The right banking platform can make or break a business. Compared to outdated legacy systems, modern digital banking platforms offer more services, flexibility, and opportunities. Current technology can help digital banks and fintechs dramatically improve cost-effectiveness and increase their competitive advantage.

Choosing a digital banking platform requires a good understanding of your business, from strategy, budget, and technical capabilities to timeframes, standards, and relevant regulations. However, with a wide range of options available in the market, finding the ideal digital banking platforms can be a complex and challenging task.

In this article, we will explore key factors and considerations that can guide financial institutions on how to choose a digital banking platform for their specific needs.

The key factors to choose a digital banking platform

When choosing the digital banking platforms, several key factors should be considered. These factors will help determine the suitability of the platform for your institution’s needs and ensure a successful implementation. Here are the key factors to consider to choose a digital banking platform:

Functionality

Evaluate the platform’s core banking functions, e.g., account management, payments, lending, and reporting. Make sure the platform supports your institution’s specific banking services and products.

Scalability

Look for the platform’s ability to handle growing transaction volumes, support a larger user base, and allow for future expansion. It should be scalable both vertically and horizontally to meet your institution’s growth needs.

Integration capabilities

Assess the platform’s compatibility and ability to integrate with your existing systems, third-party services, and emerging technologies. Seamless integration is critical to data flow, operational efficiency, and delivering a consistent customer experience.

Usability

A user-friendly interface and intuitive design are critical to customer satisfaction. Look for platform usability, customization options, accessibility across devices, and features that improve customer engagement.

Deployment options

Check that the platform offers deployment options that align with your facility’s infrastructure IT, security requirements, and future scalability needs. Common options include cloud-based solutions or on-premise deployments.

By carefully considering these key factors, you can choose a digital banking platform that aligns with your institution’s goals, increases operational efficiency, improves the customer experience, and positions you for future growth in the digital banking landscape.

Advantages of choosing a digital banking services

Future-proof microservice architecture

The capacity to roll out new features quickly has allowed modern digital banks like Revolut, N26, and Monzo to capture a significant market share in different markets worldwide. Compared to a traditional bank app that gets only a few updates annually, Revolut releases an update weekly. You can learn more about what it takes to build a Revolut-like digital bank in our previous article.

The ability to roll out new features rapidly comes down to microservice architecture. The technology increases flexibility as new services, integrations, changes, and customizations can be added to the existing product. The microservice architecture allows to take innovation to an entirely new levels as businesses have ready access to their technology.

Accelerate time to market

With ever-changing customer preferences and rising competition in the financial industry, banks and FinTech must be agile to respond to market changes or risk losing market share. Launching new digital products and services quickly and tailoring them to new demands through rapid iterations plays a vital role in successful business development.

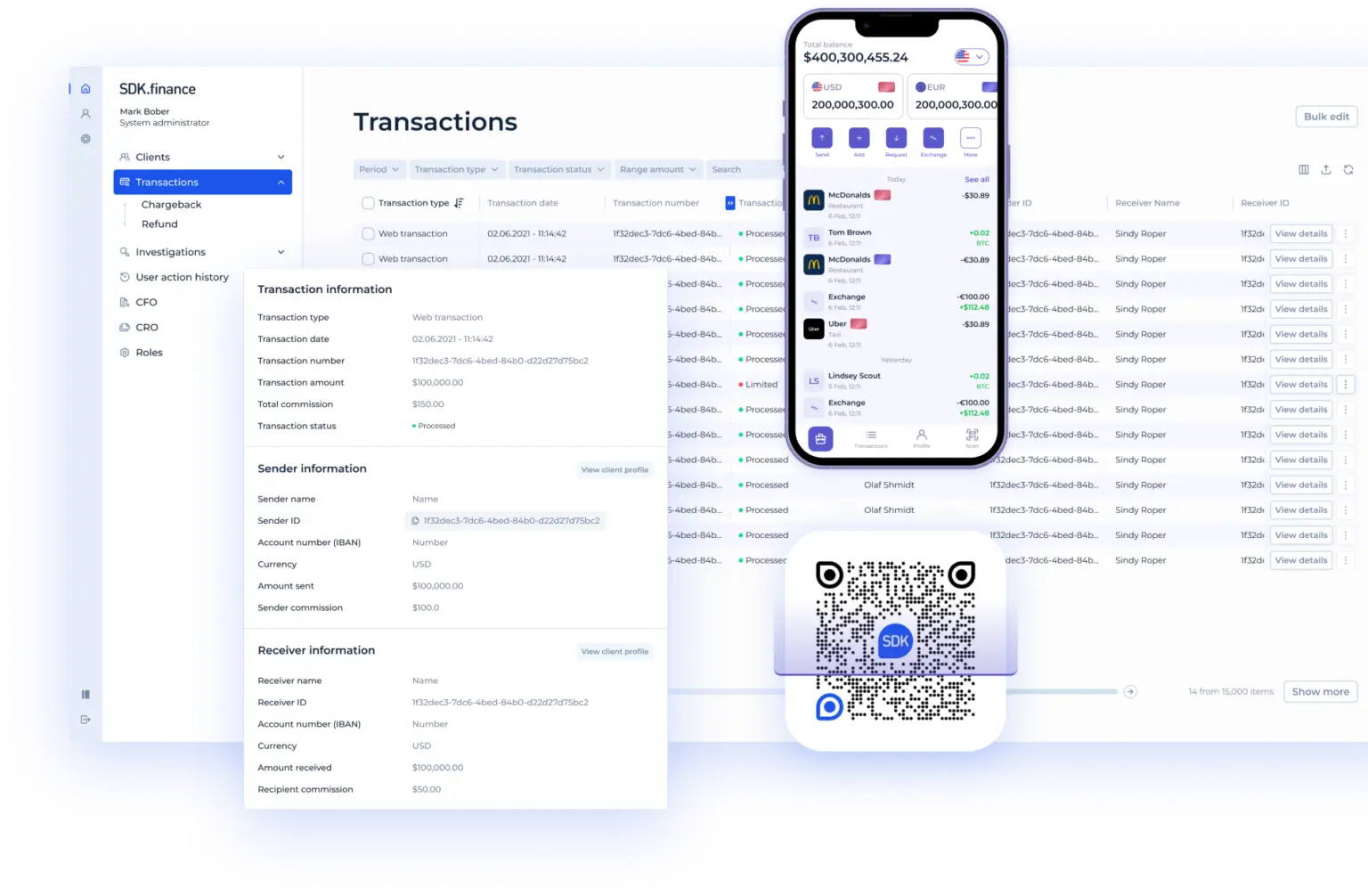

The right digital banking provider will offer a platform with all main banking functionalities: customer onboarding, account opening, bank card issuing, KYC, money movement tools, payments, currency exchange, and support, among others. With these features, banks and FinTech can launch their solution with predefined functionality in a fraction of the time it would take to develop it in-house.

Then, functionality can be extended to add new features to improve the banking experience for your customers. Adding more complicated operations, additional security measures, and countless integrations with financial, payment, and insurance providers can truly be unique.

Another important point to choose a digital banking platform provider should offer white-label front-office – web and mobile banking applications. It is much faster to rebrand and customize existing solutions than to develop them from scratch, which can easily last longer than six months. With ready-made applications adapted to your business, you don’t waste months entering the market and losing out on potential customers.

Open banking ready

PSD2, the Revised Payment Service Directive brought into law in 2018, aims to spur innovation and acknowledge the rise of fintech, ensure security and protect customers, level the playing field for challengers, and herald the beginning of open banking. It is essential to consider European legislation to choose a digital banking platform and its respective architecture.

Banking solutions that rely on open APIs can be easily integrated with third parties and other banks in the financial ecosystem to create new useful products and services. Loyalty, budgeting, and insurance products made through partnerships and connected through APIs already generate value for banking customers. Connections between services not only add new features to your products but create new revenue streams and opportunities.

Accessible and available integrations with third-party providers

A digital banking platform is much more than just a foundation for front and back offices. Modern FinTech solutions enable banks to create complex but efficient systems of connections and integrations for their business. Expanding functionality through integrations with an ever-increasing number of service providers is cost-effective and agile.

Whether it’s banks, currency exchange, KYC, remittance, or payments, digital banking providers should have accessible integrations that work with the product and technical support for any additional integrations. With an integration framework and a flexible infrastructure, banks can innovate and roll out products and services ahead of their competition.

Leading Digital Core Banking Platform Vendors

When evaluating a digital core banking platform, it’s essential to understand how different providers approach scalability, flexibility, and integration. The market offers a mix of long-established banking software vendors and newer, cloud-native FinTech cores.

Below is a comparison of top digital core banking providers highlighting their headquarters, areas of expertise, target clients, and delivery models. This overview helps decision-makers identify the right partner depending on their business priorities – from full source code ownership to a SaaS subscription model.

Top Core Banking Platform Vendors Comparison

| Vendor | Headquarters | Key Focus | Product Highlights | Target Clients | Delivery Model |

|---|---|---|---|---|---|

| SDK.finance | Vilnius, Lithuania | Leading digital banking platform | 60+ functional modules, 470+ APIs, real-time ledger, source code access, PCI DSS Level 1 | Banks, PSPs, EMIs, enterprises, neobanks | Source Code License or PaaS |

| Temenos | Geneva, Switzerland | Universal core banking system | Modular T24 Transact platform, open APIs, advanced analytics | Retail, corporate, wealth banks | SaaS or on-premise |

| Mambu | Berlin, Germany | Cloud-native banking engine | Composable architecture, lending & deposit engines, API-driven | Neobanks, lenders, telecoms | SaaS |

| Backbase | Amsterdam, Netherlands | Digital banking engagement platform | Customer experience orchestration, omnichannel UI | Banks modernising front-end and CX | SaaS |

| Oracle FLEXCUBE | Austin, USA | Enterprise-grade banking suite | Core banking, treasury, and compliance modules | Large global banks | On-premise or Oracle Cloud |

| Finacle (Infosys) | Bangalore, India | Core and digital banking | Real-time processing, open APIs, analytics tools | Retail and SME banks | SaaS or hybrid |

| Finastra | London, UK | Universal banking and payments | FusionBanking platform, open integration via FusionFabric.cloud | Tier 1–2 financial institutions | Cloud-based SaaS |

| nCino | Wilmington, USA | Lending and workflow automation | Built on Salesforce; SME and commercial banking automation | Commercial banks, credit unions | SaaS |

| Forbis (FORPOST) | Vilnius, Lithuania | Regional banking solutions | Account management, payments, and deposits | Community banks in CEE and CIS | SaaS |

| Novatti | Melbourne, Australia | Digital payments and branchless banking | Card issuing, remittance, and payment gateway | PSPs, digital banks, enterprises | SaaS |

How SDK.finance Stands Out

SDK.finance combines the speed of a ready-made platform with the freedom of source code ownership. Its ledger-based architecture, 470+ APIs, and modular setup make it suitable for building or replacing digital banking cores, from wallets and neobanks to payment and super app infrastructures.

Click here to find out more about the digital retail banking software solution and how it can help your business unlock new opportunities.