The current financial industry requires a modern solution to make the payment process more convenient and faster. The digital world continues moving forward, therefore in many countries, there is a necessity in starting a payment processing company to meet the changing needs.

According to The McKinsey 2022 Global Payments Report, the payments services industry is rapidly growing, uniting banks and technology providers to create similar seamless and convenient digital experiences. For instance, banks are optimizing their core systems and updating their payment infrastructure, largely in response to the continued rise of online payments, open-banking requirements, and cloud technology. In this article, we explore how to start a payment processing company and provide a ready-made solution to launch your product faster and cost-effectively.

The key definitions to know before starting a payment processing company

There are different payment processing services that finance companies can offer to businesses: payment service provider, payment facilitator, payment gateway, and payment processor. Payment processing fees are an important consideration, as they include various components such as interchange fees and processor fees. That’s why you have to choose what type of service you want to provide. Some payment processors serve only as gateways while others become acquirer banks and are partners with Visa or Mastercard.

For online payments, MPGS (Mastercard Payment Gateway Service) enables businesses to integrate payment processing into their websites and mobile applications. Customers can pay securely using a variety of payment methods, and businesses can manage their payment transactions through MPGS’s online portal.

Mastercard MPGS is a secure solution for fintech companies looking to improve their payment processing capabilities and stay ahead of the competition. Read our article on Mastercard Payment Gateaway Services Integration, to explore how to revoluzionize your payment business.

Within this spectrum, there are two additional payment options – becoming a payment service provider (PSP) or a payment facilitator. Each of these roles necessitates a registration process and is subject to different regulations, which standardize online payment processing activities.

What is payment processing?

What is a payment processing company?

Payment processing companies act as intermediaries between the parties involved in a transaction, including customers, merchants, banks, and payment networks. They offer a range of services that enable businesses to accept payments from customers and manage their payment operations.

What is a payment service provider?

A payment service provider (or PSP) is a third-party company that helps your business with getting digital payments (from credit cards, debit cards, e-wallets, etc). A PSP is responsible for the transaction verification process and helps to accept payments from the customer to the merchants.

What is a payment facilitator?

A payment facilitator is a service provider for retailers. If you need to process payments online, you can use a merchant account from a payment facilitator, where funds from completed transactions are deposited into the merchant's account after a series of authorizations and confirmations with card networks and issuing banks. There are two types of retail accounts: PSP and ISO (Independent Sales Organization).

Comparison of Payment Processing Company, Payment Service Provider, and Payment Facilitator

| Aspect | Payment Processing Company (Processor) | Payment Service Provider (PSP) | Payment Facilitator (PayFac) |

|---|---|---|---|

| Definition | Technical infrastructure for authorisation, clearing, and settlement of transactions. | Service layer that gives merchants access to multiple payment methods. | Aggregator that allows sub-merchants to operate under its master merchant account. |

| Role | The “engine” of payments: directly connects with banks and card networks. | The “front” for merchants: provides integration, risk management, reporting, and dashboards. | Handles onboarding and compliance for small merchants. |

| Merchant Account | Merchants need their own acquiring bank/merchant account. | PSP connects merchants to acquirers. | Sub-merchants use the PayFac’s master merchant account. |

| Regulation | Highly regulated (PCI DSS, Visa/Mastercard rules). | Regulated as an intermediary, depending on jurisdiction. | Stricter obligations, since the PayFac bears liability for sub-merchants. |

| Examples | FIS, Worldpay, Global Payments. | Stripe, Adyen, Checkout.com. | Square, PayPal Here, Stripe Connect. |

| Target Users | Banks and large enterprises needing infrastructure scale. | SMEs and enterprises that need convenient access to digital payments. | Small and micro-merchants looking for fast onboarding. |

In short: a processor is the backend infrastructure, while a PSP is the service layer built on top of processors for merchants.

Understanding Payment Processing

Payment processing is a critical component of any business that accepts payments from customers. It involves the transfer of funds from the customer’s account to the business’s bank account, requiring a secure and efficient system to facilitate this process. Understanding payment processing is essential for businesses to manage their cash flow, reduce the risk of fraud, and provide a seamless payment experience for their customers.

Components of Payment Processing

Payment processing involves several components that work together to enable secure and efficient transactions. These components include:

- Payment Gateway: A payment gateway is a software application that acts as a bridge between the customer’s payment method and the business’s payment processor. It encrypts the transaction data and ensures that it is transmitted securely to the payment processor.

- Payment Processor: A payment processor is a company that processes payment transactions on behalf of the business. It verifies the customer’s payment information, checks for sufficient funds, and transfers the funds to the business’s account.

- Acquiring Bank: An acquiring bank is a financial institution that provides the business with a merchant account. It receives the payment request from the payment processor and transfers the funds to the business’s account.

- Issuing Bank: An issuing bank is a financial institution that issues credit cards or debit cards to customers. It verifies the customer’s account status and checks for sufficient funds before approving or declining the transaction.

- Card Network: A card network is a system that facilitates the transfer of funds between the issuing bank and the acquiring bank. It provides a secure and efficient way to process payment transactions.

- Merchant Account: A merchant account is a type of bank account that allows businesses to accept credit card payments. It is provided by the acquiring bank and is used to receive payment from customers.

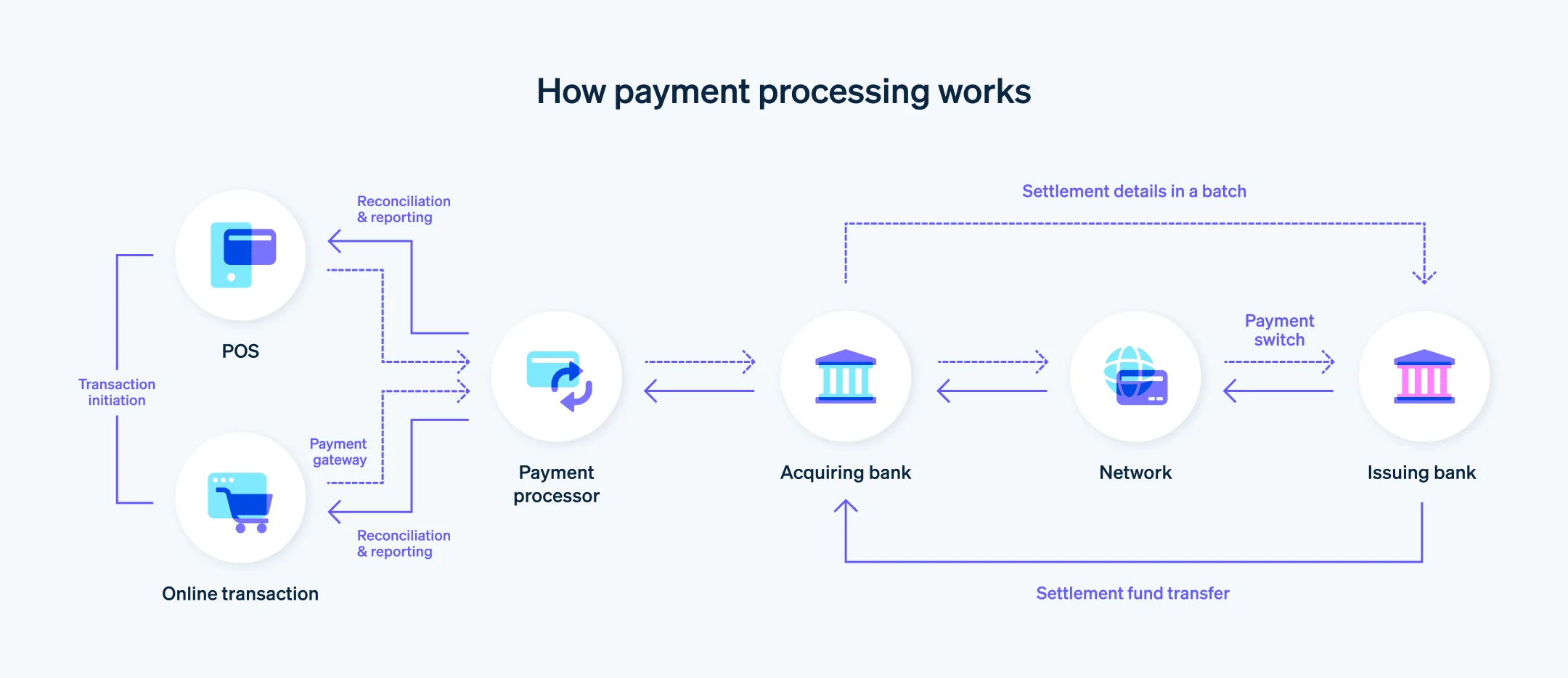

How does a payment processor work?

To understand how to start a payment processing company it is essential to clarify the payment processor workflow and the transaction process.

At first sight, payment processing is a simple automated set of actions that needs only 3 seconds to be done. In fact, it is a multi-step process that consists of customer authentication, authorizing, and settling the payment. The payment processor manages the credit card transaction, working as the mediator between the merchant and the financial institutions involved.

Source: Stripe

Let`s observe the payment processing in more detail.

- Using the card by the customer for online payment processing.

- Transmitting an amount of money to the payment processing service provider.

- Sending the information to the card associations.

- Checking the request by an issuing bank.

- Receiving confirmation (or cancellation) of the transaction.

- Sending the response to the provider by card associations.

- Forwarding the response to the merchant by an online payment service provider.

- Approving (or delaying) the credit and debit cards.

This is how payment processing works indeed, consisting of many steps to be done. Therefore, it is essential to provide an uninterrupted, stable process to prevent any problems with the transaction.

What are the main features of a decent payment processing solution?

It is important to clarify the key features of a standalone digital app to understand how to become a payment processor. A payment processing solution is a reliable service that must have the following features: easy integration, security, convenient transaction processing, detailed reporting, customer and merchant onboarding, payment initiation, and acceptance.

SDK.finance payment acceptance software features

You can start your business by providing a complete stack of online and offline payment acceptance services for merchants using the payment Platform SDK.finance, without having to start from scratch. We offer the software to build a world-class payment service provider business. It serves different types of businesses – from online shops to marketplaces to brick-and-mortar stores.

SDK.finance payment Platform offers such features:

| Feature | SDK.finance fintech Platform |

| Customer onboarding: | Online account creation, document uploading |

| Transactions management: | Transaction history, view details of each transaction, transaction history export, transactions on the map |

| Refunds initiation: | Initiating refund transactions on the customer’s demand |

| Merchant’s digital wallet: | Opening a digital wallet for the merchant’s personal use |

| Payment acceptance: | In-store payments, online payments, tips acceptance, and bill payment processing |

| Online POS: | Online POS registration, web-payments acceptance, configurable checkout page |

| Regular payouts: | Receiving settlement amounts from the merchant’s |

| Receipts generation: | Manually, from the transaction history, via sending email receipts after the transaction |

| Roles & permissions management: | Individual, merchant, administrator, accountant, compliance manager |

View the demo video of the SDK.finance Platform to see how you can streamline transaction management and guarantee financial compliance using our robust FinTech Platform:

How to start a payment processing company?

Starting a payment processing business can be a complex process, but we will outline the steps to help you get started.

Building the payment processing software: start from scratch or get it off the shelf?

Building payment processing software from scratch can be a daunting task, as it requires a lot of your resources and may take a few years to complete. You will also need server infrastructure and robust security measures in place, and an expert development team capable of handling a complex fintech project (and plenty of time to implement your project from the ground up).

If you’re into cost- and time-efficiency, using a pre-developed white-label solution might be a more beneficial way to go. It enables you to brand and customize the ready software according to your product needs and seriously accelerate the release. In addition, working with a reliable vendor can help save your team resources, and costs, plus reduce CAPEX.

If you’d like to start earning revenue as soon as possible rather than spending months or years on a from-scratch project, let us guide you through the process of building a payment processing system using SDK.finance Platform as a foundation. With our payment acceptance solution, you can start growing your revenue by providing a complete stack of online and offline payment acceptance services for merchants faster. Read this article to explore how to build a payment solution like Stripe.

How to develop a payment processing system with the SDK.finance platform?

Setting up the infrastructure and services

This step involves configuring environments, such as development, pre-production, and production, to ensure a smooth and efficient development process. It also involves setting up services that will aid in the deployment, monitoring, and maintenance of your e-wallet platform. By taking the time to configure these components correctly, you’ll create a strong foundation for the success of your e-wallet platform.

Configuring development, pre-production, and production environments

SDK.finance infrastructure consists of 3 servers: developers instance (for development and testing of the software); production instance (live operation server with end-users and real operations); pre-production or Sandbox (infrastructure with the same specs as the production instance used for debugs of integrations with third-party components).

Requirements of the instance for production and test environments

- CPU – 1

- RAM – 2 GB

- SSD – 40 GB

- OS: Ubuntu 20.04 LTS

- Software: NGINX 1.14.0

System management

System management basically allows you to create certain standards and rules for their behaviour as well as to determine main services and functions that will be available for your customers (individuals and merchants).

There are the following use cases within the system management for the payment processing business:

Contract management includes creating custom contracts, adding commission rules, editing system settings, and activating provider commissions.

Payment gateway management involves configuring exchange rates and currency management.

Reports and analytics offer the opportunity to generate transaction-based reports, which can be downloaded for further analysis.

Explore our knowledge base to find out more about system management.

Merchant account management

This step involves 4 main stages: KYC management, user profile management, user registration, and revision.

User profile management covers registration( by email or by phone number) and profile deactivation. The administrator can also update profile and business details and manage security settings.

KYC management allows you to cover basic compliance processes such as uploading the documents, verifying documents and users, and requesting users’ actions to complete the compliance procedure.

For more sophisticated KYC and AML functionality we can recommend integration with specialized third-party providers.

Watch SDK.finance Platform’s demo video to explore how to manage your users, ensure KYC compliance, and prevent fraud with the robust system back office:

Read our knowledge base to get more details about user management.

Merchant products management

Merchants can create, view, update, and delete products using the available functionalities. This module provides merchants with the ability to manage their products’ prices and measure units as well.

Further, the functionality can be extended by allowing users to tag the transactions for merchant products to control their spending. This functionality is not provided on the UI but is fully functional on the backend and covered by APIs. The administrator can update the following use cases:

- merchant product and categories creation

- merchant measure units updation

- merchant product prices configuration

Check our knowledge base to find out more information about merchant product management.

POS management

This module allows merchants to add, view, edit, and delete their POS systems, as well as generate new secret codes to ensure security. It also enables merchants to view a list of their POS systems and access detailed information about each system, including transaction history per each POS.

Additionally, the module allows merchants to edit their POS systems to ensure accurate and up-to-date information is reflected. You can find more information about POS management in our knowledge base.

Payments and transactions

This functionality includes funds transfer, bill payment, recurring payments setting up, currency exchange, invoicing, and merchant payment services through merchant accounts.

Funds transfer

This functionality is available on UI provided out of the box and has the following flow:

- The user creates the transfer and specifies the following information: source wallet for transfer; recipient wallet serial number; transfer amount

- The system validates the recipient’s wallet serial number

- The system calculates the commission and checks the limits

- The user checks the commission and confirms the transfer.

- Funds are transferred to the recipient’s wallet.

Here you can get information about funds transfers, templates, and contract payments.

Accounting

Accounting plays a critical role in managing the flow of funds and ensuring financial accuracy and transparency for payment processing business. We have pre-implemented a dedicated dashboard for the accountant role which is available out of the box and provides some basic functionality:

- Transactions. It is possible to view and filter all transactions, providing oversight and maintaining records for future reference.

- Withdrawal. You can manage withdrawal requests and bank operations, either accepting or declining transactions based on the system’s requirements.

- Top-up via bank. Accountants can execute top-ups for users and view all top-up requests, ensuring that funds are properly added to user wallets.

- Cash desks. It allows you to view and manage cash desks, transactions, and withdrawal requests, as well as accept closing day requests to maintain accurate records and balance cash desk accounts.

- System operations. Accountants can initiate various system operations, such as cash input, cash collect, investments, and gate investments, to manage the flow of funds within the e-wallet system.

Our knowledge base provides you with detailed information about accounting capabilities.

Reporting

The system offers users the opportunity to generate transaction-based reports, which can be downloaded for further analysis. All data is securely stored in the system’s database, which can be integrated seamlessly with any reporting or monitoring tool. This is especially effective when paired with QuickBooks payment integration, allowing businesses to sync transaction data automatically and keep accounting and reporting fully aligned.

Users with all roles can view statement reports in the transactions section, but downloading reports is limited to the individual role for security reasons.

In conclusion, the system’s database offers unparalleled integration possibilities with any report engine or analytical tool, providing users with a seamless and customizable reporting experience.

How much does it cost to start a payment processing company?

It is difficult to estimate the final cost of starting payment processing vendors because it depends on a number of factors.

Factors affecting the cost of starting a payment processing business

The key factors to consider when building payment processing software are listed below.

- Features you want to implement. You need to understand what features are necessary for payment solutions. The complexity of your company determines the costs.

- Development tools. It is also important to recognize what programs do you need to build, test and debug software. To get more info about payments stack and development tools, check our post on the Best payment tech stack for the financial industry.

- Development team. The cost depends on the team you work with, for example, if you need to hire a development team the cost will increase.

- Location. Depending on which area you are starting a payment processing business, the project cost can vary.

Using a pre-developed SDK.finance payment acceptance software you can save time and money resources, without starting from scratch. You can start with an affordable subscription-based option or use an on-premise one that comes with the source code license, available for a one-time flat fee.

For the sake of compliance with regulations and security, the central database is hosted on your own server, while the app is deployed using cloud providers like AWS or Azure.

Wrapping up

If you want to build a payment processing system, you can choose a ready-made solution, saving your money, and speeding up the market entry process. Nevertheless, even a pre-developed platform is far from being a turnkey solution and requires efforts to adjust it to your particular business needs. In other words, it provides you with a software foundation for starting a payment processing business.

SDK.finance is a shortcut for building a payment processing solution via its software, so reach out to us and let’s talk.