When it comes to bank transfers in the UK, there are a few options to choose from. Two of which are Bacs and Faster Payments. But which will be more beneficial for your business depends on your customers’ needs, transaction amounts and the necessary speed of the transfers. Here, we outline the features and benefits of Faster Payments vs Bacs and explain what is the difference between them.

Bacs payment: definition

What is Bacs payment?

Bankers Automated Clearing Services (Bacs) is the most popular method for sending and receiving business payments in the UK, typically used to pay salaries, pensions, and bills. Over its impressive 50-year history (founded in 1968) Bacs processed over 78 billion payments. The term Bacs actually refers to the payment network consisting of 27 UK banks and building societies that make up the membership organization.

There are two forms of Bacs payments:

- Direct Credit is used to send payments directly into bank accounts

- Direct Debit collects payments directly from bank accounts.

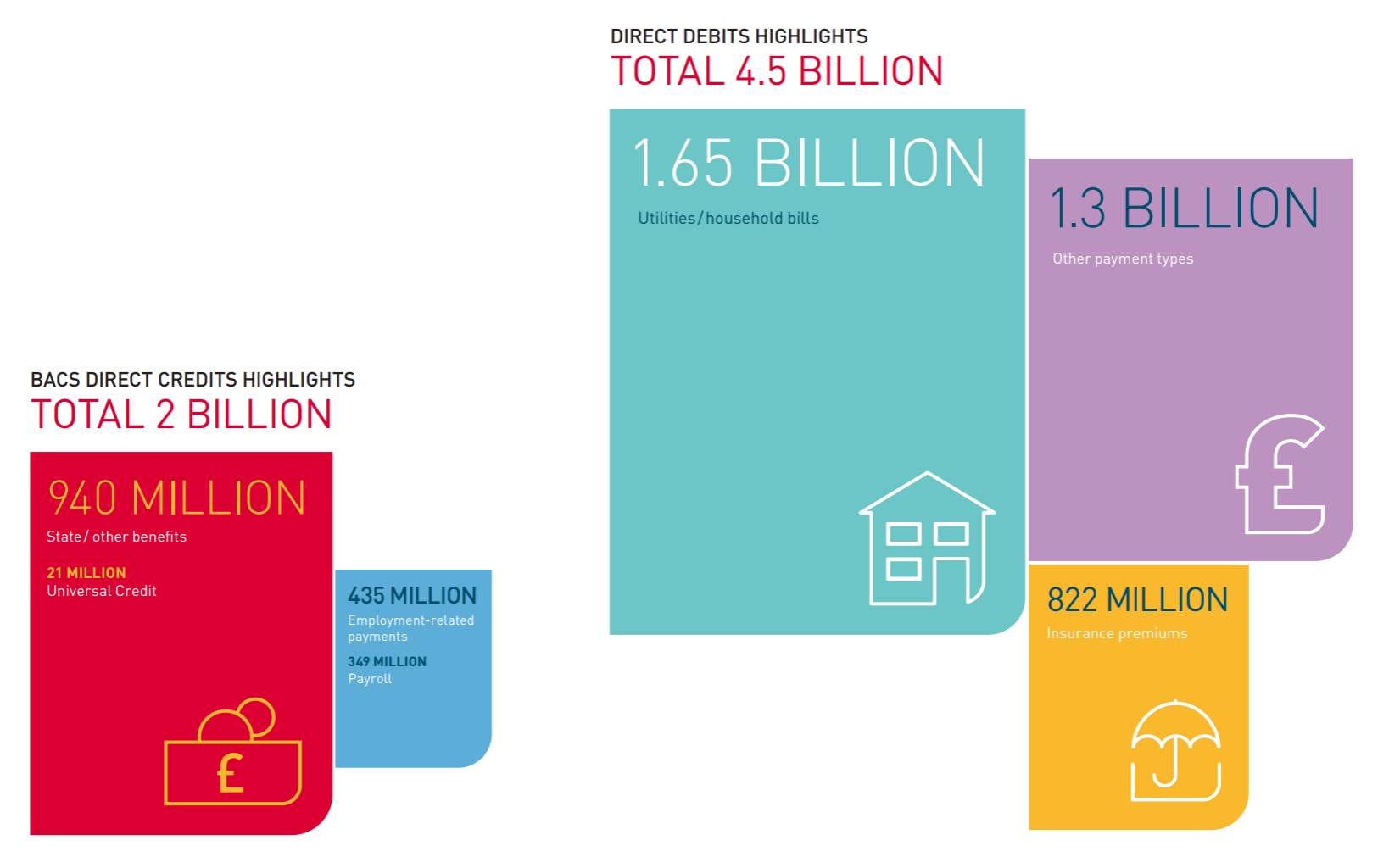

To give you an idea of the numbers involved, check out the stats. In 2019, there were 2 billion Direct Credits and 4.5 billion Direct Debits carried out.

What is Bacs Direct Credit?

Bacs Direct Credit is a tried and trusted option for companies of all sizes to quickly and efficiently send or receive payments. Direct Credits predominantly handle State benefits, such as pensions, tax credits, and various allowances, and include general B2B payments, payrolls, and dividends.

What is Bacs Direct Debit?

Bacs Direct Debit is when a customer instructs their bank to authorize a third party to collect payments from their account for as long as the customer allows. Once the bank receives the authorisation, the authorized organisation can automatically take payments on a regular basis. Direct Debit is usually used for regular and recurring payments such as utilities and household bills, loan repayments, insurance premiums, and subscriptions. 90% of people in the UK have at least one regular Direct Debit payment.

How long does it take to process a Bacs payment?

A payment Bacs takes three business days to clear. If a payment file is submitted to the Bacs system on the first day prior to a cut-off time, a bank can process the file on the second day, and credit the payment to the recipient’s bank account on the third day.

Bacs Direct Credit payments usually arrive by 7am on the third business day. Even though it is an electronic payment system, Bacs transfers only send Monday to Friday.

How safe are Bacs payments?

Bacs has a long-standing reputation for being an incredibly safe and trusted way to collect and make payments. It has a 95%-100% success rate and is renowned for its secure and reliable electronic payments delivery. Bacs uses an SSL encrypted Bacstel-IP system and requires a secure and encrypted password. There’s also a Direct Debit Guarantee that protects customers from any fraudulent payments.

Faster Payments: definition and details

What is Faster Payments?

Faster Payments is a UK banking initiative that enables mobile, internet, and telephone payments to move between customer accounts, usually within a few seconds. Almost all internet and telephone banking payments in the UK are processed through the Faster Payments Service (FPS).

In 2019 alone, the initiative processed 2.4 billion transactions worth £1.9 trillion. With 35 directly connected participant organizations and 400 financial institutions supporting the service, Faster Payments is available to more than 52 million current account holders in the UK.

How long do Faster Payments usually take?

Usually, Faster Payments arrive instantly but can take up to two hours, depending on the service provider. A real-time payment can be made and received 24/7, including bank holidays. Delays may occur if the other bank or building society is not a participant of the Faster Payments Service or if there is confusion over the sender’s identity and additional security checks are needed.

How Faster Payment works. Source: Faster Payments

What is the faster payments transaction limit?

On Febuary 8, 2022, the maximum amount the customers can send via Faster Payments has been quadrupled. So, instead of the previously allowed £250 000, it is now possible to send £1 million using an FPS transfer. However, individual banks and building societies may have their own thresholds and limitations in place for personal and corporate customers. For transfers over the limit, customers need to use Bacs.

How is Bacs different from faster payments?

Faster payments is really faster

Bacs is an older payment system, where payments are transferred directly from one bank account to another, usually taking three working days to clear.

Faster Payments is a banking initiative that enables mobile, internet, and telephone payments to move between customer accounts, usually within a few seconds, living up to its name.

Faster payments works 24/7

Unlike Bacs payments that only work during business days, Faster Payments can be made and received 24/7, including bank holidays. Delays may occur if the other bank or building society is not a participant of the Faster Payments Service or if there is confusion over the sender’s identity and additional security checks are needed.

Faster payments has lower transaction limits

It is possible to send up to £1 million using a Faster Payments transfer, but individual banks and building societies may have their own thresholds and limitations in place for personal and corporate customers. Bacs allows transfers over the £1 million threshold.

How to start using Bacs and faster payments?

How to join the faster payments service?

If you are considering providing real-time payments to your customers, Faster Payments Service outlines the following ways to join this system:

- Directly Connected Settling Participants (DCSPs) – connect directly to the Faster Payments Central Infrastructure to send and receive payments in real-time, 24 hours a day. DCSPs set their own transaction limits and carry out their own settlement with the Bank of England. Connecting to Faster Payments Service as a DCSP provides the fastest service, but it is limited to organizations that handle a high volume of payments and are eligible to open a settlement account at the Bank of England. This option requires a significant investment to build a direct gateway, hire technical experts to implement it, and adhere to initial and ongoing compliance obligations.

- Directly Connected Non-Settling Participants (DCNSPs)– connect directly into the Faster Payments Central Infrastructure via a sponsoring Participant that performs Bank of England settlement on the PSP’s behalf. Companies that are not eligible to open a settlement account at the Bank of England can connect as a DCNSP, but most transactions will take from seconds to several hours because of additional relays. Companies operating as DCNSPs report high transaction costs and more outages as directly connected participants are prioritized.

- Indirect Agency. This option enables a PSP to connect to Faster Paymentsvia a sponsoring Participant, which manages the direct connection on its behalf. Sponsoring Participants provide various options to send and receive Faster Payments, and also perform Bank of England Settlement on the Indirect Agency PSP’s behalf. This option is beneficial for PSPs that find a direct connection is not commercially viable.

FinTechs, smaller banks, and institutions can use the Indirect Agency model to access Faster Payments with APIs without the need for scheme approval. This option provides real-time payments without sacrificing speed and resources.

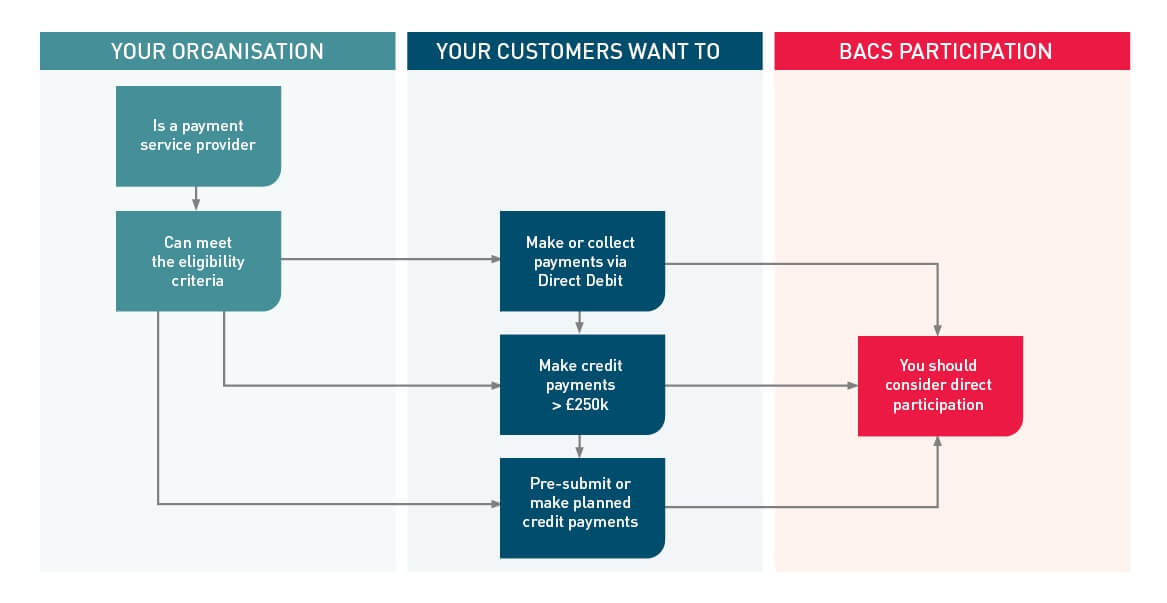

How to become a part of Bacs?

Bacs direct participation is open to banks, building societies, electronic money institutions (EMIs), and payment institutions (PIs) that meet the following eligibility criteria:

- Have a settlement account at the Bank of England

- Carry out business and operate an office in the EEA

- Meet agreed technical and operational requirements, including having an agreement in place with VocaLink (or another provider of approved clearing services), and having an approved trust service

- Be a bank, building society, authorised payment institution or electronic money institution

- Sign a legal document in respect of participation, and of the settlement arrangements

- Pay a share of Bacs costs.

Eligibility criteria. Source

Bacs participants have to abide by clear and transparent governance structure, rules, and procedures.

Bottom line

With a quality core payments software provider, financial institutions can connect to the Faster Payments Servic without long and costly development cycles. SDK.finance enables companies of all sizes to launch their real-time payment products with ease. The list of SDK.finance use cases includes white-label digital retail bank, ewallet, remittance app, payment acceptance software etc.

Contact us directly to learn more about what type of payments software will be perfect for your business needs.