services tailored to their specific needs.

More efficient for international payments

One of the benefits of neobank solution in terms of performing an international payment is that they only require you to open an account with them and then use your cards for international transactions. Traditional banks, most times, would require you to perform some form of upgrades to your account before being allowed to perform international transactions.

Disadvantages of neobanking

Lack of bank charter/license

Most neobanks lack legal documents empowering them to operate as a bank. They must partner with other banks to back their product and services. As a result, a duty of due diligence is expected from users to ensure that the neobank platform of their choice is partnered with a bank that FDIC insures.

Absence of physical branches

This is one of the most limiting factors of neobanks. As a result, they seem impersonal and do not engender trust (especially among the older generation).

Use of technology

High-end technology employed to provide financial services may pose some difficulties to the older generation, who may not be in tune with modern technological advancements.

Ready backend, APIs, and integrations

Bottom line

Neobanking emerged in response to the rapid digital transformation of the financial sector, and it continues to reshape how customers access banking services. Instead of relying on physical branches and traditional banking workflows, users can open accounts, manage funds, make payments, exchange currencies, and access financial services directly from digital channels.

However, launching a neobank requires more than a customer-facing app or a strong business idea. To operate legally and securely, you need the proper regulatory setup, which may include obtaining your own financial license or partnering with a licensed institution, depending on your target market and business model. Alongside licensing and compliance, you also need reliable technology infrastructure to manage accounts, transactions, fees, limits, integrations, reporting, reconciliation, and back-office operations.

SDK.finance provides the software layer for launching and operating a neobank. Our digital banking software helps fintech companies and financial institutions build neobank products faster, with ready-made functionality for:

- customer onboarding,

- multi-currency accounts,

- transfers,

- transaction history,

- card issuing,

- reconciliation,

- roles and permissions,

- API-based connections with third-party providers.

It is important to note that SDK.finance does not provide a banking or EMI license and is not a bank or financial institution. Your company remains responsible for the required licenses, regulatory permissions, compliance setup, and licensed partners in your operating region. What SDK.finance provides is the technology foundation: flexible neobank software that can be configured around your business model and scaled as your digital banking product grows.

Explore SDK.finance neobank software to see how our platform can support your digital banking launch.

Create your digital banking solution in weeks

Talk to Our Team