Mobile banking has moved from convenience to expectation. Nearly 4 in 10 users now rely on a banking app as their primary way to manage money, and by 2026 the global base of online banking users is projected to exceed 4.2 billion. Real-time payments, biometric login, AI-driven insights, embedded finance – features that felt futuristic three years ago are now table stakes.

Building a competitive mobile banking app in 2026 means building a financial operating system for someone’s daily life – one that’s fast, secure, personalized, and ready to scale. The challenge is that doing this from scratch is expensive and slow, with significant engineering investment required before a single user sees the product.

In this guide, we cover the must-have features, architecture decisions, development process, common pitfalls, and realistic cost expectations for mobile banking app development. We also show how SDK.finance’s mobile banking development solution helps banks, neobanks, and fintech companies get to market faster.

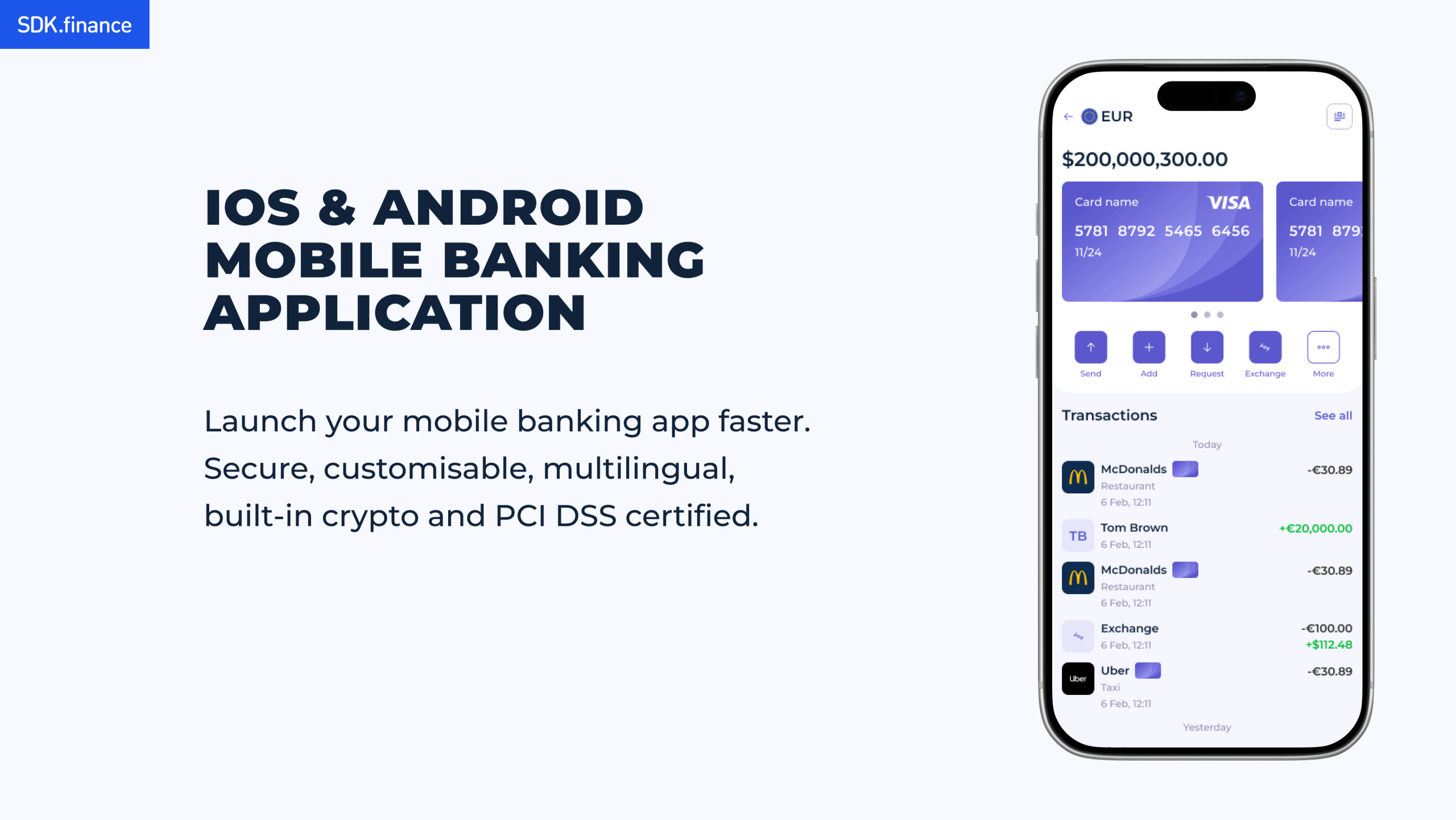

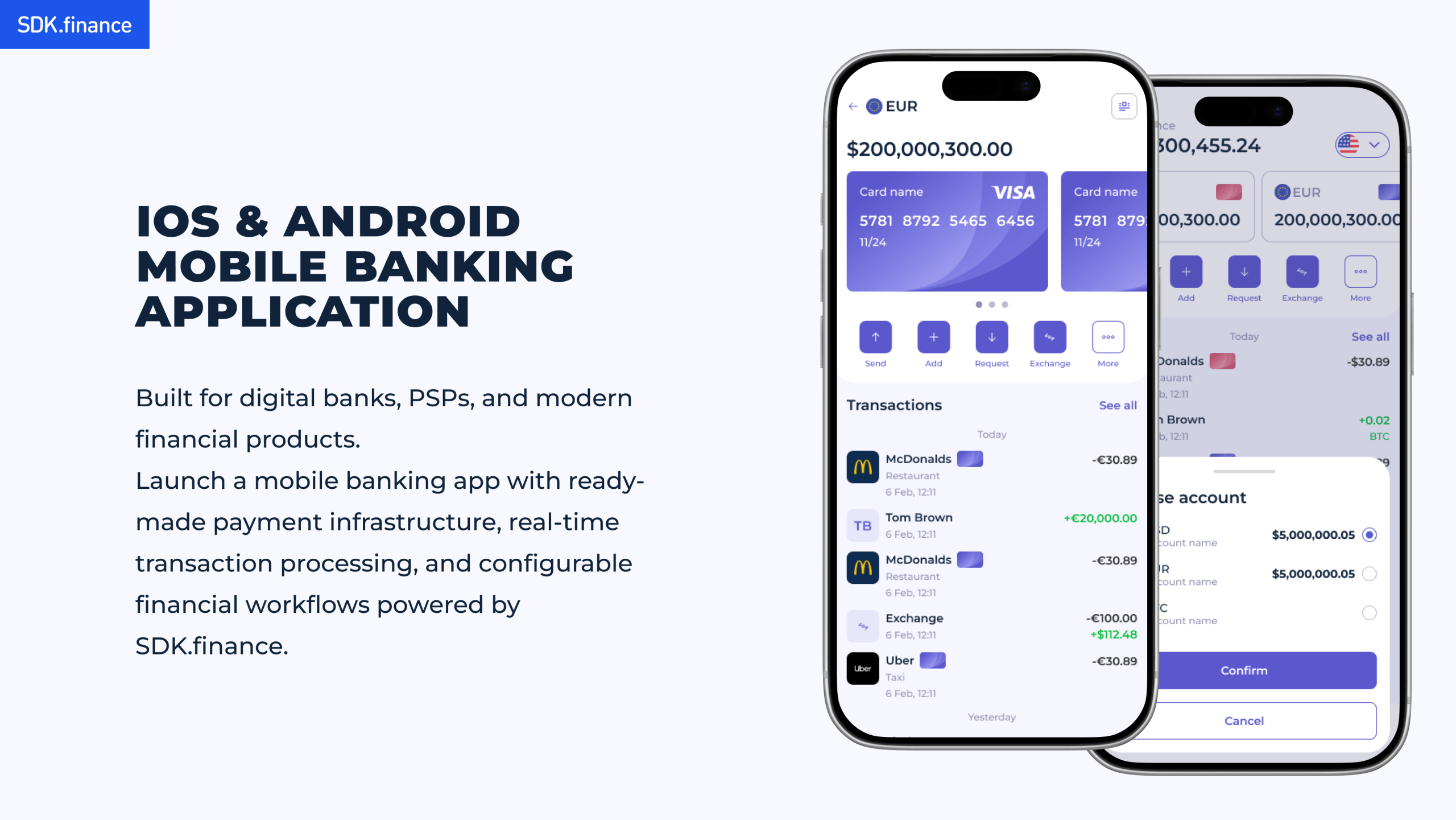

Launch with pre-built backend, APIs, mobile interfaces, and back-office tools.

Explore solutionWhat is Mobile Banking Application?

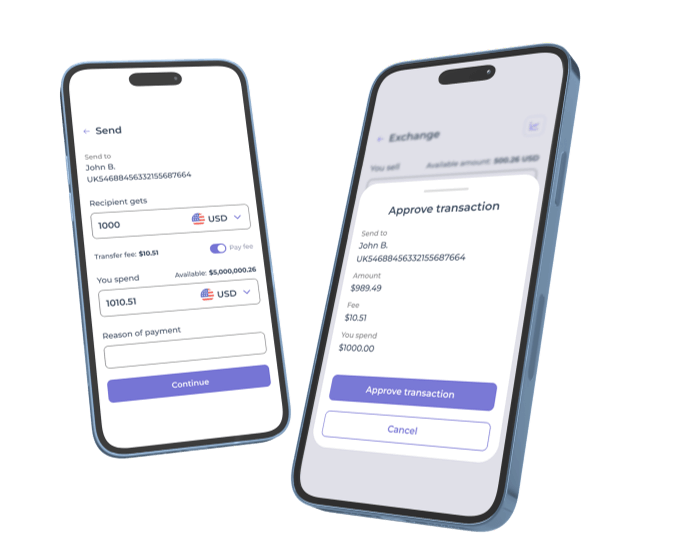

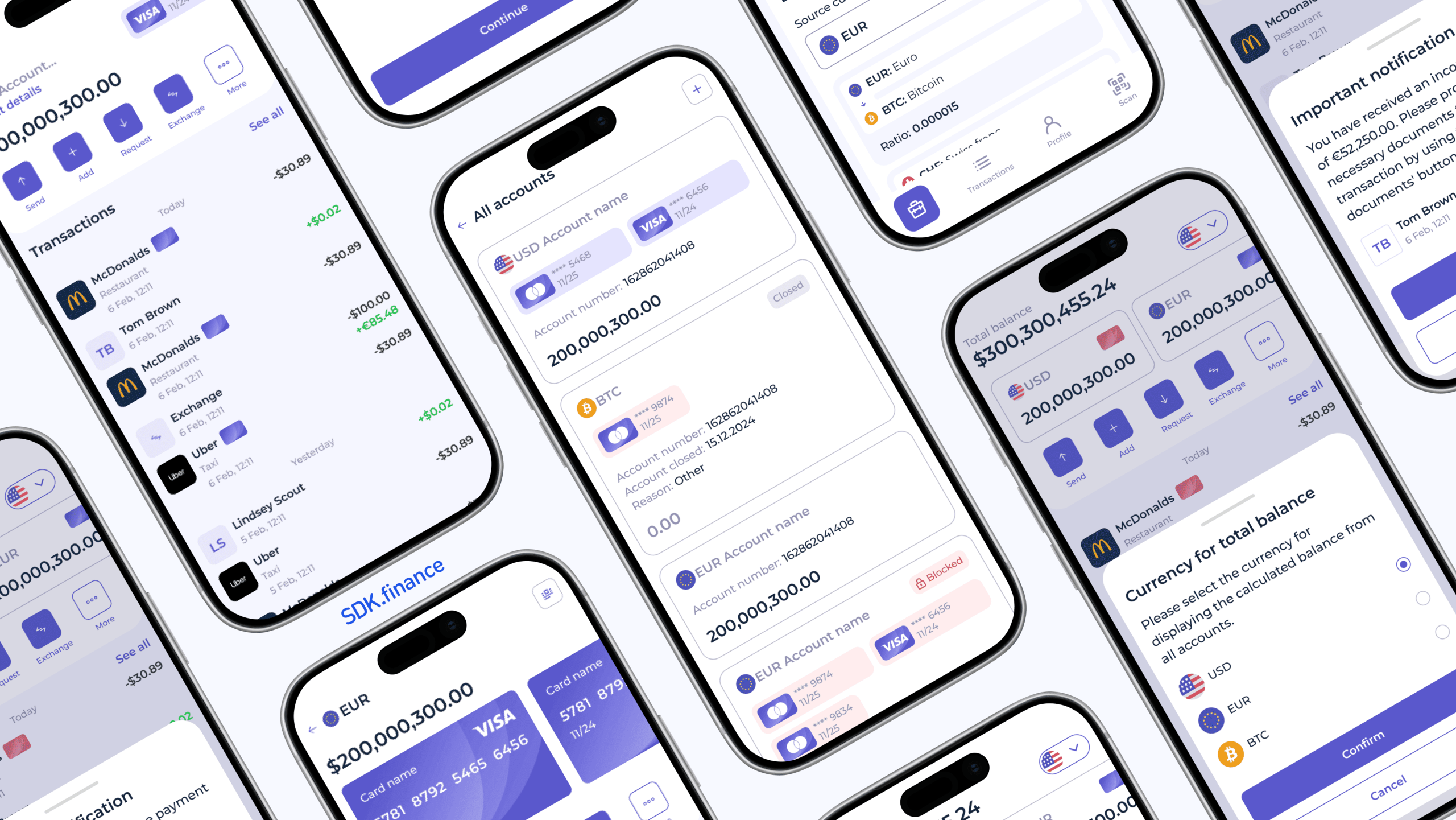

A mobile banking application is a secure digital app that allows customers to access and manage banking services from a smartphone or tablet. It connects to a bank's or fintech's core financial infrastructure and gives customers the ability to check balances, move money, pay bills, manage cards, and interact with financial services without visiting a branch or using a desktop.

Mobile Banking App Interfaces Developed by SDK.finance

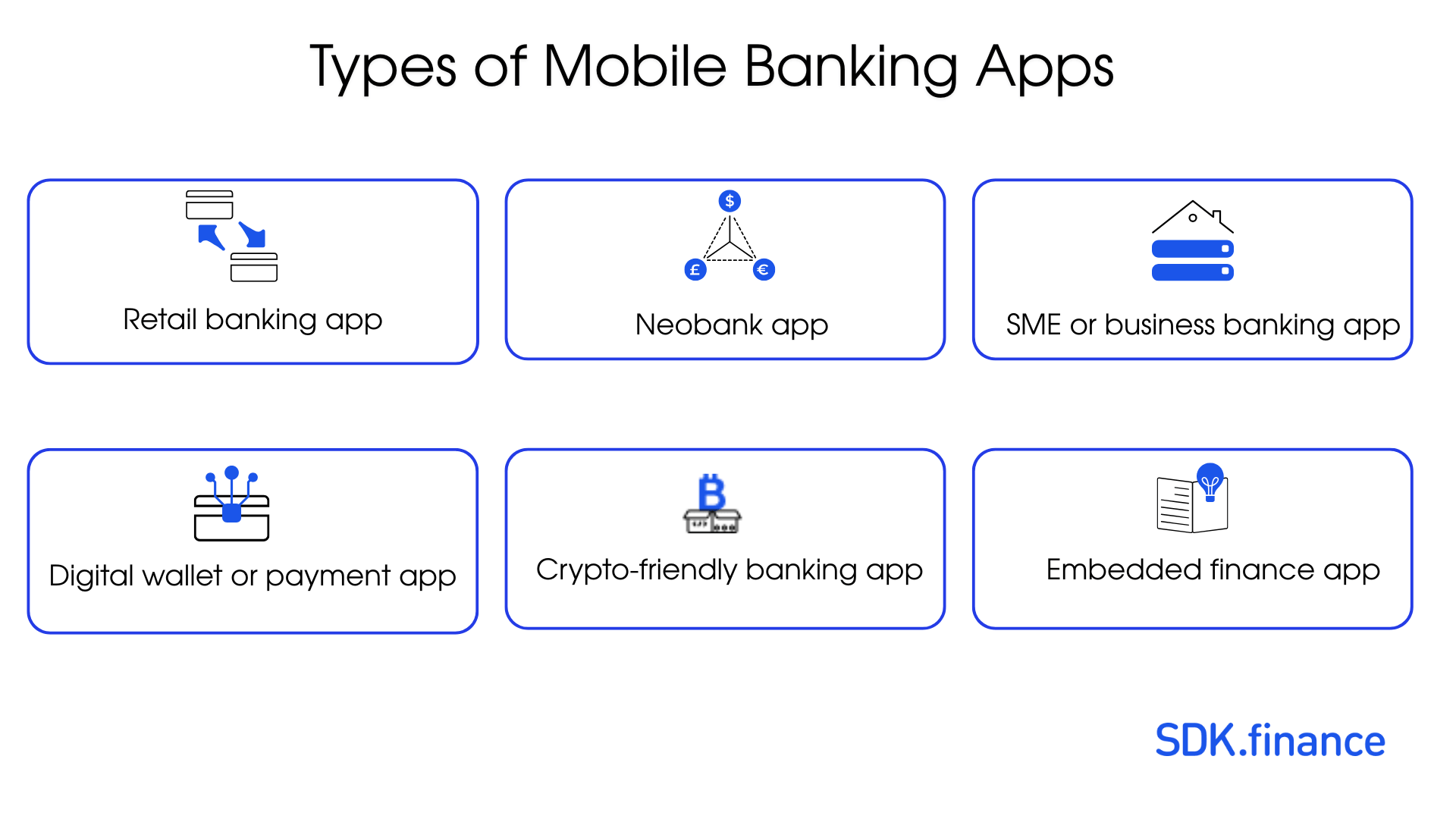

Types of Mobile Banking Apps You Can Build

Mobile banking app development can take different forms depending on the target audience, license model, and product scope. The most common types include:

- Retail banking app: for individual customers who need account access, transfers, card management, bill payments, and notifications.

- Neobank app: a branchless, mobile-first banking product with fast onboarding, accounts, cards, payments, budgeting tools, and FX features.

- SME or business banking app: for companies and merchants that need business accounts, roles, approvals, invoicing, payroll, and reporting.

- Digital wallet or payment app: focused on stored value, P2P transfers, merchant payments, cards, fees, limits, and transaction processing.

- Crypto-friendly banking app: combines fiat accounts with crypto-linked balances, fiat-to-crypto flows, digital asset wallets, and card-connected spending.

- Embedded finance app: adds accounts, wallets, payouts, cards, lending, or insurance inside an existing non-financial product.

- White-label mobile banking app: a ready software foundation that can be branded, configured, and customized for faster launch.

For banks and fintech companies, choosing the right app type early helps define the required features, backend architecture, compliance workflows, and provider integrations.

Trends in Mobile Banking App Development 2026

Mobile banking apps are evolving from simple account-access tools into intelligent, real-time financial platforms. In 2026, the strongest products combine smooth UX with secure backend infrastructure, integrations, compliance workflows, and scalable transaction processing.

AI-powered personal finance

AI is becoming a customer-facing feature in mobile banking apps. Instead of only showing transaction history, apps can analyze spending, detect unusual activity, suggest savings goals, and provide proactive financial insights.

Example: Bank of America’s AI chat-bot Erica has surpassed 3 billion client interactions, showing how AI assistants can become a core engagement layer in digital banking.

Real-time payments and instant feedback

Users expect instant payment confirmations, real-time balance updates, live exchange rates, card controls, and push notifications. This requires reliable transaction processing and event-driven backend infrastructure.

Example: Monzo built much of its customer experience around instant notifications, virtual cards, and card freeze controls.

Biometric and passwordless authentication

Face ID, fingerprint login, device binding, and risk-based step-up authentication are now standard. The trend is moving toward continuous session security, not just login protection.

Hyper-personalized banking

Mobile banking apps increasingly personalize home screens, shortcuts, recommendations, insights, and notifications based on user behavior, account type, and financial profile.

Embedded finance and ecosystem expansion

Banking apps are becoming broader financial platforms, combining payments, cards, lending, insurance, investments, and sometimes crypto-friendly features in one experience.

Open banking and third-party integrations

API-first architecture and open banking allow users to connect accounts, aggregate balances, initiate payments, and share financial data across services.

Multi-currency and cross-border banking

Users expect mobile apps to support multi-currency accounts, transparent FX, and low-cost international transfers without leaving the banking experience.

Example: Revolut’s multi-currency experience shows how FX and international payments can become core mobile banking features.

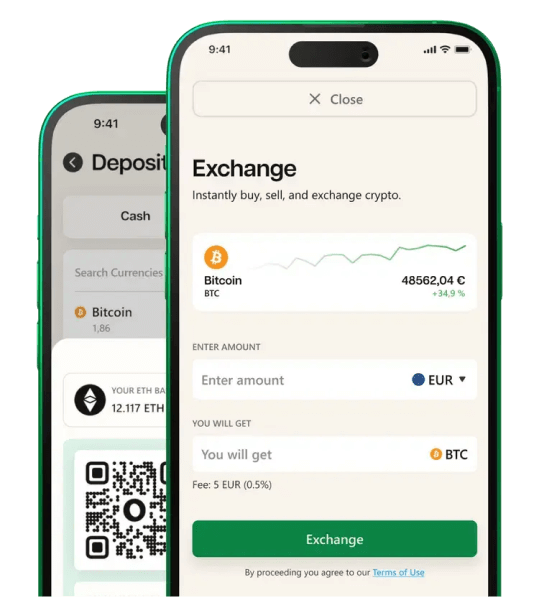

Crypto-friendly digital finance

For selected customer segments, crypto-linked balances, fiat-to-crypto flows, and digital asset wallets are becoming part of mobile finance products.

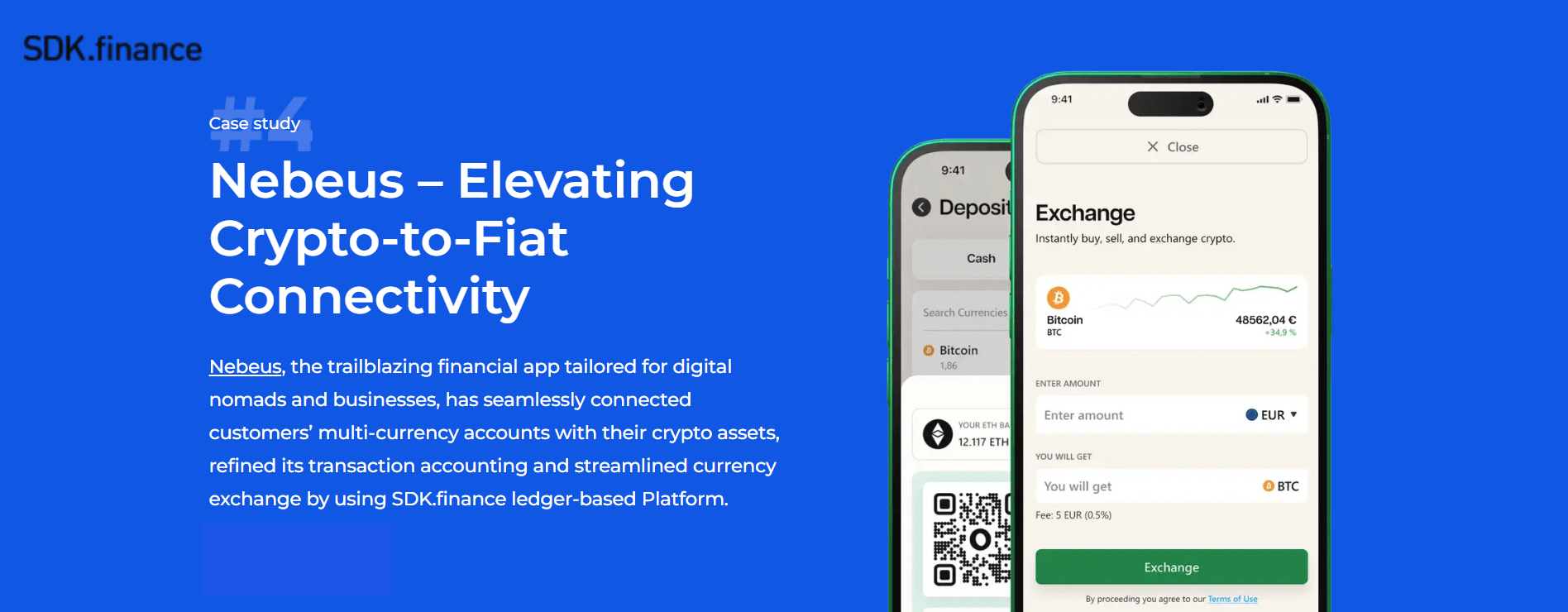

Example: Nebeus used SDK.finance software as the foundation for a crypto-friendly mobile banking app connecting fiat accounts and digital assets.

Nebeus crypto-friendly mobile banking app with built-in crypto-to-fiat exchange, developed on the SDK.finance platform

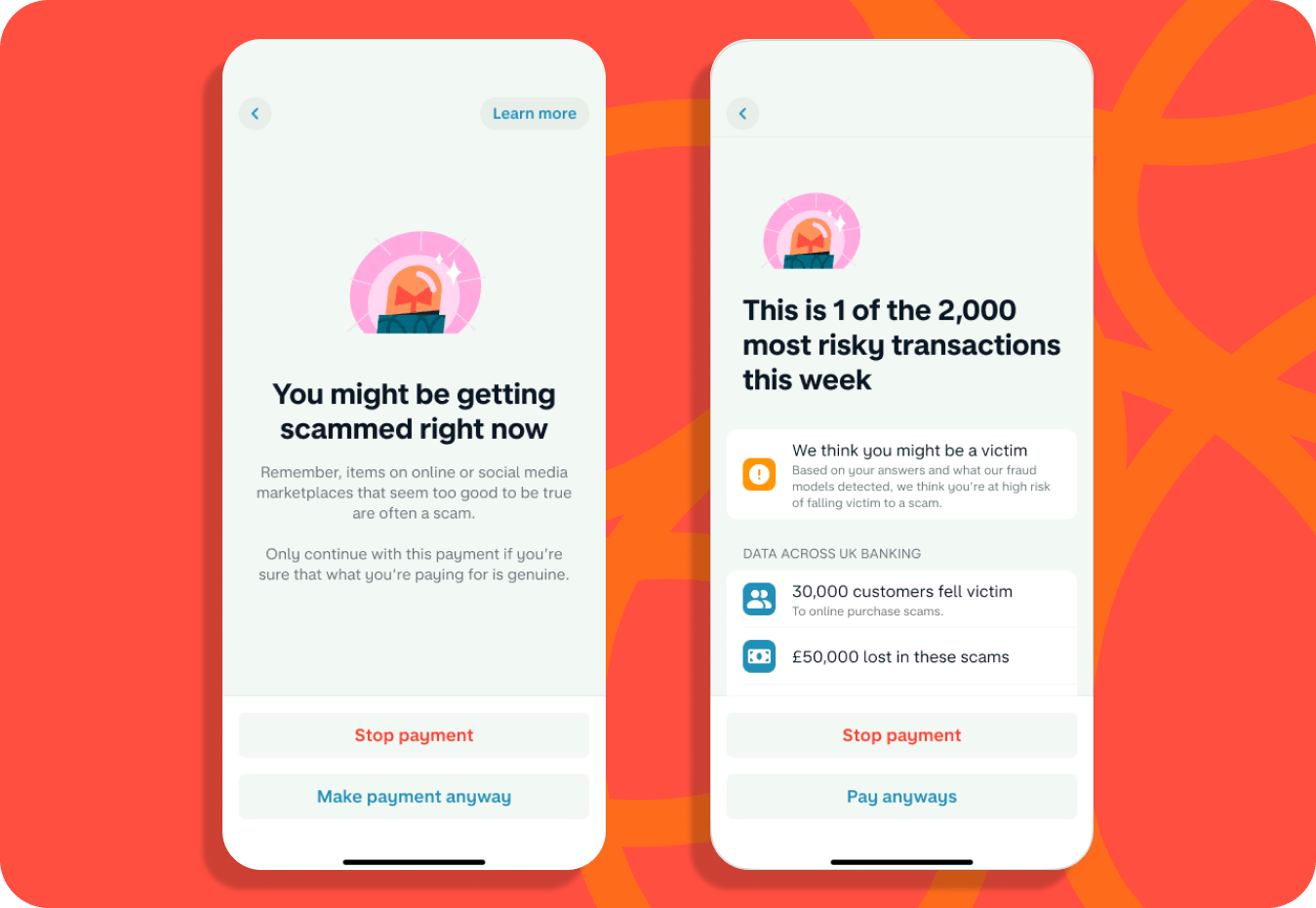

Fraud detection and proactive security

Modern apps need visible security features: suspicious activity alerts, transaction monitoring, instant card freeze, device checks, and step-up authentication.

Example: Monzo lets users freeze cards and report suspicious transactions in-app.

Scalable backend and API-first infrastructure

A polished UI drives adoption, but the backend determines reliability. Mobile banking apps need ledger-grade transaction processing, APIs, back office, reconciliation, compliance workflows, and provider orchestration.

Example: SDK.finance provides 570+ APIs, back-office tools, ledger-based transaction processing, SaaS delivery, and source-code licensing for building mobile banking products faster.

Faster launch with ready mobile banking platforms

More banks and fintechs use ready mobile banking app development platforms instead of building every layer from scratch. This reduces time-to-market and lets teams focus on customer experience, compliance, and growth.

Example: SDK.finance helps companies launch mobile banking, wallet, payment, and crypto-friendly products faster with ready core software infrastructure.

Benefits of Mobile Banking Apps

Benefits for users

Mobile banking apps offer numerous advantages to users, including:

- 24/7 access to banking services

- Convenience of managing finances on-the-go

- Real-time account updates and notifications

- Easier budgeting and expense tracking

- Faster and more secure transactions

Benefits for banks

Banks also reap significant benefits from mobile banking apps:

- Reduced operational costs

- Improved customer engagement and loyalty

- Enhanced data collection for personalized services

- Increased cross-selling opportunities

- Expanded customer base through digital channels

Features of a Mobile Banking App

To compete in today’s digital banking market, banks, neobanks, and fintech companies need more than a basic account-access app. A modern mobile banking app should combine everyday banking functions, secure payments, strong authentication, real-time notifications, and engagement tools in one smooth mobile experience. Below are the key features to consider when planning mobile banking app development.

| Category | Feature | Description |

|---|---|---|

| Account & banking | Account management | View balances, account details, transaction history, and statements in real time. |

| Multi-currency accounts | Hold, manage, and switch between accounts in different currencies. | |

| Card management | Issue, freeze, unfreeze, set limits, and manage virtual or physical cards. | |

| Onboarding & KYC | Register users, verify identity, and collect documents in-app. | |

| Notifications | Send real-time alerts for transactions, security events, and account activity. | |

| Security | Biometric authentication | Enable Face ID and fingerprint login for secure access. |

| Two-factor authentication | Add OTP or authenticator app protection for sensitive actions. | |

| Session & device management | Manage active sessions, trusted devices, and automatic timeouts. | |

| Fraud monitoring | Detect suspicious activity and trigger alerts or additional verification. | |

| Payments | Fund transfers | Support transfers between own accounts, users, and external accounts. |

| Bill payments | Pay bills, schedule recurring payments, and manage payees. | |

| P2P payments | Send instant transfers by phone number, email, or username. | |

| International transfers | Support cross-border transfers with FX rates and transparent fees. | |

| Apple Pay / Google Pay | Enable contactless payments through mobile wallet integration. | |

| Engagement | Budgeting tools | Categorize spending, track expenses, and set budget limits. |

| Personalized insights | Provide AI-driven spending analysis and financial recommendations. | |

| In-app support | Offer live chat, chatbot support, and ticket management. | |

| Advanced | Open banking connectivity | Connect third-party accounts and services for a unified financial view. |

| Crypto integration | Support selected digital asset operations and fiat-to-crypto flows. | |

| Embedded finance | Add lending, insurance, BNPL, or other financial products in-app. | |

| AI financial assistant | Provide conversational guidance, smart suggestions, and voice-enabled support. |

Step-by-Step Mobile Banking App Development Process

Based on SDK.finance’s experience building banking software and mobile applications, one of the most common mistakes companies make is underestimating the full complexity of mobile banking app development. What users see – the clean interface, instant balance, one-tap transfer – is only the visible surface of a deeply complex system. The real engineering challenge is the backend: a financial software stack that handles transaction logic, account ledgers, fee calculation, compliance controls, currency management, role-based permissions, audit trails, and integrations with payment providers and KYC systems.

That backend determines whether the product is stable under load, secure under attack, and compliant under regulatory scrutiny.

For companies evaluating how to build, there are three common approaches:

- Building from scratch with an in-house team gives maximum control, but requires deep fintech domain expertise, takes significantly longer, and carries the highest upfront cost.

- Outsourcing to a specialized FinTech software company is faster, but only if the partner has genuine banking infrastructure experience, not just mobile development skills.

- The third option, increasingly common, is starting from a ready mobile banking platform and customizing it to fit the brand, market, and product requirements. When paired with a source code license, this approach becomes particularly powerful: it gives teams full vendor independence, complete technical control, and a significantly faster path to market compared to building from scratch.

Whichever path you choose, the process follows a similar structure.

Step 1: Define Product Scope and Business Model

Before any technical work begins, the product needs a clear definition. A neobank for freelancers, a corporate expense platform, and a crypto-enabled payment wallet have fundamentally different backend requirements, compliance obligations, and monetization models.

Key decisions at this stage:

- Target user segment and geography

- Core financial operations the product must support

- Supported currencies and markets

- Revenue model: fees, subscriptions, FX margins, lending

- Regulatory environment that applies

Step 2: Plan Licensing, Compliance, and KYC/AML

Mobile banking apps operate in a regulated environment. Compliance is not a feature to add later; it is a structural requirement that shapes the backend architecture from day one.

This step covers:

- Identifying required licenses for target markets

- Defining KYC and KYB verification flows

- Planning AML monitoring and transaction screening

- Data residency, privacy, and payment data security requirements

- Audit trail and reporting obligations

Getting this right early prevents costly architectural rework and delays during regulatory approval.

Step 3: Choose Backend and Technology Foundation

This is the most consequential technical decision in the entire project. The backend is where transaction reliability, security, scalability, and compliance are either built in or absent. Building it from scratch requires assembling every component: ledger logic, account structures, fee engine, transaction management, API layer, back-office tooling, and provider integrations. This can add 12 to 24 months of foundational engineering before actual product work can begin.

A ready mobile banking development platform like SDK.finance reduces this burden significantly by providing account and wallet infrastructure, transaction processing, 570+ APIs, back-office portal, provider integration logic, and mobile and web interfaces out of the box. Teams can focus development effort on user experience and market-specific features rather than rebuilding infrastructure that every financial product needs. SDK.finance is available as SaaS for faster launch or as Source Code for teams that need full technical ownership.

Step 4: Design Mobile Banking Architecture

With the technology foundation in place, the architecture team defines how all components connect and scale. For a mobile banking product, this means designing for transaction consistency, real-time event processing, low-latency API responses, and horizontal scalability.

Critical architecture decisions include:

- Event-driven design for real-time notifications and transaction updates

- Multi-device session management and token security

- Integration layer for payment providers, card processors, and KYC vendors

- Clear separation between core financial logic and product-facing APIs

Poor architecture decisions at this stage become expensive to fix once the product is live and processing real transactions.

Step 5: Create UI/UX and Customer Journeys

With the backend architecture defined, the product and design team focuses on the mobile experience. Mobile banking UX must make complex financial operations – transfers, currency exchange, card management, onboarding, KYC – feel simple and trustworthy.

The design process should cover:

- Onboarding and identity verification flow

- Core transaction screens and payment initiation

- Card management and account controls

- Accessibility and localization requirements

- Error states, empty states, and offline handling

UX quality in a banking app is measured by conversion, trust, and task completion, not visual style alone.

Step 6: Integrate Payments, Cards, KYC, and Providers

A mobile banking app is only as capable as the integrations behind it. This step covers connecting the backend to the external services the product depends on and doing it in a way that is reliable, maintainable, and extensible.

Typical integrations include:

- Payment providers and banking rails for deposits, withdrawals, and transfers

- Card issuing processors for virtual and physical card management

- KYC and identity verification providers

- FX rate sources for multi-currency operations

- Notification services for SMS, email, and push delivery

Each integration adds complexity. Teams starting from SDK.finance benefit from pre-built integration logic for a range of provider types, reducing the custom development required per integration.

Step 7: Test Security, Transactions, and Operations

Testing a financial application requires more than standard QA. The test plan must cover transaction accuracy under concurrent load, fee calculation edge cases, payment failure and rollback handling, session expiry, and compliance workflow validation.

Security testing for a mobile banking app includes:

- External penetration testing of backend APIs and mobile client

- Certificate pinning and secure local storage validation

- Biometric authentication and session management testing

- Jailbreak and root detection verification

- AML and fraud rule testing under simulated transaction scenarios

For a regulated financial product, security sign-off is not optional; it is a prerequisite for launch. A mobile banking app should be built on infrastructure that supports strong data protection, secure payment processing, and audit-ready operations. This is why certifications and compliance readiness matter:

- PCI DSS helps address secure payment data handling,

- ISO 27001:2022 confirms a structured information security management approach,

- GDPR readiness is essential for protecting personal data and supporting privacy obligations in European and international markets.

SDK.finance supports this security-first approach with PCI DSS certification, ISO 27001:2022 certification, GDPR-ready processes, role-based access control, audit trails, and back-office visibility for operational monitoring.

Step 8: Launch MVP, Monitor, and Scale

A controlled MVP launch to a limited user group allows the team to validate real-world performance, catch integration issues that did not surface in testing, and gather early user feedback before scaling. Monitor transaction success rates, API response times, and error rates from day one.

Post-launch priorities include:

- Transaction monitoring and anomaly alerting

- Iterating on onboarding and core flows based on real usage data

- Expanding the feature set based on validated user needs

- Scaling infrastructure ahead of user growth

- Maintaining compliance as regulations evolve

The best mobile banking products are built iteratively. Launch is a milestone, not a finish line.

Key Challenges of Developing a Mobile Banking App

Building a mobile banking app surfaces challenges that most software projects never encounter. Regulatory obligations, financial accuracy, security expectations, and integration complexity make mobile banking development significantly harder than building a standard consumer app. These are the challenges teams most often underestimate.

Regulatory compliance

Financial products operate under strict and constantly changing regulation. Depending on the target market, a mobile banking app may need to comply with PCI DSS, PSD2, GDPR, AML requirements, local central bank rules, data residency obligations, and consumer protection laws at the same time.

The challenge is not only meeting these requirements at launch. Regulations change, and the architecture needs to adapt without requiring a rebuild. Teams that treat compliance as a late-stage checklist usually face the most expensive rework.

Reliable financial backend

The backend of a mobile banking app is a financial system, not a standard web application with a database. It must process concurrent transactions accurately, enforce fee and limit rules, maintain audit trails, and recover from partial failures without leaving account balances incorrect.

Building this from scratch requires engineers who understand ledger design, transaction atomicity, reconciliation, and the operational realities of live financial systems. This expertise is scarce, expensive, and often underestimated.

Security at every layer

Security is not a feature; it is a systemic requirement. The backend must protect against API abuse, session hijacking, privilege escalation, and data exposure. The mobile client must resist reverse engineering, man-in-the-middle attacks, and compromised devices. The integration layer must manage credentials and keys securely across providers.

This requires dedicated security architecture, penetration testing, and ongoing vulnerability management. In financial software, one exploitable weakness can create regulatory, reputational, and financial consequences.

KYC, AML, and identity verification

Onboarding in a regulated financial product is not a simple registration flow. It can involve document verification, liveness checks, sanctions screening, PEP checks, risk scoring, manual review, and ongoing transaction monitoring.

Complexity increases when the product serves multiple markets or both individual and business customers. Each market and customer type can require different verification rules, provider logic, and audit documentation.

Payment and provider integrations

A mobile banking app depends on external services: payment rails, card processors, KYC vendors, FX providers, notification services, banking partners, and sometimes crypto custody providers. Each integration requires implementation, error handling, reconciliation logic, monitoring, and maintenance as provider APIs evolve.

Managing multiple live integrations is one of the most underestimated operational challenges in mobile banking development.

Scalability under real financial load

As the user base grows, transaction volume can increase quickly and unevenly. The backend must process concurrent transactions consistently, maintain ledger accuracy, send real-time notifications, and keep API response times stable.

Designing for scale from the start requires deliberate choices around database architecture, event-driven processing, caching, observability, and infrastructure scaling. Products that skip this foundation often face expensive re-architecture after launch.

Platform and ecosystem changes

iOS and Android release major updates every year, and financial apps are often affected by changes to biometric APIs, secure storage, notification handling, app store rules, and device security requirements. At the same time, payment standards, open banking APIs, and regulatory technical standards continue to evolve.

Maintaining a mobile banking app is an ongoing engineering program, not a one-time project.

Talent and domain expertise

One of the hardest challenges is finding engineers who understand both software development and financial systems. FinTech backend development requires knowledge of ledgers, transaction processing, compliance architecture, payment infrastructure, and operational risk.

A platform like SDK.finance helps reduce this dependency by providing ready financial backend infrastructure, APIs, back-office tools, and integration logic out of the box. This lets teams launch a production-grade mobile banking product without building and maintaining every core financial component in-house.

Mobile Banking App Development Cost and Timeline

The cost and timeline of mobile banking app development depend on the same core factor: how much backend financial infrastructure needs to be built from scratch. A simple UI prototype can be created relatively quickly, but a production-ready mobile banking app needs much more than screens: ledger logic, account infrastructure, transaction processing, KYC/KYB workflows, provider integrations, back-office tools, security controls, and compliance-ready operations.

In 2026, a realistic budget can start from $20,000-$60,000 for a mobile banking app UI with simple flows and reach $800,000-$2,000,000+ for a custom build from scratch. Timeline can range from 1-2 months for a prototype to 18-36 months for a full in-house custom build.

| Project type | Estimated cost | Estimated timeline | Best for |

|---|---|---|---|

| Mobile banking app UI with simple flows | $20,000-$60,000 | 1-2 months | Clickable prototype, basic UI screens, onboarding flow, account overview, simple transfer screens |

| Mobile banking app with backend and core features | $100,000-$1,500,000+ | 6-18 months | Account access, balances, transfers, cards, KYC, multi-currency support, back office, payments, fraud monitoring, compliance workflows |

| Custom build from scratch | $800,000-$2,000,000+ | 18-36 months | Proprietary backend, complex integrations, custom ledger, advanced compliance and scaling needs |

| Ready platform-based launch | From $100,000-$300,000+ | 3-10 months | Faster launch using pre-built core infrastructure, APIs, back office, mobile/web interfaces, and provider integration logic |

What affects mobile banking app development cost and timeline?

The final budget and schedule depend on several factors:

- Feature scope: account management, payments, cards, KYC, budgeting tools, crypto features, open banking, or AI insights.

- Backend complexity: ledger logic, transaction processing, fees, limits, reconciliation, reporting, and back-office operations.

- Security and compliance: PCI DSS, ISO 27001:2022, GDPR readiness, KYC/AML workflows, audit logs, penetration testing, and fraud monitoring.

- Third-party integrations: card issuing, payment gateways, banking rails, KYC providers, AML tools, FX providers, open banking, and notifications.

- Platform choice: native iOS/Android, cross-platform development, SaaS platform, source-code license, or fully custom backend.

- Team model: in-house development, outsourcing, fintech software vendor, or ready mobile banking app development solution.

A polished mobile interface is important, but most of the cost and development time sits in the backend. Transaction logic, account infrastructure, compliance workflows, provider integrations, and operational tools are what make a mobile banking app reliable in production.

How to reduce cost and launch faster

The fastest way to reduce both cost and time-to-market is to avoid rebuilding core banking infrastructure from zero. A ready mobile banking app development solution like SDK.finance provides core backend functionality, 570+ APIs, back-office tools, account and wallet infrastructure, transaction processing, and mobile/web interfaces out of the box.

This allows teams to spend less budget on commodity infrastructure and more on what differentiates the product: customer experience, provider partnerships, compliance setup, branding, and go-to-market execution.

That is why many banks, neobanks, fintech companies, and financial institutions choose SDK.finance as the technology foundation for mobile banking app development. Instead of starting from a blank backend, teams can launch from a ready platform and customize it around their market, provider stack, compliance requirements, and product strategy.

SDK.finance: Mobile Banking App Development Solution for Faster Launch

SDK.finance is a ready-to-use fintech software platform built on 15+ years of financial infrastructure engineering. It helps companies launch digital banks, neobanks, wallets, payment products, and embedded finance solutions faster with core infrastructure, 570+ APIs, back office, mobile/web interfaces, and SaaS or source-code delivery for full vendor independence.

With SDK.finance, your team can focus on licensing strategy, customer experience, provider integrations, compliance setup, and go-to-market instead of rebuilding core banking infrastructure from scratch.

Why build your mobile banking app with SDK.finance?

-

Launch faster with ready-made infrastructure. Start with pre-built mobile banking functionality, back-office tools, APIs, and financial workflows instead of designing every core component from scratch.

-

Customize the product around your market. Configure accounts, wallets, currencies, fees, limits, contracts, user roles, onboarding flows, and provider integrations to match your business model.

-

Support fiat, crypto, and digital asset flows. Use SDK.finance’s ledger-based foundation to manage fiat wallets, crypto-linked balances, currency exchange, transaction history, and account-based financial operations in one system.

-

Integrate the providers you need. Use 570+ APIs to connect KYC, AML, payment gateways, card issuing, open banking, FX, crypto custody, liquidity, blockchain infrastructure, banking partners, analytics, and other third-party services.

-

Choose SaaS or source-code delivery. Use SaaS for faster launch with managed infrastructure, or choose the source-code license for full ownership, custom development, deployment control, and 100% vendor independence.

-

Build on secure, compliance-ready infrastructure. SDK.finance is PCI DSS certified, ISO 27001:2022 certified, and GDPR-ready, helping your team meet high security and data protection expectations from the start.

-

Scale with confidence. SDK.finance software powers launched financial products across the US, Canada, the EU, the UK, and MENA, including high-volume payment infrastructure.

-

Use ready mobile and web interfaces. SDK.finance includes mobile/web user interfaces and a mobile banking app demo, so your team can evaluate the customer experience before development begins.

Сase study: launching a crypto-friendly mobile banking app with SDK.finance

Nebeus, a Barcelona-based crypto finance company, used the SDK.finance banking platform as the software foundation for a crypto-friendly mobile banking app that connects fiat accounts with digital assets. The goal was to let users manage multi-currency accounts, link crypto assets to everyday financial flows, exchange between fiat and crypto, and support card-connected spending without building the entire fintech core from scratch.

With SDK.finance, Nebeus gained a ready ledger-based infrastructure for account management, wallet balances, top-ups, withdrawals, transfers, currency exchange operations, and transaction accounting. This helped the team streamline crypto-to-fiat connectivity, improve operational visibility, and reduce the time and cost required to launch and scale the product.

The Nebeus case shows how SDK.finance can support not only traditional mobile banking app development, but also crypto-friendly banking products where fiat accounts, digital assets, cards, and payment flows need to work together in one secure, scalable system.

See the mobile banking app demo

If you want to launch a mobile banking app faster, SDK.finance gives you a strong starting point: the software foundation is already built, configurable, API-driven, and ready to adapt to your market.

Explore the SDK.finance mobile banking app development solution and see how it can help you move from product idea to launch-ready infrastructure faster:

A polished, intuitive UI is essential for user adoption: customers expect a mobile banking app to look modern, feel simple, and make everyday financial actions effortless. But long-term success depends even more on what users do not see: a stable, secure, and scalable backend that keeps balances accurate, transactions reliable, integrations working, compliance workflows auditable, and the entire product ready for growth.

If you want to launch a mobile banking app faster, SDK.finance gives you a ready foundation: core backend infrastructure, APIs, back office, mobile/web interfaces, SaaS delivery, and source-code licensing for full vendor independence.

Book a demo to discuss your mobile banking app development project.

Launch with pre-built backend, APIs, mobile interfaces, and back-office tools.

Explore solution